Table Of Contents

Problem Loan Definition

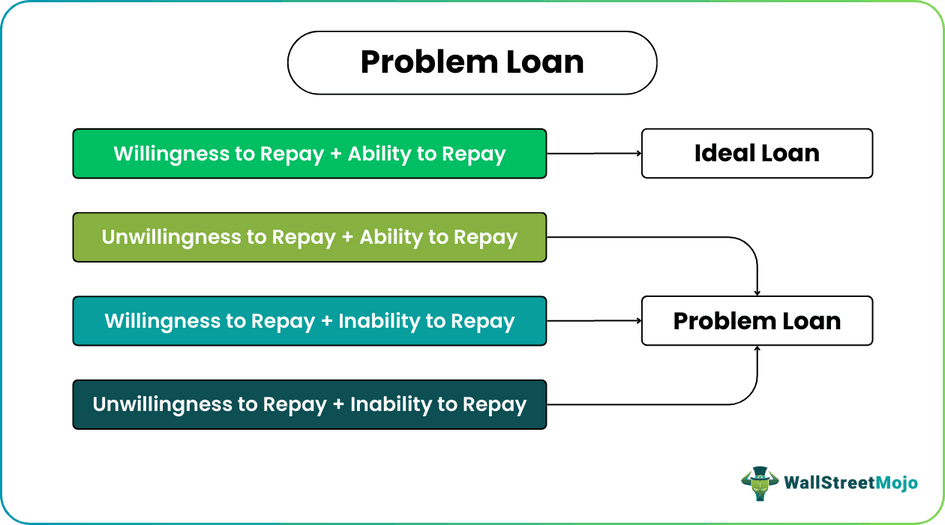

A problem loan is a scenario where borrowers fail to repay monthly loan installments. The bank labels these loans as nonperforming assets (NPA). It can occur with either a commercial loan or a consumer loan.

The loan is considered a default when borrowers miss consecutive repayments beyond the delinquency periods. A delayed repayment or loan default considerably reduces borrowers’ credit scores. It becomes a permeant mark on a borrower’s credit history. Poor credit history makes it hard for the borrower to secure future loans.

- Problem loans are debts where borrowers miss their repayment dates. It can occur with both commercial loans and consumer loans.

- Delayed repayments and loan defaults are common obstacles associated with lending. To mitigate risks, banks secure credit with collateral.

- When borrowers default on loan payments for consecutive months, their loan account is declared a nonperforming asset (NPA). When this happens, the borrower's credit scores worsen.

- Commercial loans come with a 90-day delinquency period; consumer loans give borrowers 180 days to clear pending installments. Beyond the deadline, the debt is classified as a problem loan.

Problem Loan Explained

The problem loans definition suggests serious hurdles for the banking system. They also have a massive impact on cash flow. Every bank has dealt with problem loans in its lending history.

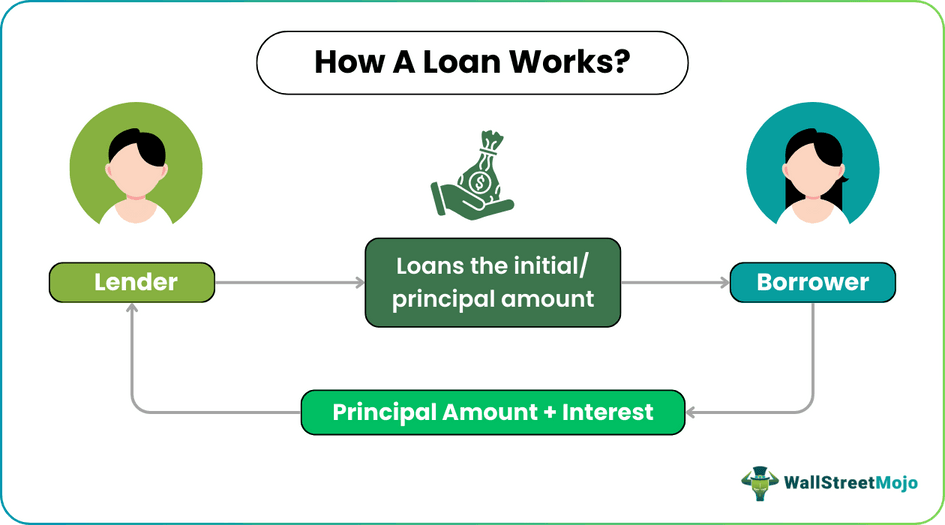

A bank offers many types of loans; commercial loans and consumer loans are the most common. Commercial loans are offered to businesses and companies, and consumer loans are offered to individuals to buy household facilities, appliances, and products.

