Table of Contents

What Is Village Savings And Loan Association (VSLAS)?

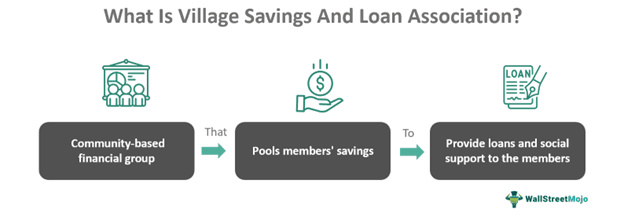

The Village Savings and Loan Association is a social saving group model. It is an association comprised of 10-25 members who are individuals from a community. These members contribute money periodically as savings and then lend as small loans to each other.

VSLAS serves as a driver of economic justice and community resilience. It facilitates a sense of community and togetherness and promotes the habit of savings. They decrease the challenges faced by low-income groups regarding food, healthcare, and income. They have proven beneficial, especially for women from vulnerable sections of society, by empowering them financially.

Key Takeaways

- Village Savings and Loan Association is an association where the members of the group save small amounts of money and form a corpus,

- which is later used to lend money to other members in need. The group members decide the operations of village savings and loan associations.

- They positively impact society, especially in cases of vulnerable sections, which include women. They provide access to finance, promote financial inclusion, increase income opportunities, and tackle social evils. Etc.

- They, however, have certain disadvantages, such as having insufficient or low corpus, lack of training for members, irregular saving habits, etc.

Village Savings And Loan Association Explained

Village Savings and Loan Association is a community group that focuses its efforts on financial empowerment. It is a small group of individuals, typically in numbers of 10-25. In VSLA, the members of the group save small amounts of money and significant amounts through joint efforts. They have periodic cycles that typically last a year, and at the end, the accumulated savings and interest made after lending are proportionally shared among the members.

In detail, the VSLA's group number differs between different associations. However, irrespective of the number, the group elects a president, and every week, the president collects an amount (as decided by the group) from each member. The collected amount is handed over to a member. This member may have requested money, or a member may have requested it according to their turn as predetermined. This handing over is the lending activity, and the amount is lent at a small rate (as decided by the group). The loans are paid off within the designated period, and the interest from lending and remaining savings are proportionally shared between members.

They are established with the aim of social welfare through community efforts. The groups work towards financial empowerment, reducing poverty and gender inequality, improving nutrition, etc.

Objectives

The general objectives of the VSLA are listed down below:

- The vulnerable sections, especially women, become financially literate, and they are empowered to be involved in income-generating activities.

- Empower the participants to become independent.

- To increase access to finance, control available resources, and collectively overcome financial and social barriers.

- Induce social changes such as financial empowerment of women, reduce gender inequality and poverty, and improve individual and social well-being.

Examples

Let us look into a few examples to understand VSLA's:

Example #1

Let's imagine a community, XYZ, located in Peru. XYZ is a community that consists mainly of fishermen. They belong to the lower income group. The women in the region decide to come together and form a VSLA. They were 15 in number. They decided to establish the group and elected a senior member as their president. The president's main job is to collect a fixed amount, say 5$ every week, to create a corpus. They had decided that their VSLA cycle would be nine months, and after nine months, they would give out the entire amount as a loan for one member at 5% interest. Let's say 36 weeks are averaging (4 weeks a month), and if each member contributes 5$, it will amount to 75$ (15*5) a week of corpus, and at the end of the nine months, they will have $2700.

This is a significant amount, considering they are from a poor community. The amount that could have been spent on unnecessary items is now saved and can be used to fulfill the needs of the community.

Example #2

The International Journal of Innovative Science, Engineering & Technology published a paper in 2022 regarding Village Savings and Loan Associations (VSLAs) in Uganda. The study concludes that the VSLAs have significantly and positively impacted the lives of people with low incomes. The community saved small amounts and invested them in small income-generating projects, which indeed increased their income levels (albeit slightly). This boosted the overall welfare of the community. The women of the groups had opportunities to be involved in the affairs of the associations, empowering them.

Advantages And Disadvantages

Given below are some of the advantages and disadvantages of the VSLA's

Advantages

- Access to finance: VSLAs promote savings, and the pooled finance is commonly accessible for all members, often given on a priority basis. The vulnerable sections of people get an opportunity to cover their daily needs, meet their expenses, and recover from debt through this. It saves the community members from the hassle of visiting a financial institution that requires mortgage-able assets and documents and involves a lot of time.

- Financial inclusion: There may be individuals, especially in lower-income or least-developed nations, who may not be a part of the formal banking system. VLSAs are a way to make them part of a system and introduce them to managing their finances.

- Innovation and opportunities: The members can use the loan amount taken out to develop small businesses or invest in innovative initiatives. This could be their only source or additional source of income.

- Empowerment: The vulnerable sections, especially women, are empowered through this small community act. Household work is often not recognized as productive work and is neglected as it has economic value. This prevents them from being included in the decision-making process.

- Tackling social evils: VSLAs work efficiently in lower-income groups and vulnerable sectors of society. They are in need because of the community's poor financial status. Social evils such as child labor are often a result of poverty.

Disadvantages

- Low/ poor savings culture: The members of the VSLAs are from the low-income section of society. They may only sometimes be able to afford vast amounts of savings or make regular, continuous contributions. This results in a poor savings culture.

- Inadequate loan funds: This is a result of a poor saving culture. When members only regularly contribute or contribute a significantly lower amount each time, the corpus available for lending to other members increases.

- Failure of members to pay back: Another issue faced by the VSLAs is the issue of members paying back the loan amount. The vulnerable sections of members may only sometimes have the funds to repay the loan with interest, and this negatively affects the other members of the group.

- Lack of support from financial institutions: It proves to be a hindrance in the expansion of their operations. This is because the majority of the community's funds come from the small savings they gather, and more is needed to support their proper functioning.

- Inadequate training of members: The VSLAs may be a good point for financial inclusion, but they may need to answer the question of financial sustainability. Even if members try new opportunities and start new ventures, they often need to gain the skills or knowledge to move forward with the idea and sustain it for longer terms.