Part of our Balance Sheet guide

What Is A Temporary Account?

Temporary accounts are nominal accounts with zero balance at the beginning of the financial year. At the end of the year, the balance is visible in the income statement and later transferred to the permanent account in the form of reserves and surplus. Thus, accounts that are part of the income statement are temporary and are periodically closed.

Temporary accounts are elements in accounting that remain in existence for a short period of time. Usually, they are started at the beginning of the accounting year and record every transaction within the accounting year. Temporary account accounting includes expense accounts, income statements, and withdrawal accounts. They are also referred to as nominal accounts.

- Temporary accounts are accounts with zero balance at the start of the financial period and close at the end to retain accounting operations during the period.

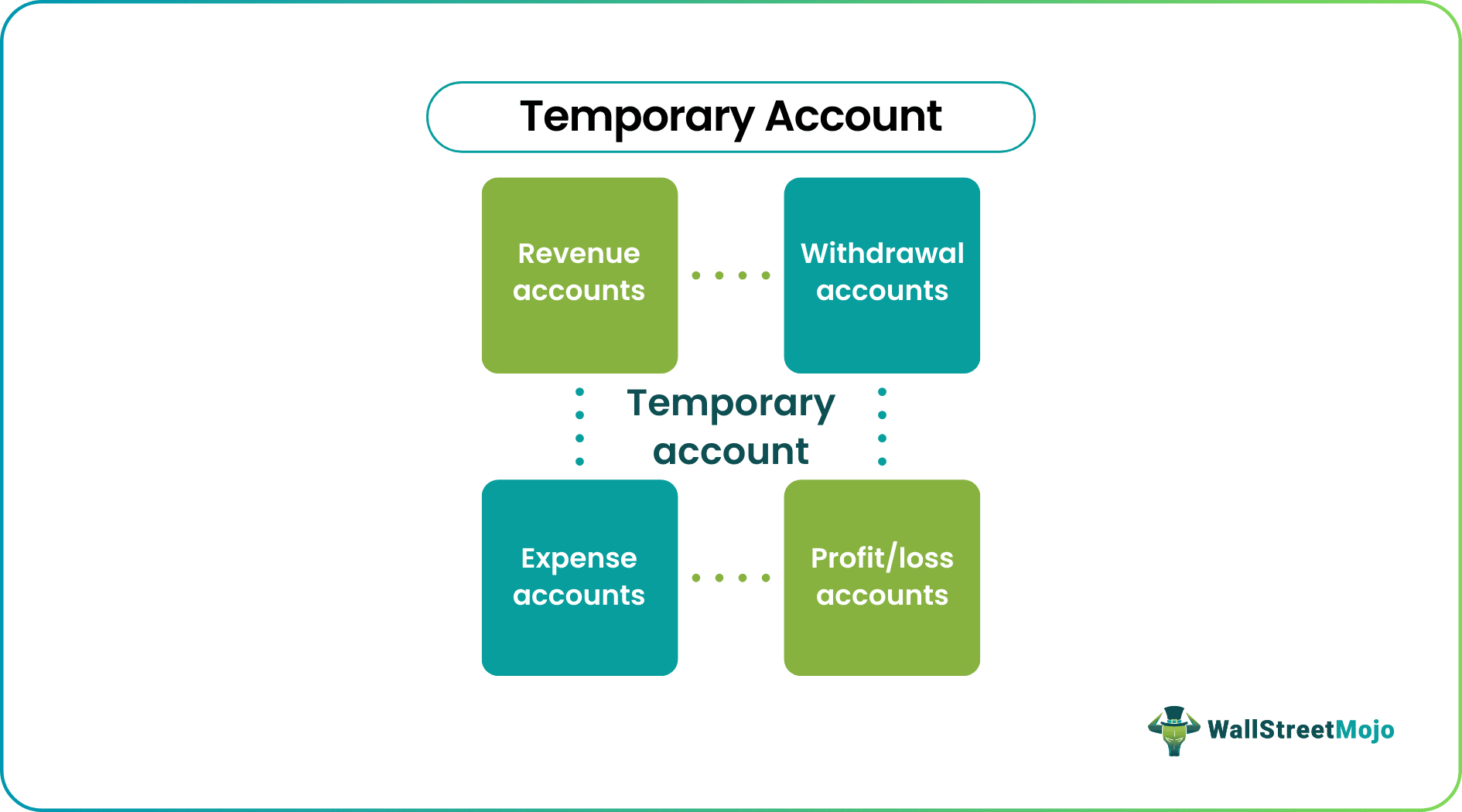

- The temporary accounts are revenues and gains, losses and expenses, and drawing or income summary accounts.

- The main objective of the temporary account is to view the profits or gains of the accounting period.

- It is crucial to classify an account carefully under a temporary account because if one considers any asset account wrongly, it may erode the entity’s asset base.

