What Is Loan Syndication?

Loan syndication is a process where a group of lenders usually collaborates through an intermediary, which is a lead financial institution, or syndicate agent, which organizes and administers the transaction, including repayments, fees, etc., to provide financial requirements to a single more significant borrower (usually out of the capacity of a single lender) where the division of risk and returns takes place between each other is known as loan syndication.

In loan syndication, a group of banks provides loans jointly to a single borrower because one bank cannot meet the huge requirement of the borrower as it may be beyond its risk exposure. This type of loan syndication process is required by large companies working on a large project, which requires a huge amount of capital for their business.

- Loan syndication occurs when a lender group works with an intermediary, such as a lead financial institution or a syndicate agent, to organize and manage the transaction.

- It includes repayments, fees, and so on to provide financial needs to a single, more significant borrower (usually out of the capacity of a single lender), where the risk and returns are shared. This is known as loan syndication.

- The agent bank, participating bank, underwriting bank, and lead bank are the loan syndication participants.

How Does Loan Syndication Work?

In the process of loan syndication, several different lenders provide various portions of a loan. Every lender has a responsibility towards their share of the loan. Therefore, every lender has less risk due to sharing a loan (big amount) between more than one lender. As a result, banks or financial institutions profit from loan syndication.

It is used in corporate financing for buyouts or mergers and acquisitions because they require huge funds that one lender is usually unable to provide. Each lender has a liability up to the extent of their contribution. The terms and conditions are the same except for the collaterals.

Some risk managers manage the agreements which helps enforce the obligations of the contract. The entity’s legal department is also involved to enforce the obligations of the agreement.

The financial institutions that conduct and coordinate the loan syndication agreement are called syndicate agent. They control and manage the fees, loan monitoring and payments, compliance reports, etc. Since the loan amount is huge, the fees is also quite high, with a detailed reporting process and coordination.

Here is the method of loan syndication: –

- Initial discussions with promoters should be there.

- Then, a project assessment is required.

- Availability of alternatives for sources of funds needs to be done.

- Then, a preliminary discussion with lenders should be done.

- Then there is a requirement to prepare of loan application and follow up on it.

- Assisting in project appraisal by doing financial analysis.

- Lastly, one should obtain a Letter of Credit from a lending institution.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Features

The loan syndication agreement has the following features.

- Large amount.

- No separate agreement between an individual bank and the borrower.

- No ambiguity used to be there.

- The length of the contract is generally between 3 to 15 years.

- Low risk is found in loan syndication.

- Each bank is not necessarily to contribute an equal amount.