There is a specific delinquency period for loans; beyond this period, the debt is referred to as a problem loan. But the delinquency period varies; commercial loans have a 90-day deadline, whereas consumer loans give lenders 180 days to clear pending premiums.

Every bank has a problem loan ratio. Banks try to keep the ratio low. Nonetheless, it is an ever-present issue with every bank; a small percentage of loans exhibit various issues. When a borrower fails to repay, it could be due to any legitimate reasons—financial difficulties, business losses, natural disasters, pandemics, or sudden personal expenses. However, a poor repayment history drastically affects a borrower’s creditworthiness—low credit scores.

There is a prevalent misconception that borrowers missing installment dates are immediately considered defaults. In reality, when a borrower misses consecutive monthly payments, the bank contacts them and asks them to pay the installments in parts. The bank restructures the loan—this assistance can last till the borrower becomes financially stable.

However, delayed monthly payments do affect borrowers’ credit scores. When a borrower applies for a new loan, past payment delays cause difficulties—lenders hesitate before sanctioning. In addition, it takes considerable time to improve credit scores—by repaying regularly.

Problem loan reports show that complete loan defaults are rare. In such scenarios, though, the bank suffers hefty losses depending on the type of loan. For example, the bank can seize property or sell an underlying asset if the loan is sanctioned using collateral. But unsecured loans (without collateral) are a big risk for the lender. As a result, the interest rates on unsecured loans are relatively high.

This discussion is incomplete without mentioning students’ problem loans; In America, 44 million students owe $1.6 trillion. Yet, not all would be able to repay in time owing to the post-Covid-19 recession and rising college fees.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us look at some problem loan examples to understand the concept thoroughly.

Example #1

Madelyn runs a small company that manufactures plastic bottles. When she wanted to expand her business, she took a commercial loan from a traditional bank, agreeing to pay a certain interest. The loan amount was $90,000, to be repaid within four years—48 monthly payments.

She paid all her monthly payments within the stipulated time for the first two years. Unfortunately, Madelyn suffered heavy business losses—she could no longer cover her monthly payments. As a result, she missed payments for three consecutive months (90 days). As a result, the bank labeled Madelyn's loan account a nonperforming asset.

Example #2

Now let us look at another problem loan example.

Madelyn's husband, Dahmer, worked for an MNC. He bought a new laptop by securing a consumer loan. Unfortunately, Dahmer also encountered financial difficulties; he missed six monthly installments consecutively (180 days). The loan delinquency limit for a consumer loan is six months, so the bank added Dahmer's loan to the list of problem loans.

In all such scenarios, the bank contacts the borrowers immediately and asks them to repay the loan. If they cannot, the bank offers restructuring options and asks the borrower to pay in part. If the loan defaults, the bank takes legal action and incurs losses.

How To Identify And Manage Problem Loans?

The simple ways to identify the problems are as follows.

- Every bank has a loan review department. The loan review department is supposed to check loan history and detect borrowers likely to become nonperforming loan accounts.

- Banks also identify repayment issues during the annual review.

- Reviewing borrowers’ credit history is one of the best problem loan indicators. By doing so, banks can prevent bad debts and debt traps from occurring in the first place.

- To solve problem loans, banks ultimately restructure the loan—decreasing monthly payments and increasing loan terms—to make it easier for the borrowers.

- From a borrower's perspective, they can always take money from another source to clear the problem loan. However, this option is not recommended. Borrowers opt for this alternative only when desperate.

- Foreclosure and liquidation of assets are used to resolve loan defaults. But unsecured loans pose a massive risk for the lender.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The main causes are as follows.

- Inefficient bank policies.

- Unsecured loans.

- Errors in collateral reviews.

- Improper background checks on loan applicant profiles and credit history.

- Financial difficulties endured by borrowers.

- Multiple bad debts sanctioned for the same borrower.

- Borrowers falling into debt traps.

- Irresponsible behavior towards loan payments.

To solve problem loans, banks first identify bad debts. Then, they declare the loan account a nonperforming asset or NPA. Consequently, they reach out to the borrower, asking them to pay the loan amount in parts. If a loan defaults, the bank takes legal action against the borrower to mitigate losses. Banks try to keep the problem loan ratio as small as possible.

After identifying the problem loan, the bank declares the loan account as an NPA. This severely affects the borrower's credit score. If a borrower completely defaults on a secured loan, the lender tries to recover the loss by seizing property or collateral.

Recommended Articles

This has been a guide to What is Problem Loan and its definition. Here, we explain it with examples and how to identify and manage it. You can learn more about it from the following articles -