Part of our Descriptive Statistics guide

What Is Coefficient Of Kurtosis?

The Coefficient Of Kurtosis is a statistical measure that describes the distribution of data points in a dataset. It quantifies whether the data has heavier or lighter tails compared to a normal distribution, thus identifying whether the sample distribution is leptokurtic, mesokurtic, or platykurtic. In the field of finance, it helps in gauging the financial risks associated with the investments.

In simple terms, it is a statistical tool that analyzes whether the sample data significantly deviates from the normal curve and to what degree. A positive kurtosis suggests a distribution with heavier tails and a sharper peak, while a negative kurtosis indicates lighter tails and a flatter peak in comparison to a normal distribution, which has a kurtosis of 3.

Key Takeaways

- The coefficient of kurtosis is a statistical measure that describes the distribution of data points in a dataset by gauging the tailedness of the distribution compared to that of a normal distribution (i.e., 3).

- It is denoted by Beta 2 (β2) and mathematically represented as β2 = µ4/(µ2)2, where µ4 represents the 4th moment about the mean, and µ2 denotes the 2nd moment about the mean.

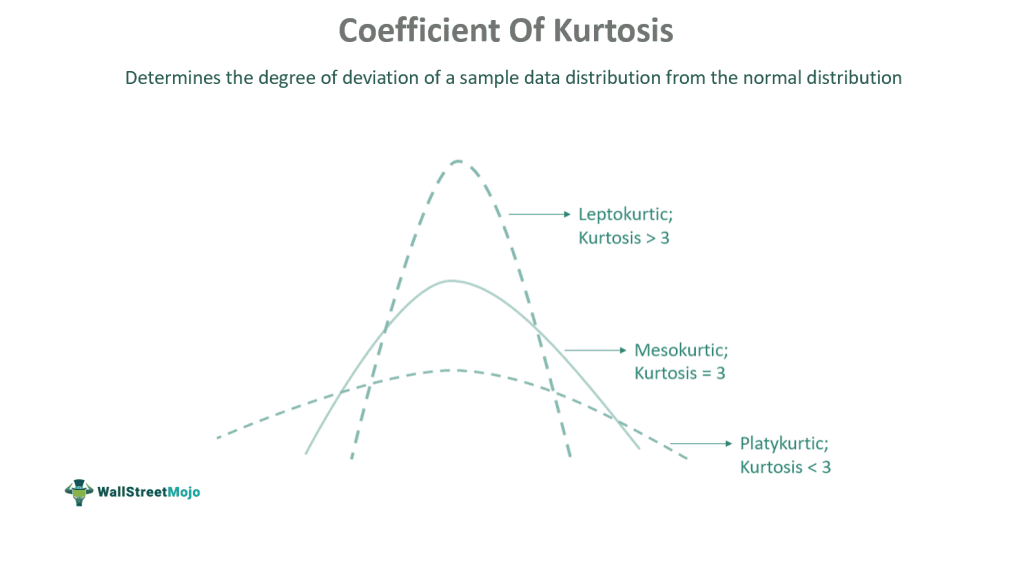

- The sample data is said to be leptokurtic if the kurtosis is more than three or positive; mesokurtic if it is equal to 3 or neutral; or platykurtic if it is less than three or negative.

Coefficient Of Kurtosis Explained

The coefficient of kurtosis is a measure of probability distribution shape introduced by Karl Pearson in 1905. It finds practical applications in diverse fields such as economics, finance, insurance, environmental science, quality control, and biology. In this approach, the sample kurtosis is equal to the expected kurtosis of a normal distribution, which is 3. This comparison helps determine whether the sample data significantly deviates from a normal distribution in terms of kurtosis, indicating the presence of heavy or light tails. When assessing the significance of the moment coefficient of kurtosis in statistical analysis, researchers often employ various hypotheses and statistical tests based on the type of data and purpose of the analysis.

Its application empowers professionals to make informed decisions, manage risks, and enhance processes across various disciplines. Financial analysts use this coefficient to model risks for strategic investment and portfolio management. High kurtosis in asset returns signifies fatter tails, indicating elevated risks during extreme market events. Moreover, economists study income distributions through this measure.

Since a high kurtosis coefficient in income data implies significant deviations from the mean, this influences economic policies and social welfare programs targeting income disparities. Similarly, actuaries assess insurance risks in claims analysis. Distributions with high kurtosis suggest a likelihood of extreme claims, impacting insurance premiums and the company’s financial planning.

Formula

The coefficient of the kurtosis formula measures the “tailedness” of a distribution, indicating its shape and the presence of outliers. There are different formulations, such as excess kurtosis, which subtracts three from the standard kurtosis value. The formula for kurtosis is:

Here,

We need to compare the kurtosis of the sample distribution with three, which is the kurtosis of the normal distribution, to get the coefficient, i.e., β2-3.

