What Is A Due-On-Sale Clause?

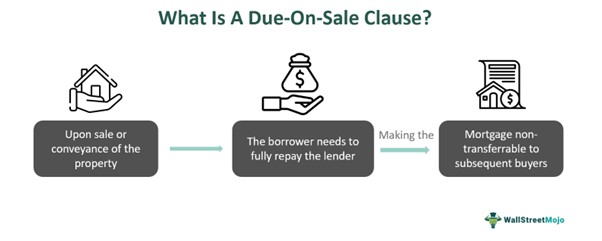

The Due-On-Sale Clause is a provision typically included by the lender in a mortgage agreement. It mandates that the borrower must settle the outstanding balance of the loan before selling or transferring the property to another party. With the exception of certain loans such as USAD, VA, or FHA loans, this clause is standard across most loans.

Lenders typically invoke this clause when they perceive the prospective buyer as posing a financial risk or when they anticipate greater financial returns by initiating a new loan with the buyer. Essentially, it prohibits the borrower from transferring ownership of the mortgaged property without first satisfying the outstanding loan amount. This provision empowers the lender to demand repayment of the entire loan balance.

- The due-on-sale clause, standard in most mortgage loans, allows lenders to enforce foreclosure if a borrower sells the property without paying off the loan, except in certain government-funded loans, according to the 1982 law.

- The Garn-St. Germain Depository Institutions Act of 1982 enabled lenders to enforce the due-on-sale clause, securing their right over mortgaged properties without foreclosing the loan.

- In certain situations where there occurs a transfer of ownership without any sale, purchase, or rent to another party, the clause does not get invoked like in – Inheritance, Joint tenancy, Divorce legal separation, or Living trusts.

Due-On-Sale Clause Explained

The due-on-sale clause is inserted into the mortgage agreement, which gives the lender specific rights to foreclose the loan when the borrower tries to sell without full loan payment. Such right gets embedded into the mortgage agreement duly on the paperwork. This provision is typically included in the mortgage paperwork, following the Garn-St. Germain Depository Institutions Act of 1982, most mortgage loans in the US established after 1988 include an acceleration clause. Borrowers should exercise caution regarding this clause, as lenders may legally require immediate loan repayment.

Usually, whenever a mortgaged property gets sold by the owner, the buyer will pay the amount to the seller to pay the remaining amount and create a new mortgage over the existing property. However, many cases have come to the point where the property owner tries to sell the property to a new owner by transfer of ownership without closing the original mortgage loan. As it resulted in losses to the lender on account of the lost chance to charge a higher mortgage rate to the new buyer, the clause protected them from allowing the owner to illegally transfer the ownership without foreclosing the mortgage and then selling it.

In essence, this clause protects lenders’ business interests and ensures that their assets are only sold with proper adherence to loan repayment terms.

Examples

Let us understand the concept with the help of some examples.

Example #1

Let us assume that a property had been mortgaged by a couple, David & Hana, to their lender at $400,000. After three years of continuous loan repayment, they paid only $350000 of the loan. Now, they get an offer of $425,000 for selling their home to another party, which they gladly accept.

The sale can happen in two ways:

- The couple could get the rest of the dues fully paid and keep the $75,000 with themselves. Or,

- The couple could bypass the system, not inform the bank, and sell the mortgaged property without notifying the bank. As a result, the lender gets notified of the ownership transfer and immediately invokes the clause to foreclose the loan legally.

Example #2

Suppose Emma purchases a condominium using a mortgage loan from a lender. The property is valued at $200,000, and Emma secures a mortgage for $150,000. She makes regular mortgage payments and pays off a significant portion of the loan over several years.

After living in the condo for a few years, Emma’s career takes her to another city, and she decides to sell the property. She finds a buyer willing to purchase the condo for $220,000.

In this scenario:

- Emma enters into a sales agreement with the buyer, but before the sale is finalized, she informs her lender of her intention to sell the property.

- The lender reviews the terms of the sale and confirms that Emma has paid off a substantial portion of the mortgage loan. However, there is still an outstanding balance of $50,000.

- Since Emma has yet to fully repay the mortgage loan, the due-on-sale clause is triggered. The lender informs Emma that she must repay the remaining balance of the loan before the sale can proceed.

- Emma agrees to use the proceeds from the sale to pay off the remaining mortgage balance. Once the loan is fully repaid, the sale is completed, and the buyer takes ownership of the property.

Exceptions

Although the clause has been legally enforceable since 1982, due-on-sale clause exceptions cannot be enforced legally in certain specific situations:

#1 – Inheritance

If the property owner dies and the title gets transferred to the legal heir to occupy the property, then the clause ceases to be enforced. However, if the heir intends to sell it, then the clause comes into effect and is invoked by the lender.

#2 – Joint Tenancy

If the property in the mortgage had been bought jointly with someone, then after the death of a party, the clause cannot be invoked, and the loan would go as before.

#3 – Divorce or Legal Separation

When a property owner goes through a divorce or legal separation, the clause also becomes ineffective if the property gets transferred to the spouse or children from the marriage.

#4 – Living Trusts

If the borrower transfers the property to the trust where the trust has the borrower as its beneficiary, then the clause cannot be invoked.

However, one must strictly note that in all the above cases, if the spouse or children or beneficiary or inheritor decides to live in the property, then only the cause does not get invoked. Moreover, if these successors sell or rent the property to someone else, then the due-on-sale clause of real estate still gets invoked. So, one must be wary of these things.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

How to avoid the due-on-sale clause?

<p>To avoid triggering the due-on-sale clause, individuals can explore legal avenues such as transferring property title through divorce settlements or into irrevocable trusts. Compliance with the terms of the mortgage agreement is essential to prevent enforcement of the clause. Consulting legal experts for guidance tailored to specific situations can provide practical strategies for navigating these complexities.</p>

What types of mortgages do not have a due-on-sale clause?

<p>USDA, VA, and FHA loans typically have restrictions on due-on-sale clauses, limiting their enforceability. These government-backed loans provide specific guidelines regarding the transfer of property ownership, often allowing for transfers without triggering the due-on-sale clause.</p>

Is there a due-on-sale clause when the property is gifted?

<p>If the property has been gifted to the natural heir of the property, then the clause can not be invoked. However, if the property gets gifted to a person other than an heir, then the clause could be invoked as per its terms and conditions.</p>

Recommended Articles

This article has been a guide to what is a Due-On-Sale Clause. Here, we explain the concept in detail along with its examples and exceptions. You may also find some useful articles here –