What Is A Signature Loan?

A signature loan is a type of personal loan that does not require collateral. Instead, the borrower’s signature on the loan agreement represents a legal promise to repay the funds. One can avail of this type of loan from banks, online lenders, etc., to meet any financial requirement.

Lenders charge higher interest rates on such loans than secured loans, such as a mortgage or auto loan, as no collateral is involved. Therefore, getting approval for such a loan will depend on the applicant’s income and credit history. Typically, one can avail of signature loans ranging from $500 to $50,000. That said, some lenders offer up to $100,000.

- A signature loan meaning implies a personal loan that does not involve any collateral (property, car, etc.); it is an unsecured loan secured by the borrower’s signature.

- Signature loan interest rates are higher than unsecured loans. But, again, this is because the absence of collateral increases a lender’s risk exposure.

- A good faith loan has a fixed interest rate, unlike revolving credit.

- Individuals need to have a high credit score for good faith loan approval. Besides a borrower’s age, lenders check the applicant’s age and income to determine if the latter can repay the loan.

Signature Loan Explained

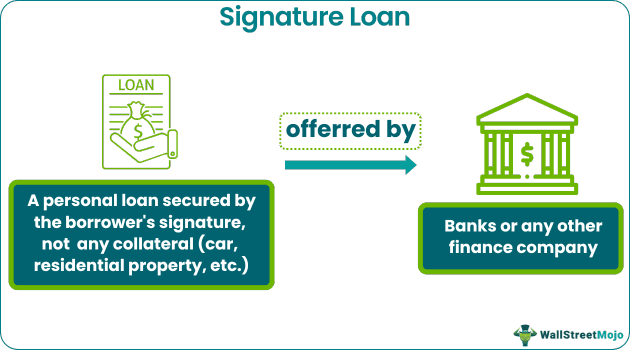

A signature loan refers to a personal loan secured by a borrower’s signature, not any collateral, such as a car, house, etc. One can avail of such loans from a bank or any other company offering financial assistance.

To get approval, individuals must fulfill signature loan requirements concerning creditworthiness, age, and income. In other words, lenders check borrowers’ credit score and their income stability to determine whether the latter can repay the funds. For instance, the minimum credit score for signature loans required by lenders is generally 610-650. With such a score, the interest rate on such a loan is usually high. On the other hand, individuals with a high credit score of 690 and above can get a loan with a low-interest rate.

Once a lender approves the loan application, they transfer the funds to the borrower’s bank account. After that, the debtor has to repay the amount plus interest over a certain duration called the repayment tenure. This period usually ranges from 1 year to 5 years. If individuals want to repay the loan quickly, they might want to find a lender that does not impose prepayment penalties.

Also known as good faith loans, these loans do not come with end-use restrictions. Hence, individuals can utilize the funds for various purposes, for example, financial emergencies, vacations, debt consolidation, etc. That said, one must note that signature loan interest rates are higher than secured loans owing to the absence of collateral. Also, the interest rates vary across different lenders. Sometimes, the loan provider may need a co-signer on such a loan. The co-signer must pay the missed payments or the entire loan amount if the borrower fails to repay the loan.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Example

Let us look at this good faith loan example to understand the concept better.

Suppose a borrower named Andy got a signature loan with 8% interest for an amount equaling the total borrowings on all his credit cards, with the interest rates ranging from 15% to 18%. He can utilize the loan to pay off the total credit card debt. This way, he would have to pay 5% interest, which is lower than the previous higher rates.

Uses Of Signature Loan

Individuals can avail of a good faith loan for the following purposes:

#1 – Financial Emergencies

Such loans can help individuals pay for the unforeseen expenses arising from emergencies, for example, car repair and medical bills. If individuals do not have an emergency fund to meet urgent financial requirements, availing of a good faith loan can be an ideal solution.

#2 – Major Events

Major events such as weddings or moving to a different state or country can be expensive. If individuals do not have the necessary funds in their bank account, they can take out a good faith loan from a financial institution. That said, they must only borrow the amount that they can repay.

#3 – Debt Consolidation

If individuals have credit card debt or other high-interest borrowings, using a good faith loan with a lower interest rate to pay off the outstanding amount can be a wise move. This way, they can save a significant amount on interest payments.

#4 – Building Credit

A good faith loan is a good way to build credit for individuals with a strong credit profile, as individuals must have a high credit score for signature loan approval.

Signature Loan vs Revolving Credit

Good faith loans and revolving credit serve the same purpose; borrowers can utilize funds received from lenders to fulfill different financial requirements. Both of them do not come with end-use restrictions. However, there are some crucial differences between the two types of credit that one needs to remember. So, let us look at them.

| Signature Loan | Revolving Credit |

|---|---|

| When an individual applies for a good faith loan, the lender transfers the entire loan amount to their bank account in one go. | One can take out funds as needed. A credit card is an example of a revolving credit line. |

| A good faith loan has a fixed interest rate. | Revolving credit comes with variable interest rates. |

| The interest rates are comparatively lower. | This form of credit comes with higher interest rates. |

| This is ideal for individuals whose financial requirements are clear. | Revolving credit is ideal for individuals who are trying to manage purchases and do not have a clear idea regarding the scope of expenses. In addition, people in business often use it to prevent future cash flow issues. |

| Interest is payable on the entire loan amount. | Individuals have to pay interest only on the amount they utilize. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. Where can I get a signature loan?

Individuals requiring financial assistance can avail of a good faith loan from the following providers:

– Banks: Traditional banks offer such a loan. Before applying for it, one must compare the interest rates offered by different banks. For example, if an individual is an existing bank customer, they might receive a loan at a lower interest rate from the financial institution.

– Credit Union: Some credit unions offer this loan, and, in some cases, the interest rate is lower than that of banks.

Besides banks and credit unions, one can get this type of loan from online lenders.

2. Are signature loans a good idea?

These loans are suitable for individuals seeking financial assistance without collateral. That said, these loans have a high-interest rate. Hence, one must assess their repayment capacity before applying.

3. How many signature loans can you have?

One can have 1-3 loans from the same lender simultaneously. The maximum limit varies from one lender to another. There is no maximum limit to the number of loans across multiple lenders.

4. How long does it take to get a signature loan?

It takes anywhere from one day to one week. The duration varies across lenders.

Recommended Articles

This has been a guide to What is Signature Loan and its meaning. Here, we explain its uses, an example, and a comparison with revolving credit. You may also find some useful articles here –