What Is A Demand Loan?

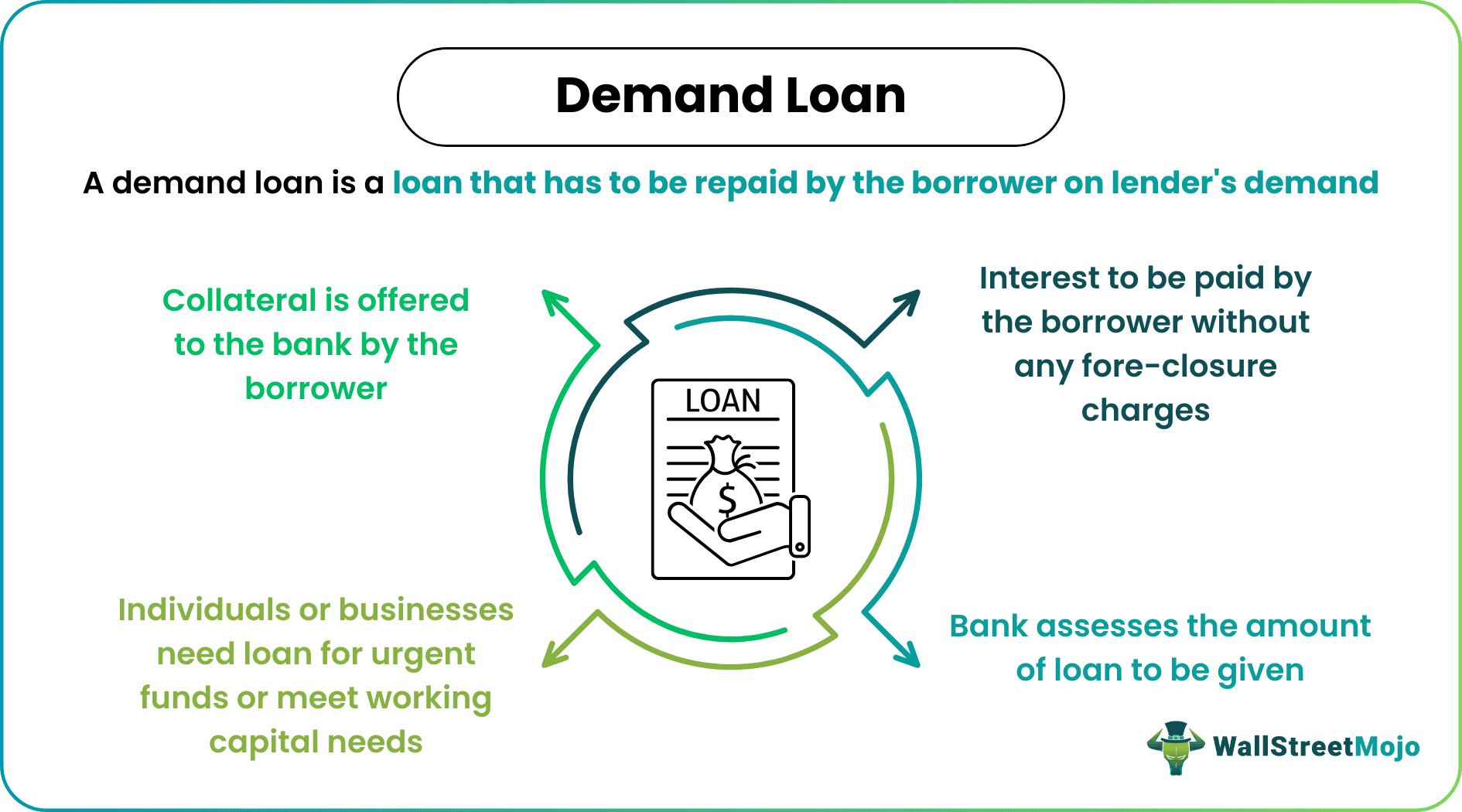

A demand loan (DL) is a secured loan that has to be repaid by the borrower upon the lender’s demand. Usually, the tenure of these loans can range from a minimum of seven days to a maximum of one year. Individuals and businesses mostly use these loans to meet their short-term financial requirements.

