What Are Net Fixed Assets?

The Net fixed asset is the asset’s residual value of the fixed asset. It is calculated using the total price paid for all fixed assets at the time of purchase minus the total depreciation amount already taken since the time assets were purchased.

- If the accumulated depreciation of the asset is enormous, it means that the age of the asset is high, and the company has not replaced its assets for a long time. This metric is more useful for the investors as it gives the idea that at that time in the future the company is going to make a massive investment in the purchase of assets.

- Additionally, it also helps investors know how efficient the company’s management is in using its assets. This metric is more useful at the time of mergers and acquisitions. If the company is analyzing the different possible acquisition candidates, then, in that case, they must analyze assets’ value based on that only they can put a value on them.

- Suppose the net fixed asset amount is low compared with the total fixed assets value. In that case, it shows that a vast amount will be needed in the future for replacing the assets, and the acquiring company can value the assets considering this in mind.

Net Fixed Assets Formula

When all the impairments and accumulated depreciation are deducted from the fixed assets’ purchase price and cost of improvement, we get the net fixed assets amount. In equation form:

Net Fixed Assets Formula = Gross Fixed Assets – Accumulated Depreciation

It is the basic form of the equation. The fixed assets include tangible assets, mostly as plants & machinery, buildings, equipment, furniture, etc. Accumulated depreciation is the total amount of depreciation expense that has been charged to profit and loss account from the date of purchase of the fixed asset.

Many analysts think that the formula needs to be taken a step forward. So, besides accumulated depreciation, they also remove fixed assets and liabilities from the fixed assets and the improvement cost.

The above sentence can be represented in a net assets formula which is as follows:

Net Fixed Assets Formula= (Total Fixed Asset Purchase Price + capital improvements) – (Accumulated Depreciation + Fixed Asset Liabilities)

The liabilities related to fixed assets are removed to know the actual net assets that the company owns.

Liabilities are the financial obligations and the combined debts that the company is obliged to pay to outsiders.

Components of Net Fixed Assets

#1 – Fixed Assets

Fixed assets are the assets that enterprise purchases for long-term use and are not meant for sale, unlike stock. These assets are not readily converted into cash and are utilized for generating revenue. Fixed assets are of two types

- Tangible assets (that can be touched) such as building, plant & machinery, equipment, furniture, etc.

- Intangible assets (that cannot be touched) such as goodwill, patent, trademark, etc.;

#2 – Accumulated Depreciation

The accumulated depreciation charged on an asset from its starting use until its present use is the accumulated depreciation. Each year, the depreciation is charged on the asset, which is then added to the accumulated depreciation account. For example, On 1st April 2016, furniture worth $100,000 was purchased. The useful life of plant & machinery is 15 years, and says its residual value is 10% of the asset’s cost. So depreciation for the financial year 2016-17 is ($100,000 – 10% of $100,000)/15 = $6000.

Similarly, for 2017-18 and 2018-19, the depreciation charged is $6,000 each year. Therefore, the accumulated depreciation as of 31st March 2019 is:

$6,000 + $6,000 + $6,000 = $18,000 i.e. the cumulative depreciation from its date of put to use till the present date.

#3 – Capital Improvements

Improvements are the capital additions on the fixed assets, which are done to increase the efficiency and capacity of the asset, increasing its operational efficiency. The depreciation is charged on the capital improvements over its useful life.

#4 – Fixed Assets Liabilities

Liabilities associated with fixed assets are fixed assets liabilities that include all the debts arising due to the purchase or improvements of fixed assets. The company is required to pay the same to the outsiders.

Example of Net Fixed Assets Formula

Let’s take the example of Shanghai automobiles, which wants to expand its operations. The company is planning to buy another company named Apex Automobile, having its operations in another territory.

So Shanghai automobiles want to decide whether they should buy an apex automobile or not. So for that, Shanghai automobiles want to ensure that the assets of the apex automobile are in good condition. So if the assets came out to be in good condition, then the shanghai automobiles are not required to buy new assets for the furtherance of business.

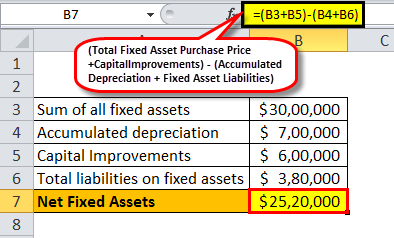

The balance sheet of apex automobiles reported the following figures in the balance sheet:

- Sum of all fixed assets: $3,000,000

- Accumulated depreciation: $700,000

- Capital Improvements: $600,000

- Total liabilities on fixed assets: $380,000

Therefore, the net fixed assets of Apex ltd are:

Net fixed assets = ($3,000,000 + $600,000) – ($700,000 + $380,000) = $2,520,000

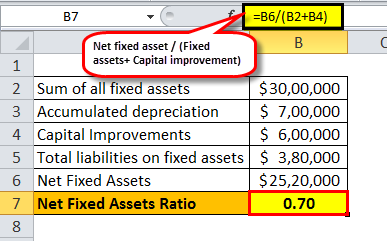

Now for the analysis, we need to calculate the ratio which is as follows:

Net Fixed Assets Ratio formula = Net Fixed Assets/ (fixed Assets +Capital Improvements)

=$2,520,000 / $3,600,000 = .70

The ratio analysis shows that the apex automobile has assets depreciated to 30% of the total cost and the improvements of the fixed assets. It shows that the assets are not that old and can be used for a large duration in the future.

Advantages

- The net fixed asset information in any company helps the company’s stakeholders know the financial reporting, financial analysis, and business valuation. It helps determine the financial health of the company.

- It is helpful for the analysts to know how the numbers are determined. Using the metric, they can know what method was used by the company because there are multiple accepted methods for recording assets, depreciating assets, and disposing of assets.

- Fixed assets analysis is very important in capital-intensive industries because these industries require huge investments in Plant, Property & Equipment. When there are net negative cash flows because of the purchase of the fixed assets, then it is the indicator that the firm is in growing mode.

Disadvantages/Limitations

- Use of Net Fixed Assets will be meaningless if there is accelerated depreciation. For example, equipment is purchased by the company, and in the same year, it claims full depreciation of the entire purchase as per any section, which allows full depreciation in the same year. So, in that case, the new equipment will have zero net book value, which may lead to wrong interpretation.

- If the asset is already depreciated fully does not mean that the asset is necessarily worthless. Many assets are there, the life of which is less, but they prove useful for even 3-5 times over the expected life.

- Before making any conclusion, one should look at the differences between values per tax and values per the book because accelerated depreciation schedules are mostly acceptable for tax purposes. Still, the same is not allowed by the GAAP.

Conclusion

Many entrepreneurs don’t have a clear idea of the worth of the asset their company is holding, which at a later stage can prove costly to them as it is always good to know the worth of the company so that future decisions can be taken accordingly. In this context, Net Fixed Assets have become very important.

Recommended Articles

This article has been a guide to Net Fixed Assets. Here we discuss how to calculate Net Fixed Assets using its formula and practical examples. You may learn more about accounting from the following articles –