Table of Contents

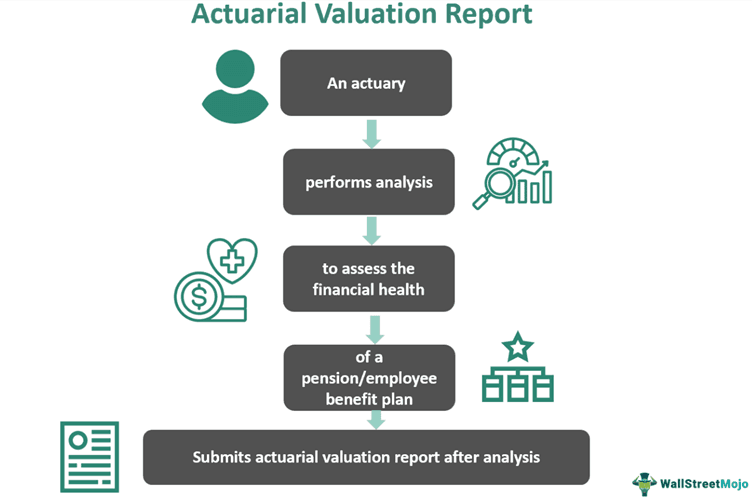

What Is Actuarial Valuation Report?

An Actuarial Valuation Report is a technical document providing an extensive evaluation of the funding and financial status of public retirement systems, such as pension plans. It considers Actuarially Determined Contribution (ADC) Rates, which show the funds needed to fund the benefits in light of assets, the funded plan ratio, and liabilities over time, among others.

To ensure annual benefits can be covered, professional actuaries prepare these reports to estimate the funding required via contributions. They use long-term projections and statistical inference, including demographic changes, interest rates, and miscellaneous factors, to develop actuarial assumptions and valuation methods. These reports are critical for the long-term continuation of employee benefit plans.

Key Takeaways

- An Actuarial Valuation Report is an estimation of a pension plan's liabilities, assets, funding status,

- and future financial obligations based on assumptions about demographic trends, investment returns, salary increases, mortality rates, and other relevant factors.

- It offers a broad assessment of the financial status of public retirement schemes and pension plans and helps strategize a plan’s funding.

- It considers the Actuarially Determined Contribution (ADC) Rates, showing the funds needed to back promised benefits.

- These reports outline the impact of employee benefits on a company's financials, including net benefit costs, analysis of actuarial gains/losses,

- balance sheet recognition, current and non-current provisions, changes in present value, reconciliation of balance sheet items, and employee profile.

Actuarial Valuation Report Explained

An actuarial valuation report for a gratuity or pension is a technical, financial evaluation that examines the financial position of a pension plan, gratuity, or any other retirement plan by comparing its liabilities with assets. A professional actuary prepares this report using techniques like inferential statistics and inflation. It plays a vital role in establishing the funding status of a defined-benefit pension fund. It relies on inputs like rates of contribution of employees and employers, mortality rate, investment growth rate, demographic trends, salary increases, and other relevant factors.

It estimates future liabilities or assets at a given point in time based on mathematical analysis. Actuaries perform these valuations based on varied inputs and assumptions that help project the estimated cash flows related to the benefits payable to a retirement plan’s members. For this, the plan’s financial stability and standing are continually monitored. The funding ratio, calculated as the assets-liabilities ratio, signals whether the assets under a given pension plan are enough to cover its total liabilities. A ratio of 1.00 indicates adequate funding.

It has various important implications for pension funds and retirement plans. If a plan has less than a 100% funding ratio, it means there is a deficit, whereas if a plan has more than 100%, it represents a surplus of assets. These assumptions also help identify funding-related risk exposure and recommend to a plan’s sponsors the contributions needed to cover the promised benefits. Additionally, they help plan sponsors make decisions that promote long-term sustainability.

These reports help manage financial risks and make judicious decisions about pension funding. They also help manage insurance claims for insurance portfolios of companies, government entities, and insurance companies. Using statistical models and historical data, risk exposure and claim costs can be estimated. It enables entities to set appropriate insurance premiums.

Additionally, these reports help align leadership decisions with business goals by offering insights into the financial health of retirement frameworks. They also enable companies to comply with Generally Accepted Accounting Principles (GAAP).

Role

In this section, let us discuss the multifaceted role these reports play, promoting the goals of every stakeholder involved in pension schemes and employee benefit plans.

- Actuarially Determined Contribution (ADC) Rate: It serves as the basis for ADC along with the funded status of pension and Other Post-employment Benefits (OPEB).

- Financial reporting: After the implementation of GASB Statement No. 68 (which is Accounting and Financial Reporting for Pensions), these reports gained prominence in pension funding data. This is because the information derived through such analysis does not appear on financial reports in the natural course of reporting. It has to be specifically assessed and included.

