What Is Conforming Loan?

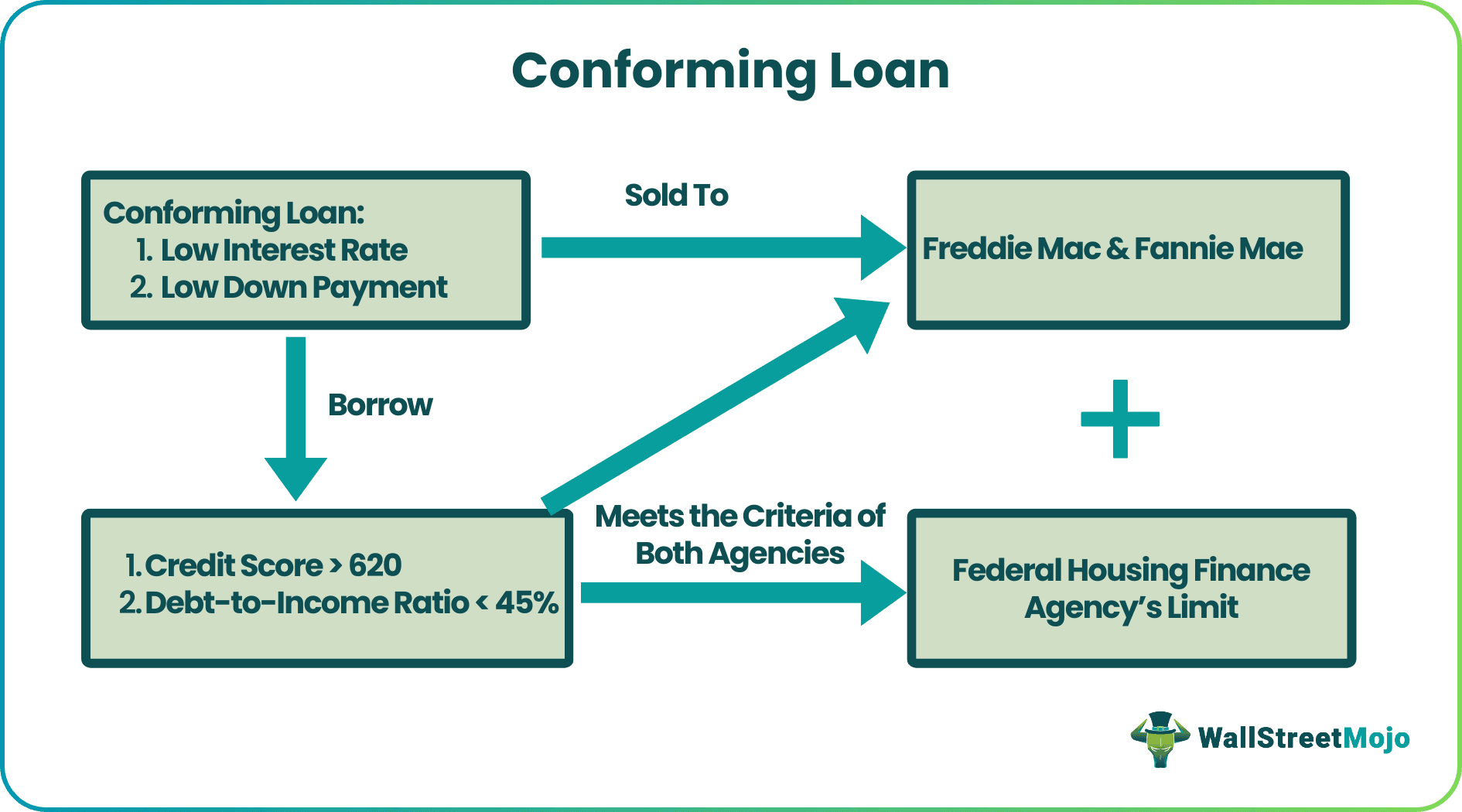

A conforming loan refers to a mortgage loan that matches the criteria set by Freddie Mac and Fannie Mae and is within the limit given by Federal Housing Finance Agency. These loans have low-interest rates and are suitable for people with good creditworthiness.

The criteria refer to the borrower’s eligibility standards, the down payment amount, and the total loan size. In addition, the loan should meet the Freddie Mac and Fannie Mae standards meaning they can purchase it, issue securities against them, and sell the securities to investors. These loans are a great start if someone is looking for a good finance option.

- A conforming loan is a type of debt where the amount has to meet the Freddie Mac and Fannie Mae standards and the limit that the Federal Housing Finance Agency has set.

- The conforming loan rates are low and are suitable for people with high creditworthiness.

- The criteria over here mean the down payment amount, the loan size, and the borrower’s eligibility.

- Freddie Mac and Fannie Mae purchase the loans and issue mortgage-backed securities against them to investors.

Conforming Loan Explained

A conforming loan meets the benchmark Freddie Mac and Fannie Mae set and the Federal Housing Finance Agency’s limit. They are suitable for borrowers with high credit and offer low-interest rates.

Lenders find it attractive and can sell it to Freddie Mac and Fannie Mae, who pack them to issue investors’ securities, ensuring steady funds supply for lenders. Federal Housing Finance Agency (FHFA) sets the conforming loan amount limit.

Freddie Mac and Fannie Mae are government-backed and rule the mortgage loan market. They do not provide mortgages by themselves. Instead, they insure the mortgages that the banks and other financial institutions offer. Thus, the lenders sell the loans and get funds, which helps them manage lenders to manage the risk and ensure a steady flow of funds for lending. But they have a monopoly in the US mortgage market despite the various federal regulations.

