Part of our Accounting Concepts guide

What Is A Cost Basis?

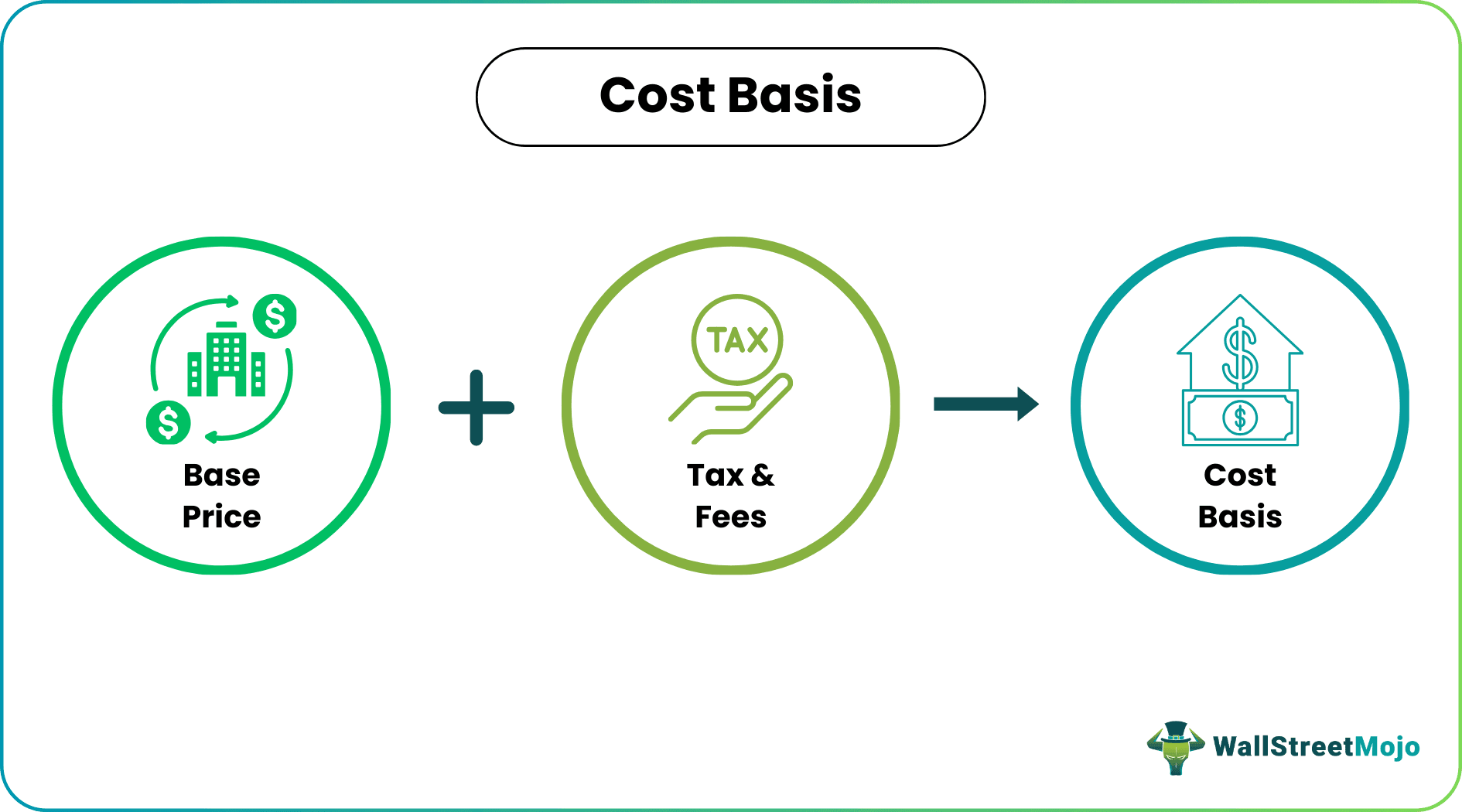

Cost basis means the at-cost purchase price of an asset, including the incidental expenses, which is used to calculate tax arising from the gain or loss of an asset due to differences between the cost and current market price. The cost basis calculator is used to ascertain the capital gains of an asset after all tax deductions.

It represents the portion of the shareholder’s investment in the fund in the case of mutual funds. It is also adjusted if the investor decides to reinvest the amount received as dividends from the shares they have invested. It is also often referred to as a tax basis and is used in different industries such as real estate, stock market, mutual funds, and bond markets.

Cost Basis Explained

Cost basis is the initial amount of investment paid to purchase an asset in the stock market, real estate, mutual funds or bond market. If the investor sells the asset for an amount above their cost basis, they have secured a capital gain. Otherwise, it must be accounted as a capital loss.

