Part of our Balance Sheet guide

What Is Restricted Cash?

Restricted cash is that portion of the cash set aside for a specific purpose and is not available for general business use on an immediate basis. This cash is usually held in a special account (for example, an escrow account), so it remains separate from the rest of a business’ cash and equivalent.

In the broader sense, it is the portion of money a business entity has in its possession but can’t use immediately. Instead, that cash portion is subjected to special limitations, such as being earmarked for future use or waiting period. It may represent cash amount on its way into the business or cash held before spending. Such kind of cash is not available for current use. It is not considered part of the liquidity source and is excluded in calculating various liquidity ratios.

Restricted Cash Explained

The term restricted cash explain the amount of money that a business will keep aside for a particular purpose and not for normal business operation. There are some specific reason, due to which such funds are kept separately.

It is normally displayed in the balance sheet along with details and description of the reason for such a provision along with notes in the financial statement. Restricted cash in balance sheet makes it easy for the analysts and investors and other stakeholders to understand why such funds are being kept aside, what is the cash status after keeping aside such money and whether these provisions are worth for the business operation.

Common reasons for keeping money aside for restricted purpose are meeting loan instalments, or urgent bill payments, bank policy related funds, meeting long term liabilities like pension funds, loan collaterals, etc.

Here, the time period of holding the cash aside matters a lot because based on that the item will be displayed in the balance sheet under the head of current asset or under non-current asset. However, it may be help in many ways, like opening of a separate bank account for only this purpose.

It is to be noted that in case the entire fund is not used up for the intended purpose, the business may transfer it to the general account which is available for normal business operations. Sometimes the management makes plans for some particular expenditure but decides to go against it later on. Thus, the cash gets freed up and can be invested somewhere else.

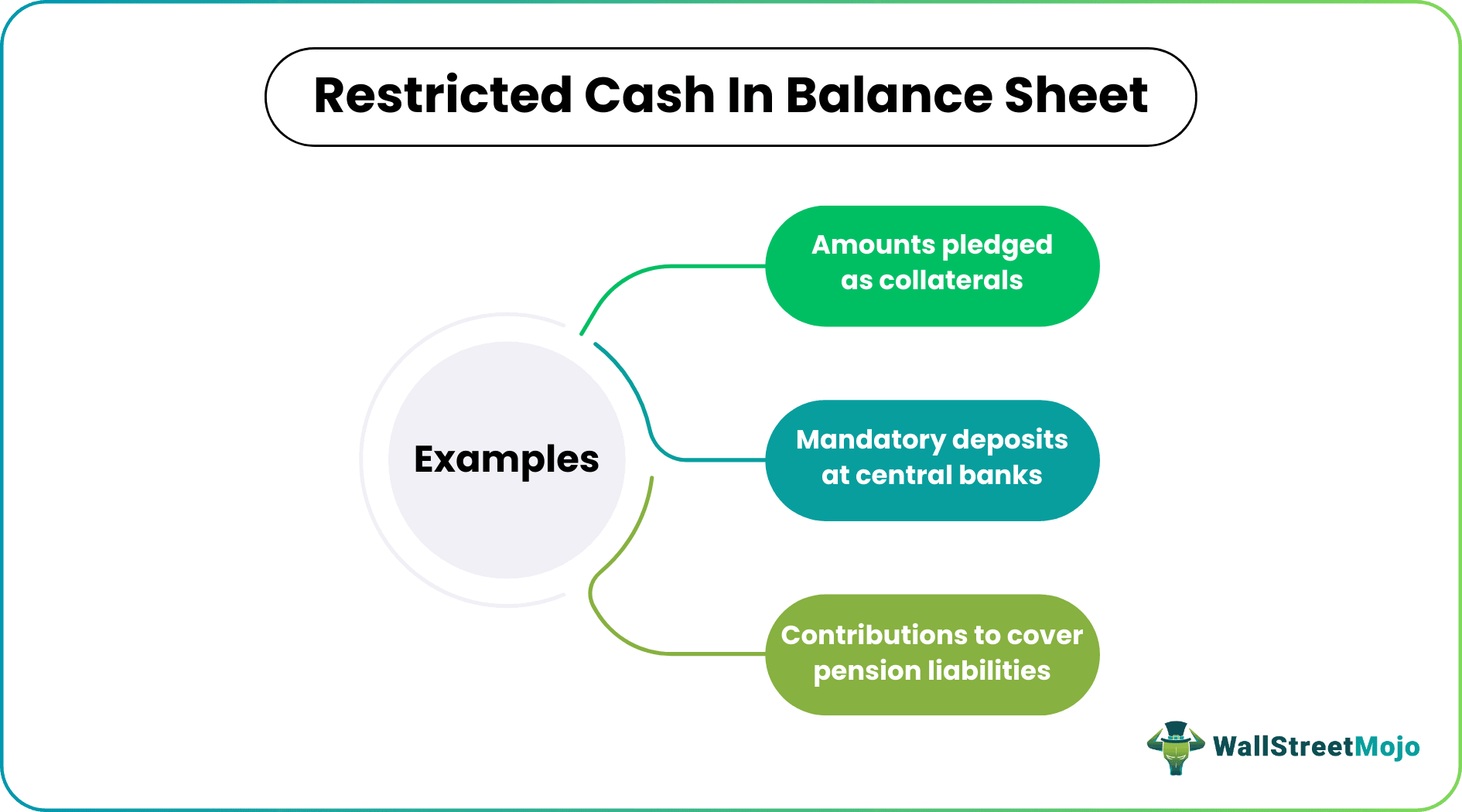

Examples

Let’s discuss the following examples of restricted cash in balance sheet.