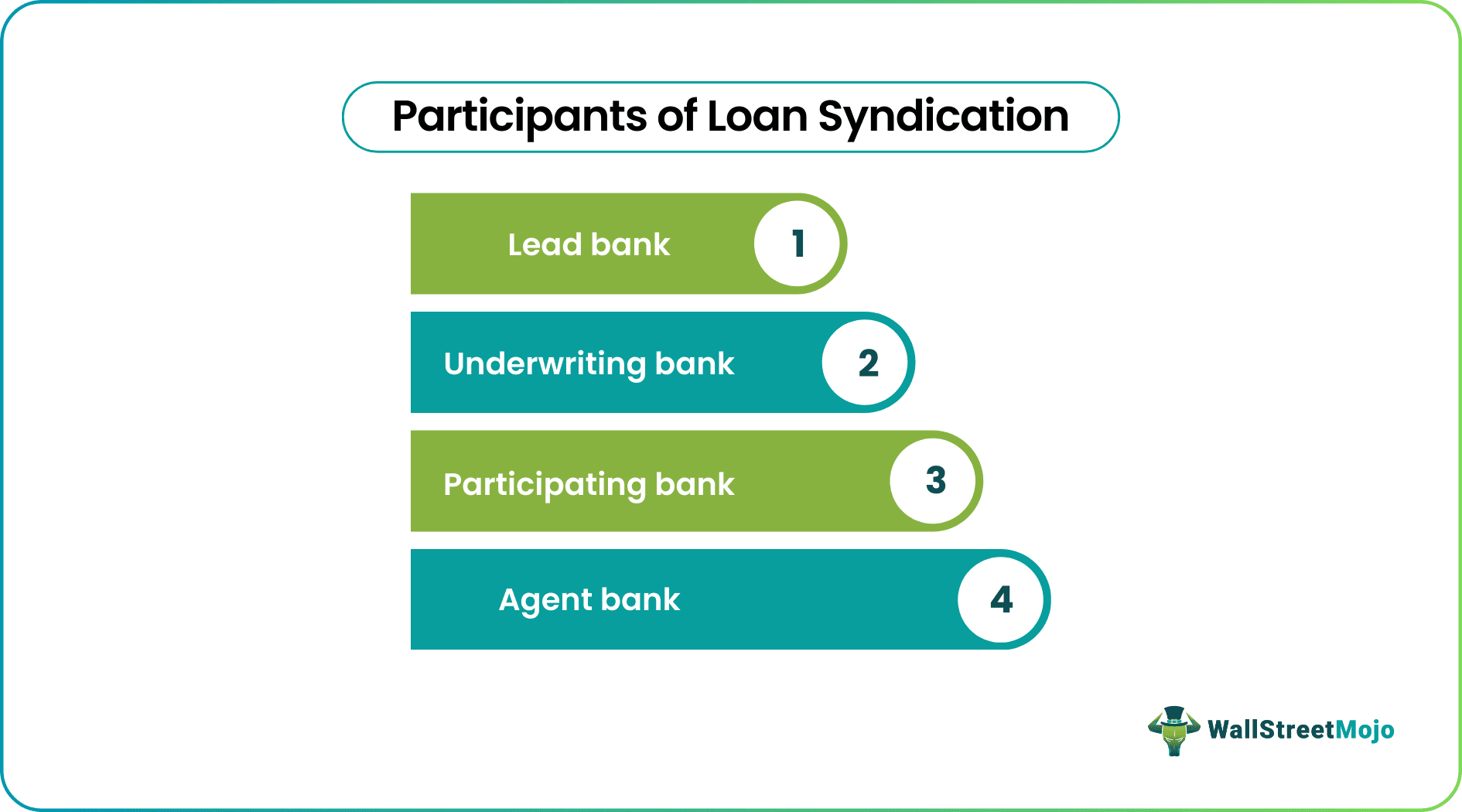

Participants

Below are the participants in process of loan syndication.

#1 – Lead Bank can also be called an Arrange Bank

- The lead bank acts as a manager and is responsible by a borrower for organizing funding based on a specific term that the loan parties decide.

- The lead bank must find other banks as lending parties willing to bear risk together to participate in this syndication.

- The lead bank must discuss details of the agreement and be responsible for preparing loan documentation with participating banks.

#2 – UnderWriting Bank

- The lead bank may underwrite the unsubscribed portions of the required loan, or a different bank may fund the loan.

- Underwriting banks will take the risk that will likely occur.

#3 – Participating Bank

- All banks that participate in loan syndication are known as participating banks.

- Participating banks will charge loan syndication fees for their participation.

#4 – Agent Bank

- The work of the agent bank is to ensure that loan syndication is operating effectively.

- The agent bank acts as a mediator between the borrower and lender and has a contractual obligation for both the parties (borrower and lender).

- In some cases, the agent bank has additional duties in the agency agreement.

- The basic work of agent banks is to channel the funds from all participating banks to the borrower and channel back interest and principal amount from the borrower to participating banks.