It is also important to note that the cost basis stocks are the price after a few adjustments are made depending on the actions of the company. These adjustments can be mergers, dividend distribution, stock splits, wash sales, or even bankruptcies.

Moreover, if an investor does not purchase their mutual funds directly, the broker’s fee and commissions. These costs must be accounted for accordingly.

Investors are advised to determine their initial investment amount including taxes and commissions, if any. Secondly, it is important to determine the cost of each share from their investment. Most importantly, they must inculcate an inventory costings method such as LIFO, FIFO, or weighted average method to determine the changes in their portfolio within the accounting period.

It is important to decide on a method and stick to the same method of maintaining inventory throughout the accounting period to ensure there are no lapses or entries that are accounted for differently.

Therefore, The method of basis cost recording has to decide at the beginning of the financial year and consistently has to follow throughout the year. The company requires maintaining proper documentation for all purchases for quality and adequate control purposes.

Formula

The cost basis calculator followed by accounting standard and cost of an asset generally includes the following Cost = Purchase Price + Installation expenses incidental expenses related to the purchase of an asset + Duty + Fee.

How To Calculate?

Cost basis can be determined differently for different asset classes. Let us understand how to calculate cost basis stocks and other such assets through the discussion below.

#1 – Fixed Asset Purchase

The cost basis is calculated by the purchase price, installation expenses, expenses incurred for bringing an asset to its location, and conditions. For example, X purchases machinery worth $ 10000, commission paid of $ 200. Transportation expenses are $ 100. The repair cost is $ 100; installation labor charges $ 100, duty, and taxes $50. The total cost of a fixed asset will be

$10000+$200+$100+$100+$100+$50=$ 10550.

#2 – Inventory

Cost is calculated differently for different levels of stock, such as For raw materials, the cost is calculated on the purchase price of materials. For Finished stock, the cost is calculated by adding raw materials and conversion costs.

#3 – Investment

- The long term investment is recorded on cost, and short term investment is recorded on cost or net realizable value whichever is lower.

- Asset acquired by Gift, under this situation, cost of an asset is calculated on the fair value of the asset as suggested in Accounting Standard, which is relevant for income tax purposes to calculate the property tax of the asset.

- Suppose the fair value of the building is $ 200000, and it is transferred as a gift which has Nil consideration. Property tax is 10%.

- Property tax will calculate on fair value, i.e., $ 200000 by the income tax department, and the amount will be 10% of $ 200000 = $ 20000.