- Amounts pledged as collaterals.: Sometimes, some corporations pledge a certain amount of cash as collateral against the risk covered by an insurance company. They generally maintain such cash in a separate escrow account.

- Mandatory deposits at central banks.: This is the most common deposit of restricted cash where the bank needs to deposit a certain amount of cash in the central bank (RBI in India), and this amount is not available.

- Contributions to cover pension liabilities.: Companies in specific geographies maintain funds to cover some employee benefits, like pensions for future payments.

Accounting

The correct accounting method for this type of item in the books are elaborated below. Let us study the restricted cash disclosure in details.

#1 – Balance Sheet

A balance sheet for any entity must add all assets and liabilities, including cash and cash equivalents. Companies generally report such cash as a separate line item as part of the cash and cash equivalents account on a company balance sheet. They typically state why the cash is restricted in the accompanying notes. It allows a balance sheet to balance until the cash is brought in as revenue or paid out as an expense and accounted for normally.

#2 – Cash Flow Statement

Restricted cash on the cash flow statement is another form of financial statement that a corporation uses to account for such cash and keep its accounts balanced.

Cash flow refers to the rate at which cash moves in and out of business. The purpose of the restricted cash on the cash flow statement is to explain how and why the cash balance moved. Usually, a change in cash and cash equivalent is presented in the final reconciliation at the end of the cash flow statement as the purpose of the restricted cash on cash flow statement is to explain how and why the balance of cash moved.

When there is cash that is not presented as part of the cash balance in the balance sheet, a change in restricted cash would be presented either in cash from operating activities, cash from investing activities. Or in cash from financing activities, depending on maintaining cash on the balance sheet.

For example, changes in the cash because the repayments of borrowings are reported under cash flow from financing activities.

Changes in deposits taken from clients to construct an asset are generally related to the main operation and thus are covered under operating activity.

In cases where restricted cash disclosure is expected to be used after one year from the balance sheet date, it should be classified as a non-current asset. However, if it is expected to be used within 12 months from the balance sheet date, it should be classified as a current asset.

Examples

Let us understand the terms of restricted cash flow with the help of a few suitable examples.

Example #1

ABC Inc. is engaged in large equipment manufacturing. It received an order from one of its customers for a piece of equipment for finishing and shipping within the next three months. The customer has made an advance payment (deposit) to ABC for the same. ABC must transfer this deposit to a separate bank account as per the customer contract. It cannot be used until the equipment ships. This advance payment received from the customer can classify as restricted cash on the ABC’s balance sheet. The company cannot use it until a future event occurs (the shipment of equipment). Once the equipment ships, this cash is available to the company for its regular operation.

Example #2

XYZ Inc. sets aside a certain amount of cash each month to pay a long-term debt, which is to be paid off in two years. The amount of cash set aside is restricted in nature as it can only be used for debt repayment in the future and thus represents restricted cash. When the loan settlement comes, the company will use the restricted funds to pay off the debt.

From the above examples, we see two different situations where the concept of restricted cash balance has been used successfully to keep aside fund for meeting important financial requirement. This not only ensure that the liabilities are paid on time and any kind of penalty is avoided, it also helps the bsuiness and management to understand how much money they have left which can be used for other useful business operation. In simple words, this act as a guide while making a budget for meeting company expenses.

Compensating Balances

Compensating balance is a minimum cash balance that a company must maintain in an account primarily maintained as part of a contractual agreement with a potential or current lender. A compensating balance is generally used to offset a bank’s costs when lending out money partially. It is typically calculated as a loan percentage. For example, a company agrees to keep $800,000 in a bank account in exchange for that bank extending an $8 million credit line. Compensating balances are often considered restricted cash and must be reported on a company’s balance sheet.

How To Audit

There are few steps involved in the audit procedure of such restricted cash flow. Let us study the steps in details as given below:

- Identify the reason – It is necessary for auditors to identify the reasons for keeping aside the cash balance. Therefore, it is important to review and study all documents and proofs related to the funds in order to justify the treatment. The documents can be related to resolution taken by the board of directors or any legal restriction or rules that the company should follow.

- Segregation – The auditors should identify the value of restricted and unrestricted cash properly and clearly and check whether they are properly accounted for as per accounting standards.

- Bank reconciliation – The bank balance and the cash balance should tally properly so that the balance matches as per the recorded amount. This also helps in identifying any discrepancy and misstatements.

- Compliance verification – It is necessary that the auditors verify all compliance issues regarding accounting and use of restricted cash along with any limits specified in the agreements. In case of any deviation, proper documents and authorization should be produced.

- Check for control – All implementation of internal controls are very important and should be followed diligently. Auditors should that the process is followed and proper measures are implemented to prevent anyone form accessing the funds without proper authorization of use.

- Recording – This amount should be properly recorded in the books and should match with other supporting documents. There should be clear, accurate and transparent reporting of its current status in the financial statement.

Maintaining transparency and accuracy is very important during financial reporting of this cash amount. Proper documentation, legal agreement and accounting standards should be implemented fro the same.

Restricted Cash Video

Recommended Articles

This article has been a guide on what is Restricted Cash, examples, and its definition. We also look at restricted cash accounting – balance sheet and cash flows and its associated examples. You may learn more about advanced accounting from the following articles –

- Balance Sheet Examples

- Financial Lease vs. Operating Lease

- Accounting Scandals

- Unearned Revenue Meaning

Recommended Articles

Continue with these closely related articles from the same guide.