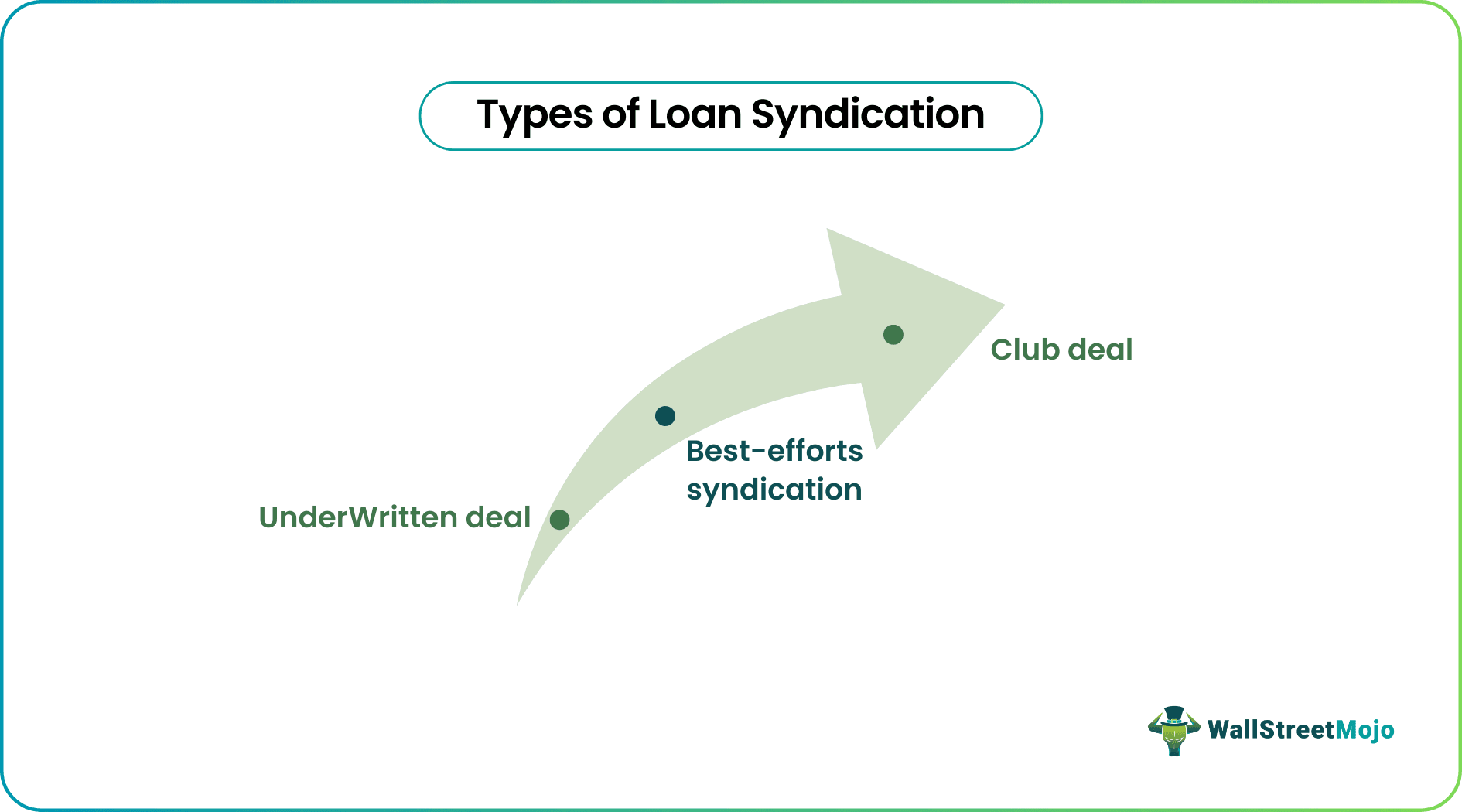

Types

The following are the types of loan syndication.

Type #1 – UnderWritten Deal

Under this arrangement, the lead agent guarantees the entire loan. The lead agent can absorb the undersubscribed portion if the loan is not fully required. This loan syndication attracts higher loan syndication fees. These loans have an increased risk, making a huge profit for the bank.

Type #2 – Best-Efforts Syndication

Under this arrangement, the lead bank is not committed to guaranteeing the loan amount required by the borrower and undertakes to find other lenders to provide commitments for the remainder. It will fill up any undersubscribed portion of the loan by taking advantage of the changes in the market condition. If the loan is continuously undersubscribed, the borrower may be forced to accept a lower amount of loan or cancel it.

Type #3 – Club Deal

This syndication is of a smaller amount, up to $150 million. In this, all the members of the club have an equal share. Again, this borrower may arrange the club, or an arranger may be involved.