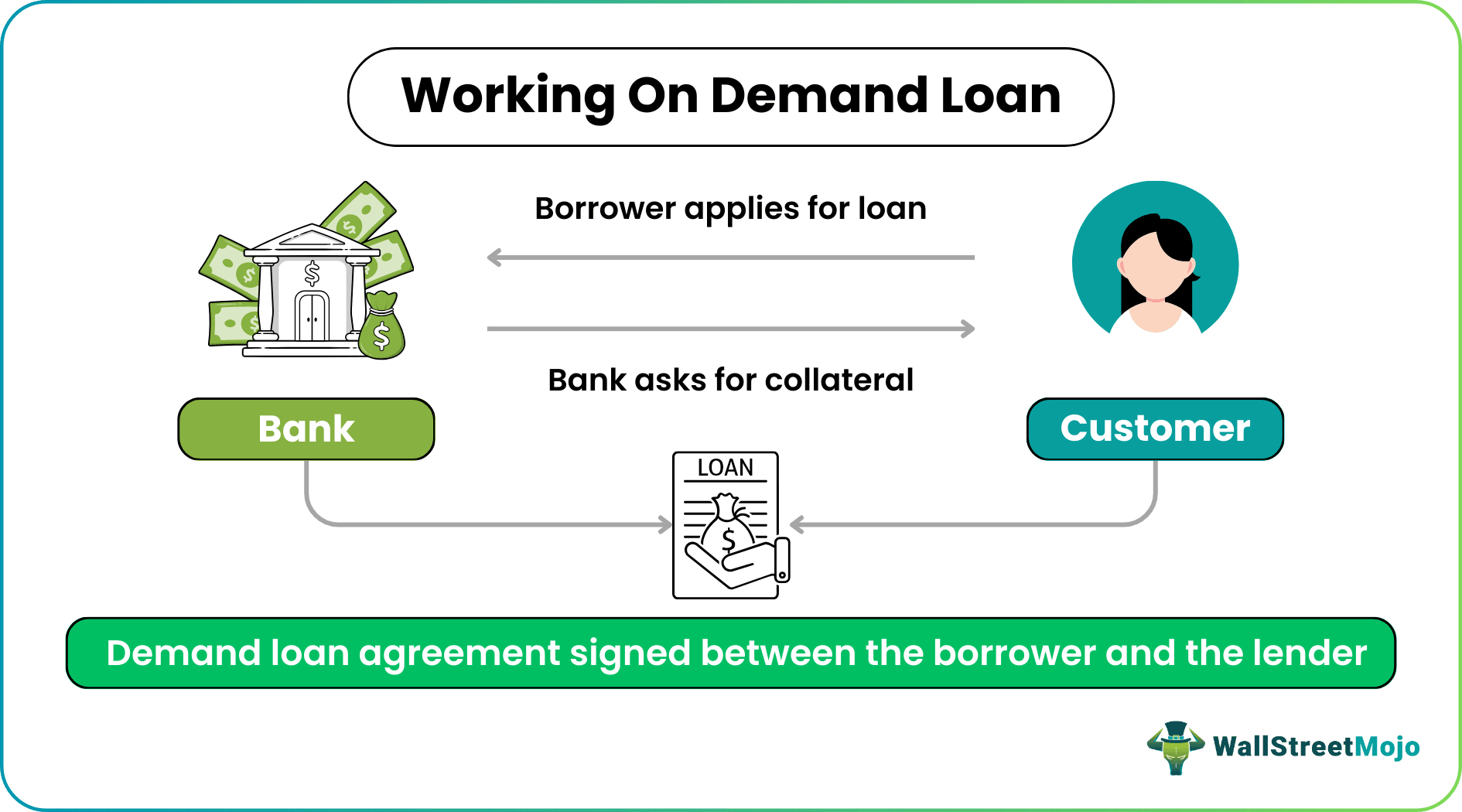

Typically, lenders grant demand loans to the borrowers against collateral at a floating interest rate. Borrowers can use land, buildings, vehicles, or fixed deposits as collateral to secure these loans. They can be closed at the discretion of the lender or the borrower or as per the terms of their agreement. Call loan is the most common form of demand loan. Furthermore, this loan is also called a working capital demand loan as it is taken to finance the short-term capital needs of businesses like payroll, rent, purchases, etc.