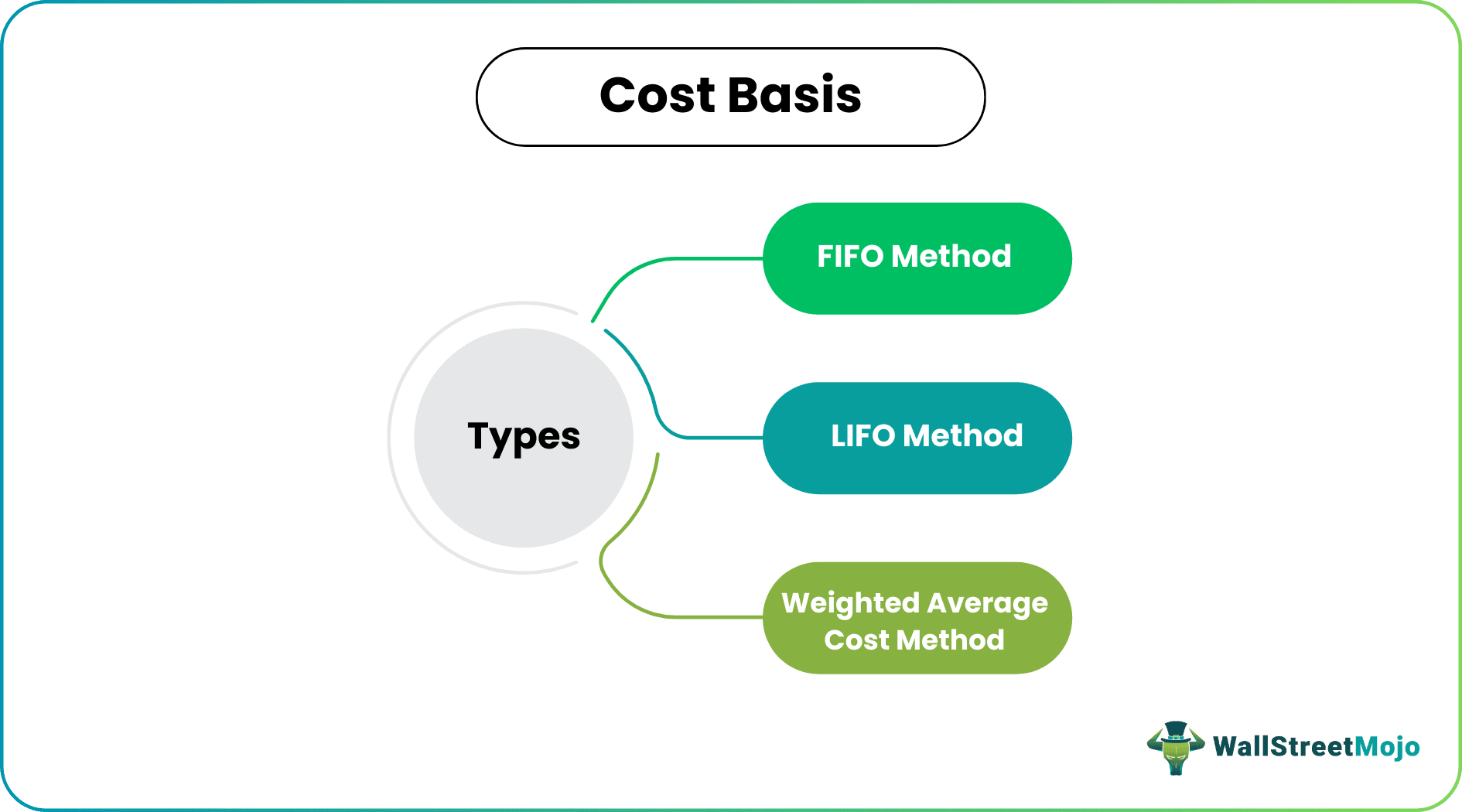

Methods

There are three major types of cost basis methods that are followed in an organization. Let us understand each of them in detail through the discussion below.

#1 – FIFO Method

- This costing method refers to when stock is sold then we have a sale the first stock which acquired, it is known as the first in first out inventory

- Suppose X purchased 10 stocks on 1st January and again on 2nd February 20 stocks. X sold 5 stocks on 3rd March. The organization will consider 5 stocks sold out of 1st January for recording purposes. This method generally is followed in perishable goods.

#2 – LIFO Method

This method is also known as last in first out accounting, and let’s consider the above example under this method organization will consider 5 stocks sold out of 2nd February.

#3 – Weighted Average Cost Method

This method records the value of the stock on an average cost basis. This method generally followed in mutual funds. Suppose 4 units purchased @$10 and 6 units purchased at $20.

The calculation will be [(4×$10)+(6× $20)]/4 units + 6 units = $16 average cost per unit.

Advantages

Let us understand the advantages of using the cost basis calculator for accounting investments through the points below.

- Cost basis important for tax purposes. For example, 100 shares purchased at $ 10 each, and the current market price per share is $ 50. Capital gains are 100 shares× ($ 50-$10) =$400

- The cost method is beneficial for financial reporting purposes. Otherwise, it would be difficult for recording for those assets which are volatile. E.g., the market price of the share is volatile, and it changes every second if we start recording the transaction based on market price, then it would be difficult to maintain books according to such change.

- Cost basis differentiates which expenses should be added to cost or not. For example, as per accounting standard, it is mentioned that which expense will be included in the cost of the asset.

- Mr. X purchases a machine of $ 15000 and pays installation, brokerage, duty, fee, totaling $ 5000. He also pays some expenses not related to the asset of $ 500.

In this case, as per cost basis, the cost of assets will be $ 20000 because it is related to the purchase of assets. However, it will not include $ 500 to the cost of the asset because it is not related to the asset.

- Cost Basis is essential to maintain tax balance across the country; otherwise, tax on short term capital gains will be as high as the income tax rate, which carries a lower tax rate as compared to income tax rates.

- Under the cost basis price of stock remain the same even if the share is split, which avoids unnecessary recording. For example, X purchased 100 shares at $1000 @ 10 each. Now the share split into 50 shares. The initial cost of $ 1000 will remain the same, but now the price for each share will be $ 20 instead of $ 10 each.

Disadvantages

Despite the advantages mentioned above, there are a few factors from the other end of the spectrum that prove to be hassles for investors. Let us understand the disadvantages of cost basis stocks through the discussion below.

- A cost basis does not indicate the actual price of the asset.

- Suppose X purchased an asset which of $ 10000 and the same asset purchased by Y at $ 12000

- As we can see, the cost of the same asset different is for X and Y for recording purposes.

- It is challenging for a large organization to identify and track the record of each item purchase date and which stock was purchased is to consider for sale.

- Under Cost basis, the sale price of a stock one of an organization can be cost price for another organization.

- For example, X sold stock to Y at $ 1000, which is the cost for Y. However, it is the sale price for X. Due to this reason how one can identify what the actual cost of a stock is.

Recommended Articles

This article has been a guide to What is a Cost Basis. Here we explain the Cost Basis methods how to calculate it, and the advantages and disadvantages. You can learn more about from the following articles –