What Is Peer to Peer Lending?

Peer to Peer (P2P) Lending refers to a lending option where borrowers can obtain loans directly from individuals and businesses without the involvement of any financial institution in the process. Multiple platforms help loan seekers connect with a matching lender and borrow the desired amount.

Also known as social lending, P2P option lets people establish their businesses besides helping them serve personal purposes. As soon as the finance seekers fill out the online application form, the lenders assess it. Once the latter finds the application good to go, they approve the deal. However, if they find the deal risky, they reject the application.

- Peer to peer lending refers to a lending option wherein no financial institutions are involved, and the borrowers and lenders can connect directly using an online platform.

- Lenders need to open an account on a website to start investing in P2P lending.

- P2P lending is different from crowdfunding as the latter gives investors an ownership of a share in the venture.

- Such loans are at a higher credit risk as the borrowers might misrepresent their credit ratings to obtain finances and default.

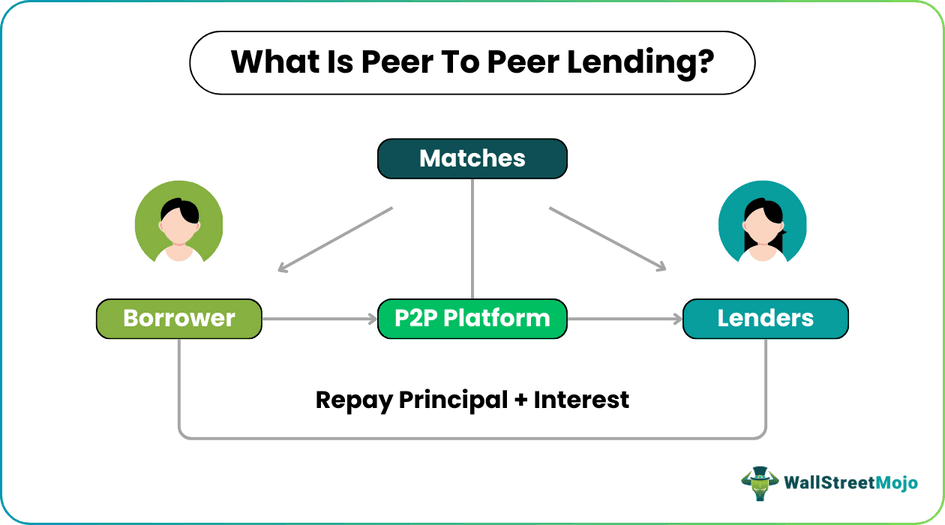

How Does Peer to Peer Lending Work?

Peer to peer lending is an alternative that financing individuals or businesses opt for to remove the involvement of any formal financial institution in the process. Multiple P2P websites offer borrowers a convenient platform to have matching lenders available to provide the required finances. These platforms offer loans at specific interest rates. This rate depends on the creditworthiness of the people.

Every P2P service provider sets a set of criteria regarding the loan tenure, repayment terms, penalties, etc., that both borrowers and lenders must consider. This social funding can either be secured or unsecured, given the borrowers’ loan requirements and credit records. Moreover, this financing option is not only available to borrowers, but peer to peer lending for investors is also widely used. Investors can consider these loans to diversify their portfolios and generate more and more profits.

When a bank is involved in lending, it uses its assets deposited by other customers to fund the loan. While borrowers are directly matched with investors on the peer to peer lending apps, investors get a choice to evaluate profiles and choose the loans they wish to provide.

This service is offered digitally, reducing the investment in overhead costs like building, office, etc., and operating at a lower overhead rate by providing services cheaper than traditional financial institutions such as banks. In such transactions, lenders earn higher returns than savings and investment products offered by banks.

P2P lending is different from crowdfunding as the latter provides investors with an equity stake in the project/ business under which the lender’s fund is invested.

How To Invest in P2P Lending?

In the United States, the peer to peer lending seems gaining dominance over traditional funding by offering consumer loans of over $48 billion from 2006 through 2018. The same is likely increase to around $150 billion annually by 2025.

Peer to peer lending and investing involves a series of steps. Firstly, lenders must register on the online P2P platform and make an account on the portal. As soon as the account opens, they must deposit a sufficient amount in the account based on what they desire to lend. Then, depending on the limit, the online service provider matches and shortlists a set of borrowers.

The next step is for the lenders to assess borrowers’ profiles to ensure they lend to someone trustworthy. When the former finds less risky borrowers, they choose the ones who are most unlikely to default. Given that creditworthiness plays an important role, there is hardly any chance of having options of peer to peer lending for bad credit. Finally, if the borrowers and lenders agree to the terms, tenure, and rates related to the deal, the latter lends the required amount.

