Part of our Balance Sheet guide

What is Asset Classification?

Asset classification is a process for systematically segregating the assets into various groups, based on the nature of the assets, by applying the accounting rules to make proper accounting under each group. The groups are later consolidated at the financial statement level to report.

- Asset classification involves categorizing assets into different groups based on their nature and applying accounting rules to ensure accurate accounting for each group. These groups are then combined at the financial statement level for reporting purposes.

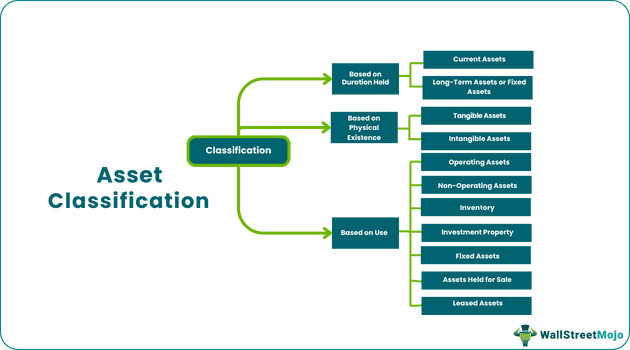

- Its classification is determined by three specific criteria: Duration Held, Physical Existence, and Use.

- Proper asset classification is crucial for accurate financial statements. An incorrect categorization can mislead working capital and revenue generation evaluations and impact a company’s solvency. A distinct type is essential for reliable economic parameters.

Asset Classification Criteria

Classification is done based on specific criteria, as explained below.

A) – Based on Duration Held

Classification based on the duration held is explained below:

#1 – Current Assets

These are the assets intended to be held in the business for less than one year. These assets are highly liquid and are expected to be realized within one year. Examples of short-term assets include cash, bank balance, inventory, accounts receivable, marketable securities, etc.

#2 – Long-Term Assets or Fixed Assets

Long-term assets include fixed assets (commonly known as property, plant, and equipment), long-term investments, trademarks, goodwill, etc. These are the assets intended to be held in the business for more than one year. These assets are expected to provide benefits to the business for several years.

B) – Based on Physical Existence

Classification of assets is based on their physical existence are, explained below:

#1 – Tangible Assets

Tangible assets are those that have a physical existence, i.e., capable of being touched, felt, and seen. Examples of such assets include plant, property and equipment, building, cash, inventory, etc.

#2 – Intangible Assets

Intangible assets are those kinds that do not exist in physical form. In other words, these assets cannot be touched, felt, or seen. Examples of such assets include patent, license, goodwill, trade name, brand, copyright, etc.

C) – Based on Use

Classification of assets is based on use are explained below:

#1 – Operating Assets

It refers to those assets that are useful in the conduct of the day-to-day operations of a business. These assets help in the generation of revenue and are connected with the core business of the organization. Examples of such assets include inventory, accounts receivable, property, plant and equipment, cash, etc.

#2 – Non-Operating Assets

These assets are those that are not required in the conduct of the daily affairs of the business. They do not play any role in revenue generation. Examples of such assets include fixed deposits, marketable securities, idle equipment, idle cash, etc.

#3 – Fixed Assets

These are those assets that are not held for sale. Instead, they are held to produce goods or provide services.

#4 – Inventory

It refers to those assets held for further sale in the course of business. Thus, a building will amount to inventory for a real estate dealer, while for other businesses, the same will form part of fixed assets. It depends on the use for which assets are deployed, and the asset cannot be generalized, and instead, it needs to be classified as per its use and other terms.

#5 – Investment Property

These are the properties owned, acquired by finance lease, or constructed by an organization for further sub-lease by way of an operating lease to other parties.

#6 – Assets Held for Sale

It refers to those assets intended to be sold (other than in the course of business) in the present state and condition within 12 months. The carrying amount is recovered by way of sale.

#7 – Leased Assets

These are the assets given under a finance lease to some other person or taken under operating lease from other person.

Conclusion

It is essential to classify the assets in the financial statements properly. Or otherwise, the financial statements may be misleading. Let us consider an example wherein a current asset is wrongly classified as a non-current asset. It will result in an incorrect representation of working capital as the same considers current assets. Also, asset classification is necessary to understand which assets help in revenue generation and which do not contribute. It also helps to identify the solvency of a business. Thus, for financial parameters to be correct, the classification must be correct.

Frequently Asked Questions (FAQs)

What is asset classification in cyber security?

Information assets are sorted based on their confidentiality, integrity, and availability level to ensure security. Each of these principles is rated low, moderate, or high.

Why use asset classification?

To help investors achieve their financial goals, financial advisors use asset classification to determine if they are over or under-diversified. It is based on their age, risk tolerance, personal preferences, and investment objectives.

What is the role of asset classification in an investment policy statement (IPS)?

In an investment policy statement (IPS), asset classification outlines the strategic asset allocation targets that define how the investment portfolio will be diversified across different asset classes. It is a guideline for the investment manager, helping them make informed decisions aligned with the client’s risk tolerance and investment objectives.

How does asset classification help in managing investment risk?

Asset classification helps in managing investment risk by allowing investors to diversify their portfolios across different asset classes. When one asset class performs poorly, others may perform better, reducing overall portfolio risk. Different asset classes have varying levels of risk and return potential, and by allocating assets wisely, investors can balance risk and reward.

Recommended Articles

This article is a guide to Asset Classification. Here we discuss the classification of assets based on parameters that include Based on Duration Held, Based on Physical Existence, and Based on Use. You can learn more about Corporate Finance from the following articles –