- A demand loan is a loan that has to be repaid by the borrower on the lender’s demand.

- Every DL is issued for a short duration ranging from seven days to a few months against collateral security.

- DLs are mostly availed for meeting short-term financial or capital requirements.

- Unlike DL, term loans are fixed long-term loans with a set repayment schedule. Lenders cannot recover them on-demand.

- A call loan offered by banks to brokerage houses is an example of DL, whereas a housing loan is a typical example of a term loan.

Demand Loan Explained

The demand loan is a loan agreement between the lender and the borrower, which enables the lender to demand the loan repayment at any time. For DL, collateral is a must. The lender and borrower enter into a demand loan agreement specifying the amount and tenure of the debt, interest payable, and call back option available to the lender.

This type of loan is not always preferred by borrowers. They avoid it because of the risk factor which involves repayment anytime whenever the lender calls for it. Thus may happen at a very short notice, which may not be convenient for the borrower. However, from the lender’s point of view, it is very convenient because they can lend the money and earn interest but at the same time access the funds as and when needed.

But it is important for both borrowers and lenders to properly and carefully consider the terms and conditions of the agreement. The need to be fully aware of various obligations, implications and risks involved like the repayment terms, fees, interest rates charged etc, in these arrangements.

Types

Here are some common types of demand loans in the market.

- Personal lines of credit – This is a revolving credit account that works similar to a demand loan. The borrower has the risght to access the amount that is pre-approved by the lender and pay the amount back at their own convenience.

- Business lines of credit – Similar to the above, the businesses are also allowed to access funds upto a certain limit and repay as and when possible.

- Credit cards – They are a form of loan on demand where the cardholder can make purchase or withdrawals upto an approved limit and repay the outstanding balance any time.

- Overdraft – This type of demand loan agreement allows the customers of banks to withdraw more money than is available in their account and repay them when the customer has sufficient funds to do so.

- Cash Credit – This is typically meant for businesses where they borrow funds upto a certain limit to meet their working capital needs and repay it as and when required and possible.

Thus, the above are some widely used form of demand loans.

Features

Let us look at some of the important features of this type of loan.

- Under this arrangement, the borrower can also settle the loan anytime. Unlike usual loans, there is no fixed maturity date or repayment schedule as per the demand loan form.

- The lenders charge a floating interest rate on loans as per the demand loan agreement. The demand loan interest rate is higher than the prime lending rates of the bank and is payable according to the terms specified in the contract.

- The loans are of shorter duration, starting from seven days to as much time agreed upon by both parties.

- It involves the most minor documentation and takes lesser sanction time. The terms of the loan, as per the demand loan form, depend on the credit rating or history of the borrower. Businesses or individuals with weaker credit scores or shoddy credit histories can also utilize such loans. Thus, banks must practice due diligence before sanctioning them.

- Usually, banks find it safer to disburse this type of loan since it has collateral security. In case of default, they can recover their loan by encashing the value of the collateral.

- Moreover, they also benefit from a steady flow of interest income from them. Therefore, DL is an attractive source of income and an important means to improve their asset quality.

- Furthermore, it is the most convenient form of loan for businesses as the loan does not have any prepayment penalty. The borrowers get the flexibility to either foreclose the loan or make part repayment anytime. If they close the loan before time, they have to pay interest only for the period borrowed. In such a scenario, the borrowers save the interest for the remaining period.

Examples

Let us understand the concept of DL using examples given below:

Example #1

A small American farmer, McMahan, setups a modern dairy plant in his village. To fund its short-term operational needs, he plans to take a loan. But, with no credit history to flaunt, if the farmer goes to the bank and asks for a working capital loan, the farmer is not likely to get it.

But if McMahan can provide collateral like a fixed deposit or insurance paper, the farmer can easily avail the DL to fund his business activity. The collateral will cover the loan amount and fully secure McMahan’s loan.