Examples

Analysts use the coefficient of kurtosis calculator alongside other statistical measures to assess dataset characteristics. Let us take some examples with calculations to understand the concept better:

Example #1

Find the coefficient of kurtosis from the following sample data:

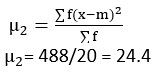

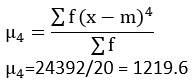

| x | f | fx | x-m (where m is 10) | (x-m)2 | f(x-m)2 | (x-m)4 | f(x-m)4 |

|---|---|---|---|---|---|---|---|

| 5 | 5 | 25 | -5 | 25 | 125 | 625 | 3125 |

| 7 | 2 | 14 | -3 | 9 | 18 | 81 | 162 |

| 10 | 7 | 70 | 0 | 0 | 0 | 0 | 0 |

| 15 | 1 | 15 | 5 | 25 | 25 | 625 | 625 |

| 18 | 5 | 90 | 8 | 64 | 320 | 4096 | 20480 |

| 20 | 214 | 123 | 488 | 24392 |

Therefore,

A platykurtic distribution with a beta-value of less than three (β2) is characterized by this sample having thinly tailed curves.

Example #2

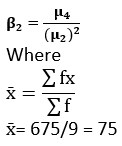

Now, let us apply the coefficient of the kurtosis formula to grouped data. Suppose the stock price volatility of an asset is as follows:

| Stock Price (x in $) | f | x | fx | x-m (wherem is 75) | (x-m)2 | f(x-m)2 | (x-m)4 | f(x-m)4 |

|---|---|---|---|---|---|---|---|---|

| 50 – 60 | 1 | 55 | 55 | -20 | 400 | 400 | 160000 | 160000 |

| 60 – 70 | 3 | 65 | 195 | -10 | 100 | 300 | 10000 | 30000 |

| 70 – 80 | 2 | 75 | 150 | 0 | 0 | 0 | 0 | 0 |

| 80 – 90 | 1 | 85 | 85 | 10 | 100 | 100 | 10000 | 10000 |

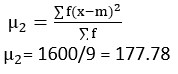

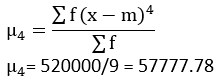

| 90 – 100 | 2 | 95 | 190 | 20 | 400 | 800 | 160000 | 320000 |

| 9 | 675 | 1000 | 1600 | 520000 |

Therefore,

The distribution of this sample is platykurtic and has a lower tail thickness since its kurtosis value is less than three, which is characteristic of a normal distribution.

Interpretation

The moment coefficient of kurtosis measures how the data points are distributed in the tails compared to a normal distribution, which is 3. The following are the three possibilities when this measure is applied to a given sample distribution:

- Positive Kurtosis or Leptokurtic (Coefficient > 3): If the coefficient is more significant than 3, it indicates that the data distribution has heavier tails and a sharper peak than a normal distribution. This suggests that the data has more outliers and is more prone to extreme values than a normal distribution.

- Normal Kurtosis or Mesokurtic (Coefficient = 0): The data is considered to be mesokurtic or to have a normal distribution if the coefficient is 0.

- Negative Kurtosis or Platykurtic (Coefficient < 3): If the coefficient is less than 3, it means that the data distribution has lighter tails and a flatter peak than a normal distribution. This suggests that the data has fewer outliers and is less prone to extreme values than a normal distribution.

Frequently Asked Questions (FAQs)

How do we find the percentile coefficient of kurtosis?

To calculate the percentile coefficient of kurtosis, we can use the given formula:

Kp = QD/(P90-P10)

Where:

• QD is the semi-interquartile range, which is equal to (Q3 – Q1) / 2;

• P90 is the 90th percentile;

• P10 is the 10th percentile;

This measure helps to understand the data distribution relative to a normal distribution in terms of shape.

What is the limitation of the coefficient of kurtosis?

The coefficient of kurtosis has some drawbacks, as discussed below:

• Its accuracy depends on the sample size.

• An extreme value or outliers can affect the outcome.

• Its interpretation is difficult as the direction of the kurtosis can be positive or negative.

• Difficult to use by individuals without a solid statistical background.

• It is based on the fourth moment of the distribution, which means it depends on higher-order moments.

What does the coefficient of kurtosis come from?

The kurtosis ranges between 1 and infinity; hence, the coefficient of kurtosis can be from -2 to infinity.

Recommended Articles

This article has been a guide to what is Coefficient Of Kurtosis. Here, we explain the concept in detail with its formula, examples, and interpretation. You may also find some useful articles here –

Recommended Articles

Continue with these closely related articles from the same guide.