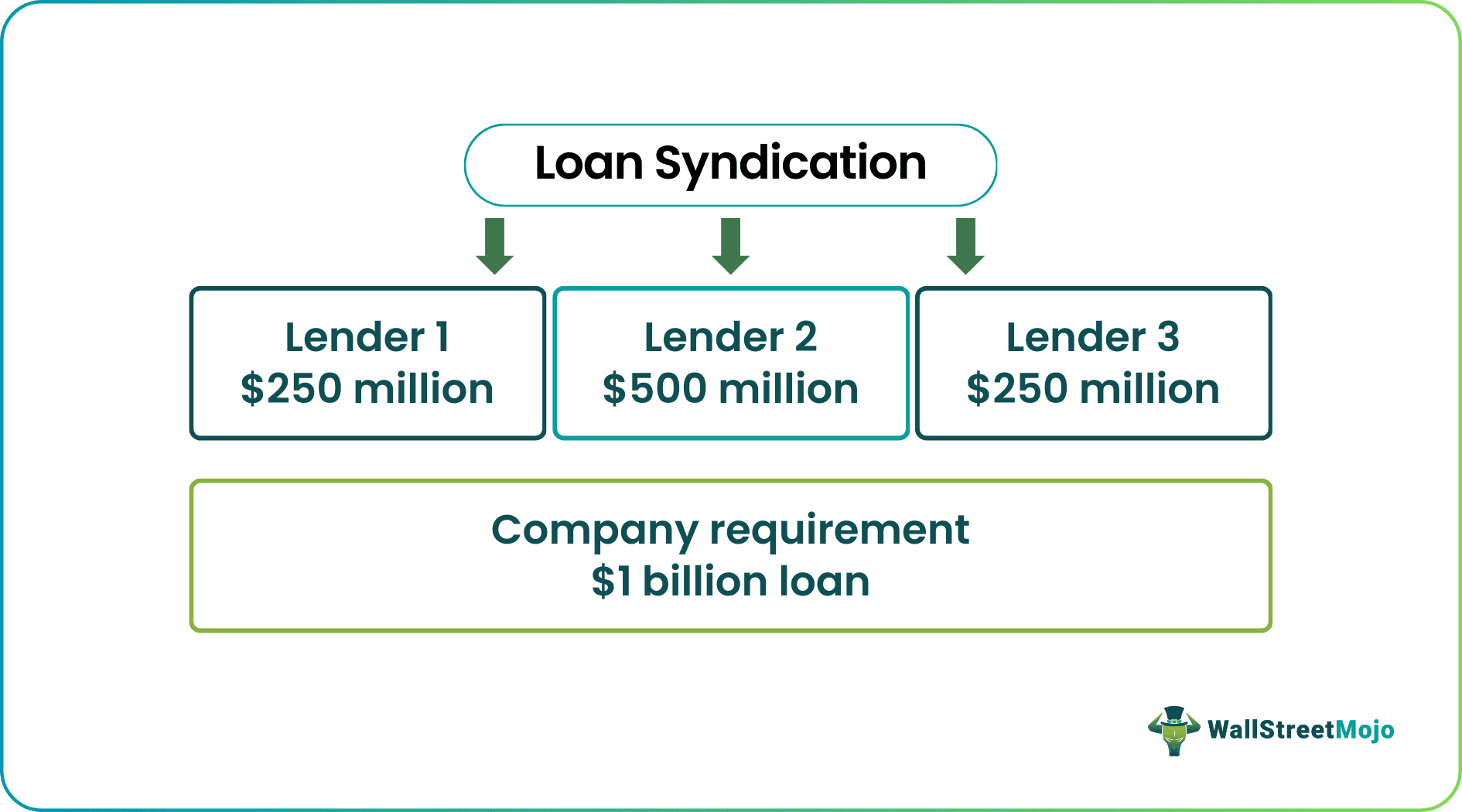

Example

Suppose EFG Ltd. is a single national organization and now wants to be a multinational organization. The company requires a large amount of capital and has a good relationship with one bank to run the business. This large amount of money is so high that a single bank cannot finance and take that high risk alone.

EFG Ltd. approaches his preferred bank (lead bank) with which the company has a good relationship and says our company requires $2 billion. Bank gives an option to the company for syndication of loans because it is not feasible to finance such a large amount individually. The preferred bank now introduces other banks to the client (company) and will decide how to segregate the amount between them (it may or may not be equal). One of the banks will be appointed as an agent bank, and all other banks will be known as participating banks.

Advantages

Let us look at the benefits of loan syndication.

- Financing takes less time and effort.

- The administration of the loan is extremely efficient.

- It is beneficial for borrowers to establish a good market image.

- Borrowers have flexibility in structure and pricing.

- The borrower need not go to each bank and not apply separate applications to all banks.

- The purpose and period of the loan are fixed.

- The system is simple.

Disadvantages

Apart from the benefits of loan syndication, there are some limitations too.

- Time-consuming process since negotiating with the bank can take various days. Thus, loan syndication is a time-consuming process.

- Borrowers may also be adversely affected by syndicated loan agreements.

- If the problem arises, it may be difficult for borrowers to satisfy all banks simultaneously.

- Managing the relationship between multiple parties is a difficult task.

- If profitability fails, the smallest bank withdraws its capital.

Loan Syndication Vs Consortium

Loan syndication is the process in which multiple financial institutions provide loan with same objective, whereas, consortium can be individuals or organizations who pool financial for some purpose. The difference between them are as follows:

| Loan Syndication | Consortium |

|---|---|

| It can be banks or financial institutions. | It can be individuals or groups. |

| A syndicate agent is appointed. | There is no role of any agent. |

| The aim is usually merger, acquisition, international transactions, buyouts, etc. | The aim is usually to meet any financial obligation like debt. |

| The fund involved is huge. | The money involved is lesser than syndication requirement. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What is loan syndication vs participation?

Loan syndication is the process by which multiple lenders fund a large loan for a single borrower. In contrast, participation refers to a lender selling a portion of an outstanding loan to buyers who may collect interest and principal payments from that loan later.

What are loan syndication fees?

Borrowers pay different fees to syndicate lenders depending on their roles, such as an upfront fee, a commitment fee, a facility fee, and a letter of credit fee. Such payments generate a specific bank income in the syndicated loan market.

What are the reasons for loan syndication?

Loan syndication is typically used when a borrower requires a loan amount too large for a single lender or when the loan falls outside the lender’s risk exposure scope levels. Multiple lenders form a syndicate to offer the borrower the requested capital in loan syndication.

What is consortium loan syndication?

Several lending institutions collaborate to finance a single borrower in consortium loan syndication. Despite structural and operational differences, these banking arrangements are similar to loan syndication.

Recommended Articles

This article is a guide to Loan Syndication and its meaning. Here, we discuss types of loan syndication, process, examples, types, and participants. We also include some of its advantages and disadvantages. You can learn more about accounting from the following articles: –