Temporary Account Explained

Temporary accounts are accounts that are reset after a fixed period with respect to accounting. After the reset, their balance is zero, and are started afresh. The resetting of these accounts is owing to calculating the gains or losses of the particular accounting period. Therefore, temporary account numbers are independent of the performance of the company in previous financial years.

These are prepared to avoid a mix-up of the balances between two or more accounting periods. The main objective is to see particular periods’ profits or gains and the accounting activity. It is essential to diligently classify any account under a temporary account because if any asset account is wrongly considered, it will erode the asset base of the entity.

Since these accounts are temporary, the entries are moved to permanent accounts according to relevance for long-term documentation. The long-term accounts or the permanent accounts provide a detailed account of the company and its profitability.

Types

Let us understand the different types of these accounts and temporary account accounting through the discussion below.

#1 – Revenues and Gains

The entity’s revenue and gains need to be closed at the end of every year. Thus, accounts like sales accounts, service revenue accounts, interest income account, dividend income account, and profit on the sale of debit details of a company’s assets. Examples include short-term Investments, prepaid expenses, supplies, land, equipment, furniture & fixtures, discount income account, etc. are the type of temporary accounts covered under revenue and gains.

#2 – Losses and Expenses

Expenses are the core of all businesses. Hence, as discussed in revenue, expenses must be precise at the end of the year to check the net outflow of the cash for the given period. Thus, accounts like the cost of sales account, salaries expense account, interest expense account, delivery expense account, purchase account, etc., are the type of temporary accounts included under losses and gains.

#3 – Drawing Account or Income Summary Account

The income statement summary is transferred to the capital account in sole proprietorship and partnership at the end of the year. The income statement summary is credited to reserves and surplus in a dividend. Without these entries, books cannot be closed. Therefore, entries with such adjustments are considered closing entries and passed into the temporary accounts.

Examples

Below are a few scenarios to help us understand the temporary account numbers. Let us discuss different scenarios through the discussions below.

Example #1

- ABC Ltd. recorded revenues of $600,000 for the financial year 2017. In 2018, it recorded $400,000 worth of gains and $800,000 in 2019.

- The company will use a temporary account to represent the revenue annually to display in financial statements. If the record were not closed, the total earnings would be $1800,000.

- The company can be visible as profitable due to total turnover. Therefore, that cannot always be good because three years’ worth of revenues cannot be clubbed to measure the business’s solvency. For the proper computation of any year’s profit and expenses, the temporary account must be created and closed adequately at the end of the year.

Example #2

- Let us take the example of retained earnings. Retained earnings show the company’s accumulated gains or losses over time. Every year, at the end of the year, the balances of income and expense accounts are transferred to the income statement and then squared off against the income summary account, bypassing the closing entries.

- Once the accounting process is completed, books are closed by transferring the surplus/losses to the retained earning account. Ledger reserves and surplus will not be closed at the end of a period as the exact nature is permanent. Instead, it contains a balance that carries forward to the next year and later discloses its past incomes and losses.

