Part of our Balance Sheet guide

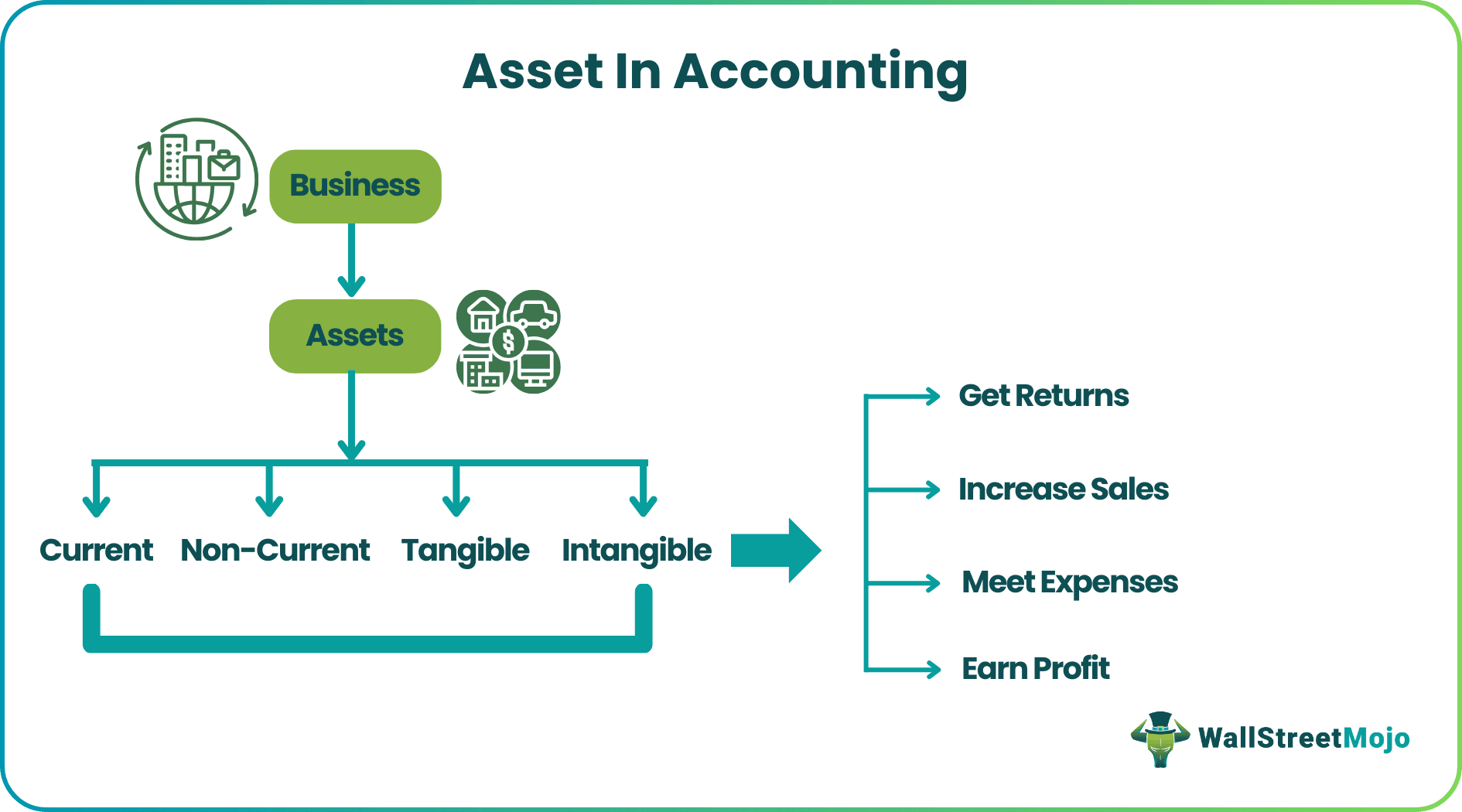

What Are Assets In Accounting?

Assets in accounting are a medium through which one can undertake business, which is tangible or intangible in nature with a monetary value due to the economic benefits. Assets include property, plant and equipment, vehicles, cash or cash equivalent, accounts receivables, and inventory.

The characteristics of assets are that it is owned and controlled by the enterprise. It provides a future economic benefit It is an important resource for the entity that will earn returns if sold or invested. Thus, it increases the entity’s value and control expense, leading to higher sales and profits.

- Assets in accounting are useful for undertaking business activities; they can be tangible or intangible and have a monetary value. Assets can be property, plant, machinery, equipment, vehicles, cash, equivalents, etc.

- They are of two types – Current and Non-current assets. Current assets are prepaid liabilities such as cash and cash equivalents, whereas non-current assets are property, plant, and equipment and are often referred to as derivative assets.

- Certain numerical factors affect the price of assets, such as depreciation or amortization, obsoleting technology, change in statutory requirements, impairments, etc.

Assets In Accounting Explained

All assets in accounting in a business are the resources that is used to to get a return either by selling or investment. They add value to the business, and get converted to cash in case need arises to meet any expenditure. They include property, plant and equipment, Cash and Cash Equivalent, vehicles, inventory and accounts receivables.

Assets represent the investments that an entity owns, and by utilizing these, the company can meet all its future liabilities. Hence, it is of utmost importance to determine the value of list of assets in accounting and check the assumptions to calculate the same.

Previously, there have been several instances where the assets were misrepresented, and financial statements were window dressed to obtain funding for financial institutions. Hence, while reading the assets in the balance sheets, one should read notes to accounts accurately, considering all the disclaimers provided by auditors and the board of directors.