However, these agencies ensure a continuous liquidity supply for financial institutions. If the loans do not meet the necessary standards, they are non-conforming ones. Since the conforming loan rates are low and they also have low down payment facilities, they are easily affordable to borrowers.

Requirements

A loan to meet the conforming category should meet specific requirements as follows:

- The total amount should be within the limit given by FHFA, which is called the conforming loan limit (CLL)

- It should be eligible for purchase by Freddie Mac and Fannie Mae, government-backed agencies.

- The FHFA may change the CLL every year depending on the rise or fall of real estate prices in a particular city.

- If the conforming loan amount is above CLL, it is a jumbo loan with high rates and a higher down payment.

- The borrower’s loan-to-value, the loan amount divided by the value of collateral or property, should be good. Therefore, a lower ratio is better.

- A good (lower) debt-to-income ratio is essential.

- The borrower should have a good credit score and have the necessary documents.

- The mortgage should meet the conforming loan down payment criteria.

Limit

A mortgage-conforming loan has certain limits, as given below:

- In addition, the total loan amount is fixed by FHFA, which may change yearly depending on home prices.

- For most of the US, the limit is the same. However, the limit will be more for costlier cities like New York or San Francisco, which might be 150% more.

- Cities like Hawaii or Alaska have different provisions.

- For most borrowers, the credit score should be a minimum of 620.

- The debt-to-income ratio should ideally be less than 45%, but it may be more if the credit score is higher or if any other security is used to compensate for the risk.

Examples

Let us understand the topic with some examples.

Example #1

John, a borrower, is looking for a housing loan to buy an apartment in San Francisco. He had taken a housing loan for another house in the same area and had paid it on time. Thus, his credit score is good enough to get another loan quickly.

His house price is $1,200,000. But he decides to split his loan into two types: conforming, which has a low-interest rate, and the rest is non-conforming. He takes the conforming part from Rocket Mortgage for $700,000. He has to pay 18% as a down payment, which comes to $126,000.

The rest is $500,000, which he takes from a bank but has to pay a higher interest and a down payment of 20%.

In the above example, the loan benefits the borrower due to the low interest and down payment, provided they have a good credit score.

Example #2

It has been observed that the mortgage limit is suddenly increasing in the housing finance market, even though rates are already rising. Thus, borrowers will be able to afford a higher loan amount. However, analysis shows that there are other factors besides the rise in the limit that might affect the homebuyer’s affordability. It is the personal repayment capacity, the housing market in the area, and, more important, interest rates.

Benefits

The benefits of this type of loan are listed below:

- Low-interest rates – The conforming loan down payment amount is usually high for this type of loan, which reduces risk. Thus, the interest rate is lower than other types of loans.

- More savings – Saving is comparatively more because of the low-interest rate and the Equated Monthly Installments (EMI).

- Low down payment for first-time homebuyers – They allow a low down payment if the borrower buys a home for the first time.

- Profitable for lenders – This method benefits the lenders because they can sell it to Freddie Mac and Fannie Mae, government agencies that issue securities against them, which ensures a continuous supply of funds to lend.

- Low risk for lenders – It also helps reduce lending risk because the loan is given only to those with good credit ratings, thus ensuring they will not default.

- Only borrowers with a good credit score are eligible – The borrowing process should meet the Freddie Mac and Fannie Mae standards, which also means that the borrowers should have a good credit score.

Conforming Loan vs Non-Conforming Loan vs Jumbo Loan

A conforming loan meets the FHFA limit and Freddie Mac and Fannie Mae’s standards. A non-conforming loan does not meet the above criteria. If a borrower borrows an amount above the FHFA limit, it is a jumbo loan. However, they have some differences, as listed below:

| Conforming loans | Non-conforming loans | Jumbo loan |

|---|---|---|

| They meet the FHFA limit and Freddie Mac and Fannie Mae’s standards. | They do not meet the FHFA limit and Freddie Mac and Fannie Mae’s standards. | The amount of this type of loan is above the FHFA limit. |

| Their demand is very high. | They have a low demand. | They have a low demand. |

| The interest rate and the fee are low. | The interest rate and fee are high. | The interest rate and fee are high. |

| The lender’s risk is low. | The lender’s risk is high. | The lender’s risk is high. |

| Government agency backs it. | It is not a government agency-backed loan. | It is not a government agency-backed loan. |

| The amount may need to be more to meet the requirement. | It meets the requirement since the loan amount is more. | The amount is high. Thus, it meets the requirement. |

| The credit score has to be high. | Credit scores may be low. | Credit scores may be low. |

| Most lenders offer it due to low risk and low amount. | Few lenders offer it due to the high risk and amount. | Very few lenders offer it due to the high amount. |

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1. What is super conforming loan?

<p>It is a mortgage-conforming loan in which the FHFA has set a limit much higher than the average loan that is conforming because the areas where home buyers take such loans are costly, and they need to pay more to buy a house over there.</p>

2. Do conforming loans have prepayment penalties?

<p>There is no prepayment penalty for loans taken with the FHFA limit or meeting Fannie Mae’s and Freddie Mac’s standards. Therefore, the borrower can avoid a prepayment penalty if the loan falls under these categories.</p>

3. Where are high cost areas for conforming loans?

<p>A high-cost area in a home loan is when the loan amount is more than the median of the baseline limit, which is the limit divided by 115%. Thus, the loan will fall under the high-cost area if the home is costly compared to other places.</p>

4. Are conforming and conventional loans the same?

<p>All conforming loans are conventional, but all conventional loans may need to be conforming ones because a conventional loan may also be non-conforming with higher interest rates and more installment amounts.</p>

Recommended Articles

This has been a guide to what is Conforming Loan. We explain its requirements, limit, and benefits and comparison with the non-conforming and jumbo loan. You can learn more about financing from the following articles –