Examples

Let us consider the following peer to peer lending examples to understand the concept better:

Example #1

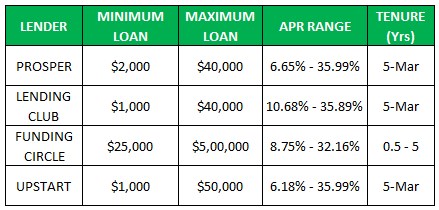

Here is a list of P2P portals with the lending details, which borrowers can easily access and retrieve.

Example #2

The peer to peer lending portals are classified based on the nature and purpose of borrowing. For example, while LendingPoint, a Georgian lending platform, makes available financing options for people with fair credit, Universal Credits is for those who need to improve their credit rating. Thus, borrowers can search for their type of portal, and lenders should choose and make an account on a portal based on what they find suitable per their funding wishes.

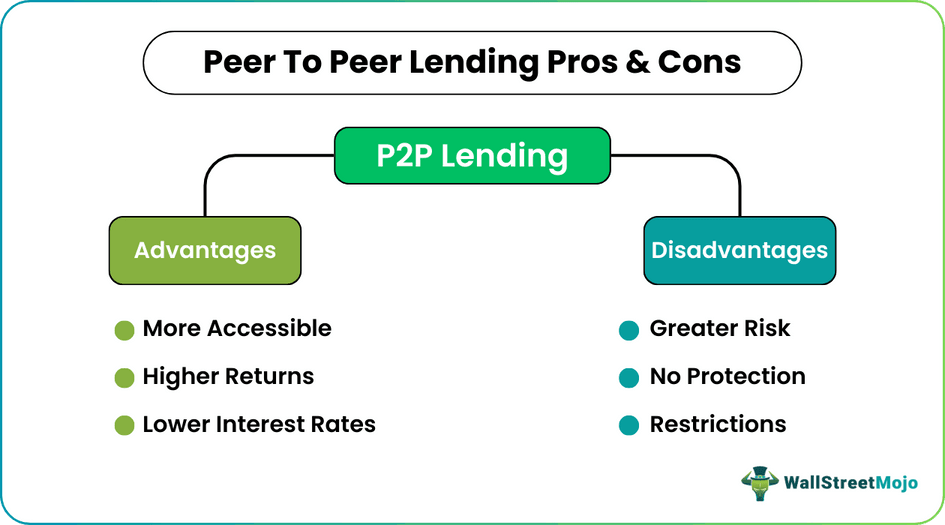

Advantages And Disadvantages

When there is a portal with numerous lenders, the borrowers can access multiple financiers. Hence, they know that they will get a match for their requirements sooner or later. Simultaneously, lenders get an opportunity to contact the loan seekers directly and assess them individually based on their creditworthiness, and then choose the one they think won’t default. The best part is that there is no involvement of any intermediary in the process.

Investors get higher returns as they decide the interest rates themselves, making it a profitable deal. Plus, the loans in P2P lending come with a lower interest rate than conventional institutions due to the competition between the lenders. This allows borrowers to choose from an ocean of lenders with lower interest rates.

Peer to peer lending has a lot of benefits in store for borrowers and lenders alongwith multiple disadvantages simultaneously. First, lending involves greater credit risk as borrowers with low credit ratings opt for such funding.

This lending mechanism has no government protection. Here, borrowers and lenders choose their partners in the transaction irrespective of the government’s insurance against the loss. In addition, some countries’ jurisdictions do not allow P2P lending due to certain constraints regarding investment regulations.

Frequently Asked Questions (FAQs)

What is a peer to peer lending in the UK?

Peer to peer lending refers to a modern, fully digital lending business where the money is borrowed and lent between individuals or groups without the involvement of any third-party institutions such as a bank or financial authority. The industry has grown widely in the UK, with the funding limit reaching over £6.1 billion in 2018.

Is peer to peer lending safe?

Yes, P2P lending is a safe option despite involving high-interest fees and greater interest rates for few borrowers. The risk is, of course, more as everything is maintained and managed online. However, the lenders are at a greater risk as it’s their fund involved in the deal. This is why these platforms allow lenders to assess profiles, verify them, and then lend to the borrowers they find less risky.

Is peer to peer lending a good investment?

Yes, P2P lending is a good investment as investors get significant returns on their funds. In addition, they do not require restricting lending to one borrower. They can diversify their investments and offer funds to multiple borrowers at a time. Hence, multiple returns are guaranteed at the end of each loan tenure.

Recommended Articles

This is a guide to what is Peer to Peer (P2P) Lending & its meaning. Here we explain how to invest in it with its examples, advantages & disadvantages. You may learn more about financing from the following articles –