Hence, McMahan takes a repayable on demand loan against the fixed deposit he has with the bank and gets the required funds to operate the dairy project. Bank will be willing to offer debt as it can request repayment anytime and receive interest on the money lent. Also, the bank has the option to encash the deposit in case of default.

Example #2

An individual, Martin, has some urgent medical needs and requires some loan for the same, but for a shorter duration. As Martin’s loan needs are urgent, Martin may not like to undertake the lengthy process of loan disbursement from the banks.

Therefore, Martin will hand over the life insurance policy as collateral and avail the DL to cover his treatment. Moreover, Martin can close the loan as soon as he gets the money from his pension fund and pay interest only for the period he borrowed the money. Therefore, he’ll have access to instant funds and pay less interest.

Example #3

A big company, XYZ, urgently needs machinery to improve its production capacity to meet the demands of its product, facemasks. Since the company has a good relationship with its bank, it will opt for DL. In this case, XYZ will submit a DL application with the bank to get a working capital demand loan for buying machinery for its urgent needs.

Therefore, XYZ will offer some collateral like stocks, against which XYZ will be availing of the DL loan and buying the required machinery. By purchasing the machinery, the company can expand its production. As soon as XYZ gets the payments from the buyers of its facemasks, XYZ will close the bank’s DL.

If the bank fears that the company will not be in a position to fulfill its obligation, it can ask the company to repay. As evident, both the bank as well as the company XYZ benefit from demand loans. The company gets the funds, and the bank receives interest based on the demand loan interest rate..

The above examples give us a very clear idea about the different forms of repayable on demand loan and the various situations where they can be used along with the risks that come with the facility.

Demand Loan Vs Term Loan

For knowing the real difference between the DL and term loan, we will study the below table:

| Parameters | Demand Loan | Term loan |

|---|---|---|

| Meaning | Short-term loan that the borrower must repay on the lender’s demand | Long-term loan with a fixed tenure and repayment schedule |

| Purpose | Meet short-term funding needs of the borrower | Fulfill long-term funding needs |

| Duration of the loan | 7 days to a few months | 1 year to 20-30 years (depending upon the project) |

| Documentation | Less documentation required | Complex documentation process |

| Disbursement | Loan sanctioned quickly | Sanction takes time |

| Risk involved | Less risk of default as the duration is short | More risk of default due to long duration |

| Restrictions on repayments | No restrictions | Restrictions exist |

| Mode of repayment | Lender reserves the right to ask for the repayment of the DL, or the borrower repays at its discretion | Pre-defined payment mode in equated monthly installments (EMIs) |

| Rate of interest | Floating | Fixed/Floating |

| Interest charged | Chargeable only on the outstanding principal | Charged on the total principal amount |

| Collateral | Required | Not required |

| Penalty for foreclosure of loans | No penalty | Pre-determined penalty |

The above table shows that DL is the best form of working capital debt for businesses. A favorable DL agreement benefits both the lender as well as the borrower. Also, term loans are more suitable for an individual salaried class person who can easily repay the loan using the EMI option spread over a long period like housing loans.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

How do the demand loans work?

<p>DLs are short-term loans that the lender can call for repayment anytime. They work on the principle of keeping any tangible asset or financial instrument as security against which the lender grants a loan to the borrower. The loan is always given to the extent which can be covered by the value of the collateral in case the loan gets defaulted.</p>

What are the benefits of a demand loan?

<p>DLs are easily available to the borrower. It can be availed even by clients with bad credit records. It needs less time for disbursal and can be paid in full prior to the loan tenure. Since it is a secured loan, the lender doesn’t face the risk of default. The lender can also benefit from the interest income.</p>

What are demand loans usually most appropriate for?

<p>They are generally taken by individuals for immediate personal needs like marriage, education, or medical treatment and by businesses to meet their short-term or working capital needs. Businesses can use them to pay salaries, rent, purchase inventory, machinery and equipment, and invest in new projects.</p>

Recommended Articles

This has been a guide to what is Demand Loan. We explain it with example, types, features and its differences with term loan. You may also have a look at the following articles to learn more –