Loan Servicing Definition

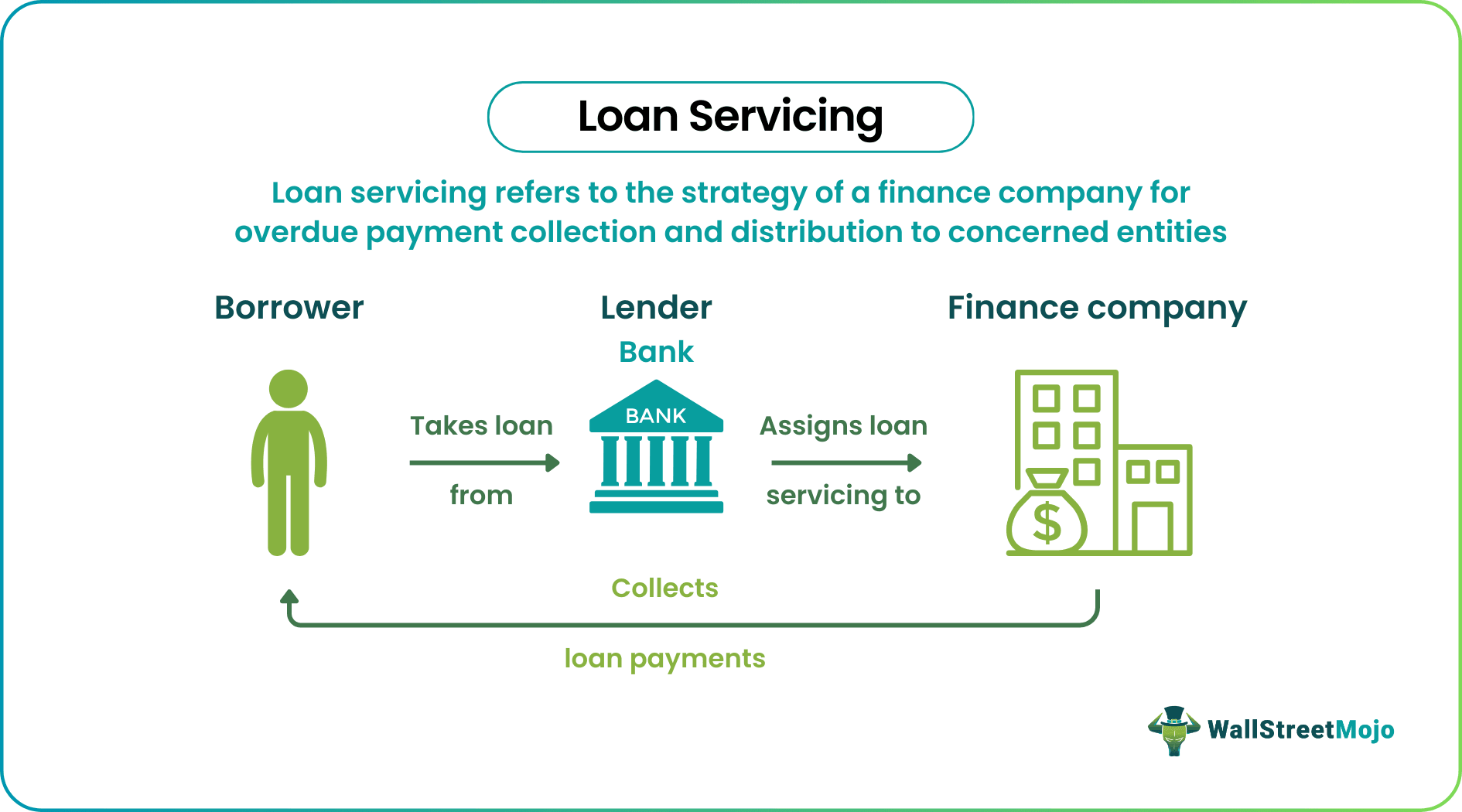

Loan servicing is the procedure followed by a consumer finance company to recover the outstanding principal, interest, and insurance payments. It aids in ensuring swift and timely loan payment via a fully transparent and legal system. Moreover, the national student loan servicing providers are specialists in efficient loan handling.

This comprises dispatching monthly account balances, payment processing, answering requests, and preserving collection records. Although it serves all kinds of loans, mortgages are the most prevalent. It certainly helps foster healthy relationships between the borrower and the lender.

- Loan servicing refers to delayed payment collection on the loan and further dispersion to concerned parties.

- The loan servicing specialist manages prompt debt payment collection and, in turn, receives a minimum proportion of the compensation to be paid by the borrower.

- It assists in preventing complex loans and fostering a healthy relationship between the defaulter and financial institution. Though applied to every type of loan, mortgages are the most used.