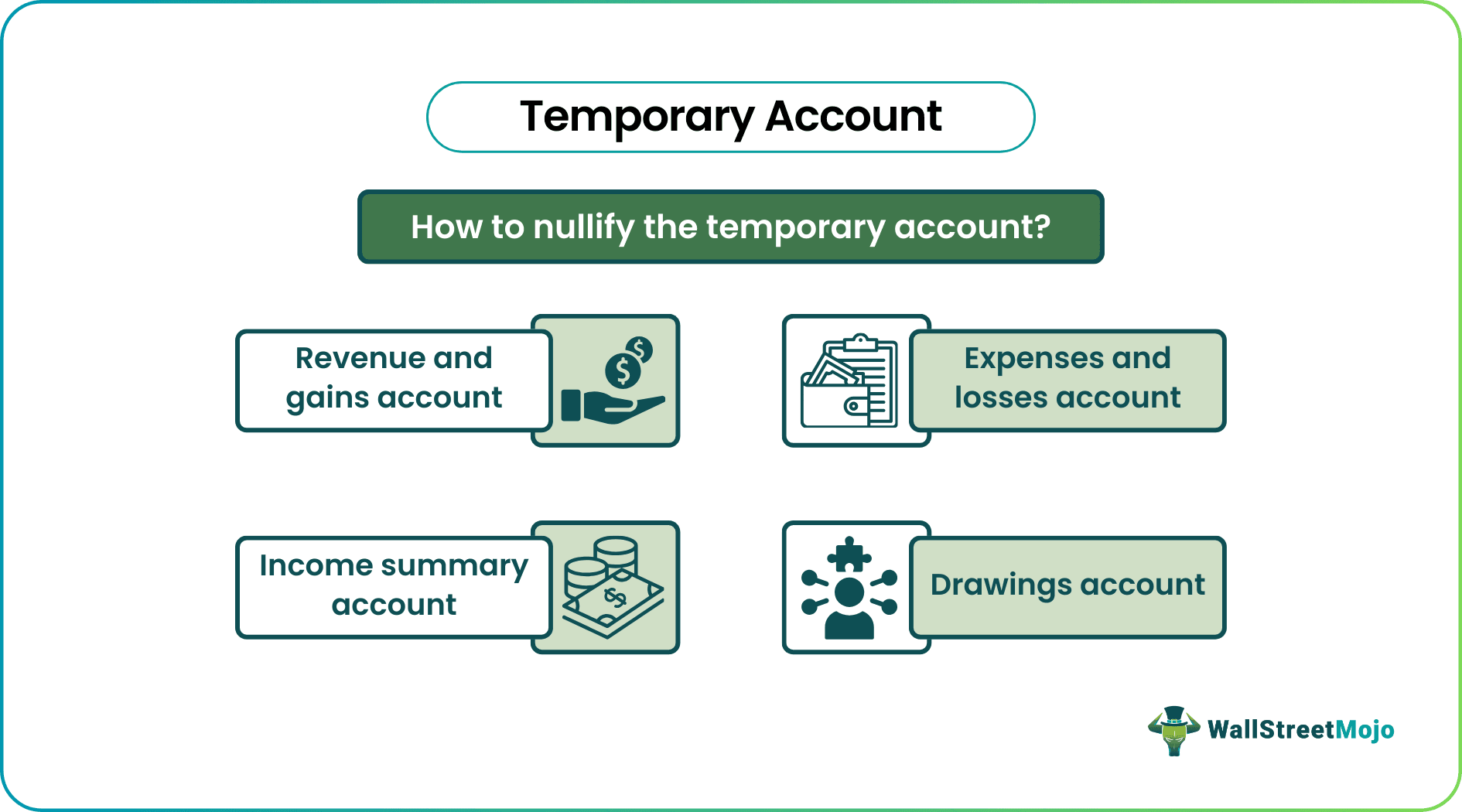

How To Close?

It is always mandatory to close all temporary accounts and record the net change to the owner’s capital account. To do this, pass the journal entries and post the same to respective ledgers balancing the same, and then pass closing entries for all temporary accounts. Finally, an income summary account is prepared to show the summary of revenue and expense accounts and discloses the profits and losses of the entity for the given period.

Below are the steps to be followed to close these accounts: –

- Revenue and gains account – Step one is to square off this account. It includes transferring the amount of the revenue account to the income summary account on the debit side.

- Expenses and losses account – Step two is to square off the expenses and losses. It includes transferring the amount of the cost account to the income summary account on the credit side.

- Income summary account – Step three is to square off the income summary. The amount of the income summary is expenses and revenue transferred to the capital account.

- Drawings account – The last step is to square off the drawings account. The amount in the drawings account is transferred to the capital account or the retained earnings account.

Temporary Account Vs Permanent Account

| Closure of account | It gets closed at the end of every year. | Permanent Account |

|---|---|---|

| Income statement vs. balance sheet | All the income statement accounts are temporary. | All the balance sheet accounts are permanent. |

| Carry forward balances | The balances of temporary accounts are not carried forward to the following year. | The balances of permanent accounts are carried forward to the following year. |

| Brought forward balances | Balances are not carried forward. Therefore, no credits were brought forward. | The permanent account may or may not have brought forward credits. |

| Also known as | They are also known as nominal accounts. | They are also known as permanent accounts. |

| Post-closing trial balance existence | After preparing the trial balance, all such accounts will be zero. | As credits are carried forward, there will be only a permanent account, post-closing trial balance. |

| Examples | Sales account, purchase account, expense account, income account, etc. | Asset account, liability account, capital account, etc. |

Frequently Asked Questions (FAQs)

Which is not a temporary account?

Revenue, expense, and profit and loss accounts are temporary accounts. In addition, in the case of a sole proprietorship or partnership, one may also have a temporary drawing or withdrawal account.

What is the difference between a permanent and temporary account?

Permanent accounts are different from temporary accounts. Temporary accounts display accomplishments across a specific duration. At the same time, permanent accounts show proceeding business progress.

Which is not a temporary account in accounting?

A drawings account is a corporation’s dividend account where the money is distributed to the owners. As it is not a temporary account, it is transferred to the capital account instead of the income summary through an amount credit.

Why are temporary accounts closed?

A temporary account is closed at the end of every accounting period and begins a new period with a zero balance. It is closed to safeguard the balances from being mixed with the subsequent accounting period balances.

Recommended Articles

This article is a guide to what is a Temporary Account. Here, we explain its examples, vs permanent accounts, along with how to close it. You can learn more about accounting from the following articles: –