Table Of Contents

What Is A Credit Builder Loan?

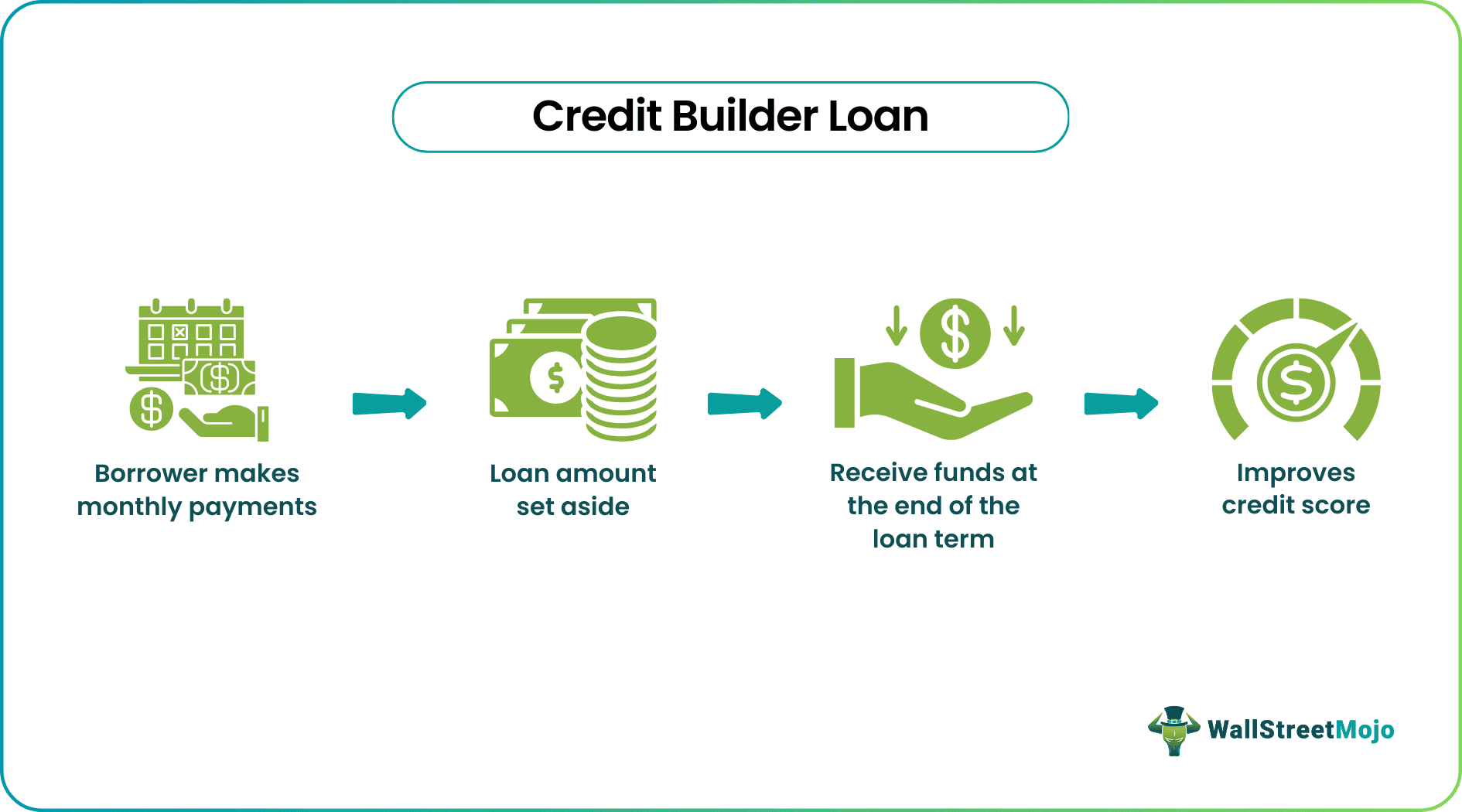

A credit builder loan is a financial product designed to help individuals establish or improve their credit history. Unlike traditional loans, where the funds are disbursed upfront, a credit builder loan works in reverse. The borrower makes regular payments into a savings account, and once the loan term is completed, they receive the accumulated funds.