- It incorporates payment processing, sending monthly balance statements, maintaining bill records, and replying to requests.

Loan Servicing Explained

Loan servicing entails the collection of payable working capital and any late fee. Formerly a basic banking segment, it has become an independent occupation since servicing delinquent loans became less advantageous for banks. Moreover, the servicers must certainly obey the added statutory and federal requisites.

The firm or individual behind servicing the loan (servicer) dispenses the amount to an array of various parties perhaps linked to the loan,

- Mortgage guarantors and agents acquire remittance fees.

- Mortgagees or lenders with mortgage-backed securities (MBS) accrue principal or interest expenses.

According to the loan, its conditions, and involved investors, the amount may also incorporate term or loan restructuring centers, delinquency monitors, and foreclosure executors. Moreover, the loan servicing providers obtain salaries to confirm prompt payment distribution to appropriate parties.

The loan servicers receive a tiny percentage of the consistent loan payment compensated by the borrower. Additionally, they supervise escrow accounts to reimburse escrow payments for yearly owed insurance and taxes.

So, they must,

- Apply payment to the loan on the same date it is derived.

- Notify investors regarding missed payments.

- Report to them the present payment amount.

- Offer them comprehensive information about their payment history.

Most banks generate new loans and pass off servicing responsibilities to different financial institutions, with servicing as among their core competencies. Furthermore, mortgage servicers forward the annual statement to investors outlining their real estate tax payments, account status, homeowners’ insurance, and other actions on the account.

Examples

Now, let’s go through some national loan servicing examples.

Example #1

Say Victor (borrower) has a federal student loan and the loan servicer acts as a middleman between him and the federal government (lender). So, the servicer is authorized to collect loan bills and track whether or not Victor pays them on time.

The loan servicing specialist may also assist in determining the eligibility criteria for the administration’s income-driven repayment policies. If Victor decides to switch, the specialist will process his application and yearly income recertification (required for eligibility).

Additionally, the servicer also helps Victor with loan payments personalization, the processing of requests for forbearance or deferment, and certification for loan burden reduction.

Example #2

The US education department has commenced a critical transformation in servicing loans for students. Moreover, the largest financial aid provider for college in the US, namely, The Federal Student Aid, has posted this petition for the Unified Servicing and Data Solution (USDS).

This will supposedly act as the continuing servicing solution for the federal student loan defaulters. Moreover, the new servicing scheme will,

- Provide the student loan payers with complete student loan management via StudentAid.gov

- Substitute legacy student loan servicing agreements for both federally-handled FFELP loans and direct loans

- Enhance answerability for loan servicers by measurable standards

- Offer a smoother transition throughout loan account transfers, and

- Utilize loan servicers’ supervision to diminish loan default and student delinquency.

Benefits

To clarify, here are the perks offered by loan servicing providers:

- Lenders depend on the loan servicers to suggest and process post-closing incidents, including lease approvals, assumptions, land planning affairs, and transfers. Therefore, it certainly assists offer guidance and conversation on request processing criteria and the information required.

- These servicers with strong mortgagor relations can avert complicated loans and reduce losses by consultation and reporting.

- Generally, servicing connections sustain the deep ties between lenders and non-payers built over time.

- Their impressive network of relationships can manage any probable requests or issues that might occur throughout the loan’s lifespan.

- Above all, loan servicers with strong lender relations may access relevant individuals behind crucial decisions. Therefore, it saves the annoyance of navigating complicated firms and defaulters’ time.

- In case of a serious problem, the professional loan servicers may connect with vetted specialists (investment brokers, attorneys, environmental consultants, and contractors). This aids in getting an instant and competent response affordably.

Most importantly, it assists in decreasing the overhead costs of the company to a great extent.

Frequently Asked Questions (FAQs)

What Does Loan Servicing Mean?

Loan servicing is the approach of a finance company to get payments, dividends, and (if required) escrow from loan defaulters. Moreover, the national loan servicing covers periodic payment collection, dispatching monthly bill statements, and tax collection and payment. Servicing mortgage loans is the most common type among all other loans.

What Does a Loan Servicing Specialist Do?

A loan servicing specialist processes and approves the latest loan applications and handles current loan accounts. Also, these experts supervise applications on intake, claim data verification, and review the documents. They process the approval decisions and establish the earliest record of a new loan into the system.

How To Become a Loan Servicing Specialist?

A high school diploma and know-how of loan application procedures are required to become a loan servicing specialist. Furthermore, most recruiters prefer candidates with a bachelor’s or associate degree in finance or related subject possessing consumer service skills.

Recommended Articles

This article has been a guide to Loan Servicing and its Definition. Here we explain loan servicing (national & student) specialist providers & its benefits. You can learn more about finance from the following articles: –