Types

The various types of assets in accounting are mentioned below:

As per the capacity to get converted into cash, list of assets in accounting can be:

Based on the asset’s maturity, they can be classified as current assets in accounting (if maturing in 12 months from the reporting date) or Non-Current (if maturing beyond 12 months from the reporting date).

There are various kinds of components of current assets in accounting as well as non-current assets, which are as follows:

Current Assets Non-Current Assets

| Current Assets | Non-Current Assets |

|---|---|

| Cash and cash equivalent | Property, plant, and equipment |

| Trade Receivables | Intangibles |

| Readily Marketable securities | Long term lease obligations |

| Stock in trade | Investment in subsidiaries |

| Deposits | Deferred tax assets |

| Prepaid liabilities | Derivative assets |

As per the physical existence, all assets in accounting can be:

- Tangible assets

- Intangible assets.

Tangible assets are the ones that can be seen or touched like building, plant, machinery, vehicles, inventory, etc, whereas intangible assets are the ones that cannot be seen or touched like goodwill, patent etc.

Examples

All corporations have to calculate their assets and liabilities based on a given set of instructions and guidelines. Accordingly, they have instructions for each of the above components, which must be followed while calculating them.

Additionally, the total asset figure is the total of all the components mentioned above, the assets duly calculated as per the rules.

Let’s understand some examples of assets accounting.

Example #1

The following are the asset components of Amazon Inc. as of December 31, 2017.

Cash of $19,334 million

Marketable securities of $6,647 million

Inventories of $11,461 million

Trade receivables of $8,339 million

Property, plant, and equipment of $29,114 million

Goodwill of $3,784 million

Other assets of $4,723 Mn

The calculation of Total assets in accounting is as follows,

Total assets of the company = $19,334 million + $6,647 million + $ 11,461 million + $8,339 million + $29,114 million + $3,784 million + $4,723 million = $83,402 million

Hence, Amazon Inc. has $83,402 million as of December 31, 2017.

Example #2

Following are the components of the BP group of companies as of December 31, 2017. Please calculate current assets, non-current assets, and total assets:

Property Plant and Equipment of $129,471 million

Intangibles of $29,906 million

Investment in subsidiaries of $26,230 million

Derivative financial instruments of $4,110 million

Deferred tax payments of $4,469 million

Inventories of $19,011 million

Trade receivables of $24,849 million

Cash and cash equivalent of $25,586 million

Calculation of current assets in accounting is as follows,

Current Assets= $19,011 million + $24,849 million + $25,586 million = $69,446 million

The calculation of non-current assets in accounting is as follows,

Non-Current Assets = $129,471 million + $29,906 million + $26,230 million + $4,110 million + $4,469 million = $194,186 million

The calculation of total assets in accounting is as follows,

Thus, Total Assets= $263,632 million

Hence, the BP group has total assets worth $263,632 million as of December 31, 2017.

Limitations

- Consideration of only monetary factors ignores non-monetary factors. Hence, intangibles such as self-developed patent valuation will always be under doubt of improper calculation.

- Historical-based accounting, hence present market value, is not available in consideration of only Monetary Factors. It ignores non-monetary factors. Hence intangible assets in accounting is such as self-developed patent valuation will always be in doubt of improper calculation.

- Hence, Historical based accounting, is not available in the financial statement, hence present market value.

- The depreciation method is for the management to choose the property, plant, and equipment. Due to this, comparability is not possible.

- Estimates are considered while assuming the useful life, scrap value, etc. Therefore, professional judgments are used to estimate highly subjective figures.

Valuation

The value of assets keeps on changing from year to year. There are numerical factors that can affect the values of the assets.

- Depreciation and amortization – One has to determine the method of depreciation of PPE by considering the nature of assets, their useful life, and scrap value. For amortization, one has to consider the nature of intangibles, their ownership, and how they will help the entity gain revenue.

- Impairment of assets– Impairment means to deplete the value based on the change in market factors. It is considered when the asset’s book value is less than its market value.

- Obsoleting technology – Machinery is highly dependent on the version of technology prevailing in the market. Hence, any obsolescence will lead to a change in the value.

- An asset sale is one of the most common scenarios in which an entity sells the assets either for replacement or diversification. The main thing one has to determine while recording the sale of an asset is the gain on sale, market rate, and stamp duty value.

- Change in the asset’s useful life – Many factors like depreciation, impairment, or capacity highly depend on the useful life estimate. Auditors should consider any change in the same judiciously. Also, taking professional or actuarial opinions while estimating the useful life will add to the authenticity of the estimates.

- Change in the statutory requirement to change the disclosure – Accounting of the assets always happens under the strict guidelines of IFRS, GAAP, and local laws. Disclosure and valuation will be dependent on these rules. Thus, any change in them will directly affect the disclosure and valuation of the statements.

Frequently Asked Questions (FAQs)

What are fixed assets in assets of accounting?

A physical piece of property, plant, or equipment (PP&E) that you own or manage with the assumption that it will continually contribute to income generation is referred to as a fixed or a capital asset.

What are quick assets?

Current assets like accounts receivable that can be converted to cash with little to no discounting are considered quick assets.

What are intangible assets in accounting?

Intangible assets are assets that aren’t physical. For example, intangible assets include computer software, licenses, trademarks, patents, films, copyrights, and import quotas.

Will loan be considered as an asset?

A loan may or may not be considered an asset, depending on a few conditions. For example, a borrower receives cash as part of a loan, which is a current asset; nevertheless, the loan amount is also included as a liability on the balance sheet. In addition, a loan issued by a party that will be repaid in less than a year can qualify as a current asset. On the other hand, it is not a current asset if a party offers a loan that must be repaid after a year.

Recommended Articles

This has been a guide to what are Assets In Accounting. We explain it with examples, the various types, their valuation and limitations. You can learn more about accounting from the following articles-