- Annual funding: It informs decisions about the annual funding requirements to sustain pension or other employee benefit plans.

- Mandatory contributions: They help calculate mandatory contributions to pension plans and monitor the progress pension plans continue to make over the years to be able to fund obligations in the future. Hence, decision-making depends on such reports.

- Report interpretation and stakeholder communication: Relevant entities and professionals interpret actuarial reports and present them to the public and other stakeholders in an easily comprehensible format.

- Organization-level compliance and reporting: Employers need timely reports to ensure they can make funding arrangements or revisions to their existing strategy to ensure pension plans remain intact. Actuaries help them secure their plans through precise actuarial reports.

- Experience studies: Experience studies, say every 5 years or over any other relevant period, helpadjust funding or contributions to ensure they conform with actuarial valuations. This aligns a plan’s potential sustainability with its experience (in terms of funding performance) to date.

How To Read?

Every report has different sections. Let us discuss how such reports can be read in general.

- Introduction: Actuarial principles and accounting standards determine employee benefits. Hence, the introduction shows the aspects that a given report will cover—scope and purpose.

- Impact on Financials: A company's profit & loss account, along with its balance sheet, is affected by the liabilities of employee benefit schemes. Hence, such reports include expenses, interest charges, service costs, etc., to show the effect on profit & loss accounts.

- Actuarial Valuation Report Components: The actuarial valuation report has various tables to record relevant disclosures. These have been discussed below.

- Table 1 - Net Benefit Costs: It represents the net employee expenditure related to the employee benefit plan. Interest costs and service costs are shown separately to facilitate analysis.

- Table 2 - Analysis of Actuarial Gain/Loss: It divides actuarial gains and losses due to experience, demographic factors, and financial adjustments. This table helps readers understand the factors that drive any changes that will likely be seen over the years in a given pension plan.

- Table 3 - Balance Sheet Recognition: It contains the closing liabilities, surplus/deficit, and assets, as seen on the balance sheet.

- Table 3A - Current and Non-Current Provisions: This section categorizes funded and unfunded liabilities as current and non-current elements, respectively, helping relevant parties understand when a plan’s payment obligations will arise or fall due.

- Table 4 - Changes in Present Value of Defined Benefit Obligation (DBO): It shows the reconciliation of changes, which is based on the movements reported in a pension plan’s assets and liabilities in a specific reporting period.

- Table 5 - Reconciliation of Balance Sheet Items: It shows the reconciliation of net assets, taking into account profit & loss figures and contributions. This indicates a plan’s position relative to the entity’s financial position.

- Table A - Employee Profile: It contains information about existing employment data in the form of current statistics. It covers discontinuance gratuity and present-year employees.

- Conclusion: Appendices list actuarial assumptions and additional disclosures for comprehensive understanding. This section helps stakeholders understand the report’s findings.

The above details are commonly found in several actuarial valuation report samples. Besides these elements, it includes long-term projections, interest rates, demographic changes, and miscellaneous factors to ensure accuracy during financial planning.

Examples

Let us study some examples to delve deeper into the topic.

Example #1

Suppose Aylee is an actuary who was asked to prepare an actuarial valuation report for Rapidity Limited’s pension fund as of 31 December 2023. After an in-depth investigation, Aylee found that the plan was adequately funded at 115%, indicating that the assets were enough to cover the company’s estimated liabilities.

The net liabilities of Rapidity Limited stood at $10 million, and the plan assets were at $11.5 million, which exceeded the liabilities by a good margin. However, Aylee noticed that in 2028, several employees are set to retire. Hence, she suggested that the company must maintain a contribution of $5000 per employee to sustain the long-term viability of the pension fund.

She recommended this plan of action to ensure that the plan did not suffer adverse consequences in later years when a large chunk of employees were set to retire, which would mean that the pension and other employee benefits would become payable to them.

Example #2

A New York City Comptroller report published in November 2023 discussed state/public retirement systems and shared reports of an actuarial examination. The following pension plans were studied:

- New York City Employees’ Retirement System (NYCERS)

- Teachers’ Retirement System of the City of New York (TRS)

- Board of Education Retirement System of the City of New York (BERS)

- New York City Police Pension Fund (POLICE)

- New York City Fire Pension Fund (FIRE)

Since these are public retirement systems, their evaluation is critical to the well-being of the members or participants enrolled in each of these plans. The actuarial team presented a detailed evaluation covering data from June 30, 2019, and June 30, 2020.

The report evaluated economic assumptions, funding policy parameters, and actuarial standards. As of 1 January 2022, the assumptions were considered reasonable, and no adjustments were recommended. Funding policy elements were found to align with actuarial standards, including adherence to a white paper published by the Conference of Consulting Actuaries titled Actuarial Funding Policies and Practices for Public Pension Plans.