Table of Contents

What Is A Life Insurance Trust?

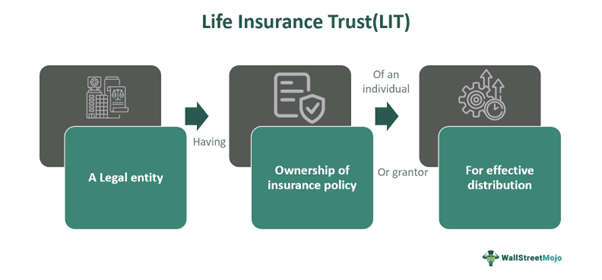

A life insurance trust (LIT) refers to a legal entity established to take control of the ownership and death benefit of life insurance of an individual or grantor. It ensures the distribution and management of insurance proceeds effectively between beneficiaries without getting subjected to estate tax.

Here the trustee handles and oversees all the benefits of the insurance policy. It allows the grantor to align distribution structure of assets to beneficiaries as per their wishes, time and manner. the distribution of the policy proceeds has to be done as per trust document terms.

Key Takeaways

- Life insurance trust is a legal arrangement to distribute policy proceeds bypassing probate and estate taxes through trust owned policy.

- It can be setup by determining trust categories, select beneficiaries, calculating insurance needs, choosing

- and purchasing life insurance, and transferring ownership with the help of an estate planning attorney.

- It helps in reducing or eliminating estate taxation leading to estate tax savings but requires substantial costs for setting up.

- Its trustee has the authority to legal ownership & control of the trust whereas in living trust, the grantor has full ownership & control over the trust during their lifetime.

Life Insurance Trust Explained

A life insurance trust means a legal structured arrangement to form an irrevocable trust for placing a life insurance policy inside the trust to distribute and manage the policy’s death benefit. A few people do it to bypass estate taxes and probate and allows policy proceeds to the beneficiaries after grantor’s death in a hassle-free manner as per the desires of the grantor. It helps exclude the policy proceeds from the taxable estate. It acts as a vehicle to conserve and handle life insurance benefits and address tax considerations and estate planning.

It works in the following manner:

- The grantor creates an irrevocable trust while designating beneficiaries to receive the death benefit of life insurance after grantor’s death.

- Then the existing or the new policy is legally transferred to the trust that removes all ownership of the policy from the grantor and gives the ownership to the trust.

- After that grantor nominates trustees to handle the trust by paying the premium, management of trust asset, and distribution of death benefit of the policy to the beneficiaries as per grantor’s wish.

- As a result of the trust, the proceeds of life insurance policy get exempt from taxable estate of grantor, reduces estate taxes owed by the beneficiaries.

- Finally, after the grantor’s death, all the policy proceeds are transferred to the trust. next the trustee distributes the funds to the selected beneficiaries as per the instructions inscribed in the trust document.

Therefore, setting up of a trust of life insurance, not only safeguards policy proceeds from taxes and probate but also helps in convenient in death benefit distribution to the beneficiaries.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

How To Set Up?

For setting up of an LIT one has to follow the below steps:

- Find out the categories of trust that can be made like revocable life insurance trust fund or irrevocable life insurance trust.

- Then select the persons from the family who would be the beneficiaries of the trust.

- After that, the total current and future needs of the insurance for the trust have to be calculated using online calculators or methods like debts, income, mortgage and education (DIME) method.

- Further, one must choose the best life insurance like permanent one or aicpa life insurance trust which does not expire or term life insurance.

- Next purchase the selected life insurance from a trusted broker and writing the trust as the beneficiary of the life insurance policy to get whole insurance proceed to the trust.

- Finally, ownership of the trust has to be transferred to the trust with the help of estate planning attorney.

Therefore, after all these steps, the trust owns the responsibility to manage the policy, its make premium payments and lay claim over death benefit.

Examples

Let us use a few examples to understand the topic.

Example #1

An online article published on 20 November 2023, discusses about the role of trust in ownership of lie insurance policies. the article underscores that by owning a life insurance in trust, beneficiaries can get the protection from estate tax. moreover, an insurance trust can be beneficial to married couples:

- As it can provide protection to insurance proceeds from coverage of estate taxes.

- Also, it can curtail the limit of spouse's estate value from breaching the exemption threshold of estate tax.

Further, the article explains in detail the procedure of transferring life insurance ownership to a trust. It also mentions the significance of surviving beyond three years post-transfer excluding proceeds of insurance proceeds from estate tax. lastly, it also talks about selection of insurance as per the purpose of the trust.

Example #2

Let us assume that an office clerk, Jackman wants to secure his family’s future using a life insurance policy. For the purpose, he decided to create Old York Insurance trust in consultation with his estate planning attorney. The attorney drafted a trust document suggested and nominated jackman’s wife and kids as beneficiaries.

As a result, the trust will be the owner of the insurance policy to ascertain the insurance proceeds to remain exempt from estate tax. but, still jackman had to live for three years after the policy is transferred into the trust. as a result of such a structure, of the life insurance policy trust, jackman maximized the benefits of his policy and reduced the estate tax burden to a great extent.

Advantages And Disadvantages

Let us understand the pros and cons of such trust for life insurance policy using the table below:

| Advantages | Disadvantages |

|---|---|

| It helps in reducing or eliminating estate taxation leading to estate tax savings. | It requires substantial costs for setting it up and running like attorney cost. |

| It safeguards eligibility of beneficiary for various government benefits. | It has irrevocable nature which cannot be revoked under any circumstances rendering it ineffective during emergency situations. |

| It provides legal and convenient method of distributing proceeds as per the wishes of the grantor. | Has lot of legal complexity involved necessitating legal help. |

| Helps beneficiaries receive the inheritance of policy in short time. | Policy cannot be withdrawn as it is irrevocable. |

| It can also protect inheritors from inheritance tax by upto 40%. | One could lose some control over the policy duet to requirements of trustee signature. |

| It assures easy liquidity to larger estate holder without asset dissolution. | Has three year period of look back where if the grantor dies inside three years of creating the trust then the policy comes under estate tax. |

Life Insurance Trust vs. Living Trust

Let us use the table below to understand the differences between the two types of trusts:

| Life Insurance Trust | Living Trust |

|---|---|

| Trustee has the authority to legal ownership & control of the trust. | Grantor has full ownership & control over the trust during their lifetime. |

| Has the nature of irrevocability. | Remains revocable during grantor’s life time. |

| Asset do bypass probate process. | Same |

| Policy becomes excludable from estate tax if the policy holder lives for three years. | After death, all assets come under the purview of taxable estate. |

| Trustee or Grantor pays insurance premiums | Only grantor pays the premiums of insurance directly. |

| Involves complex legal documentation needing help of an attorney. | Does not require the help of attorney to create the living trust however complex situations might need one. |

| Grantor nominates beneficiaries. | Same. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.