The primary aim of a credit builder loan is to provide individuals with limited or poor credit histories an opportunity to build a favorable credit profile. Since these loans are typically offered to individuals with low or no credit scores, they serve as a means for borrowers to demonstrate their creditworthiness by making timely payments. The lender reports the borrower's payment history to credit bureaus, positively impacting their credit score over time.

Table of contents

- What Is A Credit Builder Loan?

- Credit builder loans help individuals establish or improve their credit history by providing a structured way for those with limited or poor credit to demonstrate creditworthiness.

- Unlike traditional loans, credit builder loans involve making regular payments into a savings account. The borrower receives the accumulated funds once the loan term is completed, encouraging disciplined repayment.

- Borrowers need to receive the loan amount upfront. Instead, funds are released after completing the loan term. This feature promotes responsible financial habits and discourages impulsive spending.

- Such loans are designed for individuals with limited or poor credit histories. Lenders often consider factors beyond credit scores, making these loans more accessible than some traditional financing options.

How Does A Credit Builder Loan Work?

A credit builder loan operates as a unique financial tool aimed at helping individuals establish or improve their credit history. When a borrower applies for such a loan, the lender typically approves a small loan amount, often ranging from a few hundred to a few thousand dollars. Instead of receiving the loan funds upfront, the approved amount is held in a secure account.

The borrower then makes regular monthly payments towards the loan over a predetermined period, typically ranging from six months to a couple of years. These payments are reported to major credit bureaus, influencing the borrower's credit history and credit score. Notably, the funds are not accessible until the loan term is completed.

Once the borrower completes the loan term and has made all the payments, they receive the accumulated funds plus any interest earned during the period. This process allows individuals with limited or poor credit histories to demonstrate their ability to manage credit responsibly, leading to an improvement in their credit score. It serves as a structured and gradual approach for individuals to enter or re-enter the credit market while building a positive credit history over time.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Choose?

When choosing a credit builder loan, several factors should be considered to ensure it aligns with one's financial goals and circumstances. Start by comparing interest rates and fees among different lenders. Look for a loan with affordable terms and minimal fees to maximize the benefits of the credit-building process.

Next, assess the loan's reporting practices to ensure the lender reports the borrower's payments to major credit bureaus. Not all lenders report to all bureaus, so choose one that provides comprehensive reporting to have a broader impact on the credit history.

Consider the loan amount and term that fits one's budget. While a higher loan amount may seem attractive, it's crucial to select an amount one can comfortably repay. Similarly, choose a loan term that aligns with one's financial goals and timeline.

Additionally, check for any additional features or educational resources offered by the lender. Some institutions provide credit education tools or other resources to help borrowers better understand and manage their credit.

Lastly, read and understand the terms and conditions of such a loan, including any potential penalties for missed payments. Transparent and fair terms contribute to a positive credit-building experience. By carefully evaluating these factors, a person can select a credit builder loan that suits their financial needs and facilitates the improvement of their credit history.

How To Get?

To get a credit builder loan, follow these steps:

- Research Lenders: Start by researching financial institutions, credit unions, or online lenders that offer credit builder loans. Consider factors such as interest rates, fees, and reporting practices.

- Check Eligibility: Review the eligibility criteria of potential lenders. These loans are often designed for individuals with limited or poor credit, but requirements may vary.

- Gather Necessary Documentation: Prepare documentation typically required for a loan application, such as proof of identity, address, and income. Lenders may request recent pay stubs, bank statements, or other relevant documents.

- Apply: Submit a loan application to the chosen lender. The application process may vary but often involves providing personal and financial information. Some lenders may perform a "soft" credit check, which doesn't impact a person's credit score.

- Approval and Terms: Once approved, carefully review the loan terms, including the loan amount, interest rate, and repayment schedule. One should ensure that they understand all the terms before accepting the loan.

- Make Timely Payments: After accepting the loan, make regular, on-time payments. The lender will report the payment history to credit bureaus, positively impacting the credit score over time.

- Complete the Loan Term: Once the borrower has made all the payments, the lender will release the funds, which the borrower can then use as needed. Keep in mind that the primary goal is to build or improve the credit history.

Examples

Let us understand it better with the help of examples:

Example #1

Imagine Henry, a recent college graduate with a limited credit history. Eager to establish credit and qualify for future financial opportunities, he applies for a credit builder loan from a local credit union. The credit union approved him for a $1,000 loan with a 12-month term and a reasonable interest rate. Henry makes regular monthly payments, and the credit union reports his positive payment history to credit bureaus. After completing the loan term, he receives the $1,000 plus a modest amount of interest. Henry’s credit score has improved, making it easier for him to qualify for a credit card or other financial products.

Example #2

The Digital Federal Credit Union (DCU) credit builder loan is reviewed in a recent article on Business Insider in 2023. DCU's Credit Builder Loan is lauded for its focus on helping individuals establish or rebuild their credit. The review highlights the structured repayment plan, where borrowers make monthly payments into a savings account, and once the term is completed, they receive the accumulated funds. This approach encourages responsible financial habits.

The article notes that DCU's interest rates are lower compared to other subprime loans, making it an attractive option for those looking to improve their credit. Additionally, the review mentions the accessibility of credit builder loans to individuals with limited or poor credit histories, contributing to financial inclusion. The article provides insights into the features that make DCU's credit builder loan a beneficial tool for credit building.

Pros And Cons

Following is a tabular representation of the pros and cons of a credit builder loan:

| Pros of Credit Builder Loan | Cons of Credit Builder Loan |

|---|---|

| Establishes or improves credit history | Limited immediate access to funds |

| Accessible to those with poor or limited credit | Interest payments (though typically lower than other loans) |

| Structured repayment plan | Potential fees associated with the loan |

| May have lower interest rates | It may not impact credit scores immediately |

| May offer financial education resources | Limited loan amounts for building savings |

| Potential to qualify for better financial products in the future | Requires a commitment to timely payments |

Credit Builder Loan vs Personal Loan vs Secured Credit Card

Below is a comparison of Credit Builder Loans, Personal Loans, and Secured Credit Cards:

| The security deposit may determine a credit limit | Credit Builder Loan | Personal Loan | Secured Credit Card |

|---|---|---|---|

| Purpose | Build or improve credit history | Various purposes (no specific credit-building focus) | Establish or rebuild credit |

| Collateral | Typically, lower loan amounts are designed for credit-building | The security deposit may determine a credit limit | Requires a security deposit (collateral) |

| Access to Funds | Limited access until the loan term is completed | Full access to funds upfront | Credit limit determined by the security deposit |

| Repayment Structure | Monthly payments into a savings account | Fixed monthly payments over the loan term | Revolving credit with minimum monthly payments |

| Impact on Credit Score | Positive impact through on-time payments | Positive impact with responsible repayment | Positive impact with responsible use |

| Interest Rates | Generally lower interest rates compared to other loans | Interest rates vary based on creditworthiness | Interest rates may be higher, but can be mitigated with a security deposit |

| Loan Amounts | Typically, lower loan amounts are designed for credit building | May offer higher loan amounts based on creditworthiness | Typically, lower loan amounts are designed for credit-building |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

While making timely payments on a credit builder loan can positively impact your credit score, improvement is not guaranteed. Other factors, such as overall credit history and debt management, also contribute to credit score changes.

Some lenders may charge fees for credit builder loans. Standard fees include application fees or administrative fees. It's essential to review the terms and conditions of the loan agreement carefully.

The timeline for credit score improvement varies, but positive effects can typically be observed over several months as the borrower demonstrates a consistent pattern of timely payments.

Some lenders allow early repayment, but it's crucial to check the terms of the loan agreement. Paying off the loan early may impact the credit-building aspect, as the positive payment history may not be reported for the entire agreed-upon term.

Recommended Articles

This article has been a guide to what is Credit Builder Loan. We explain how to get & choose it, comparison with secured credit card & personal loan, and examples. You may also find some useful articles here -