Part of our Fixed Assets and Depreciation guide

Depreciation for Computers Definition

Depreciation for Computers means an amount which is written-off from the cost of computers each year equally or calculated on written down the value by a business enterprise over the useful life of computers to change them as. When they become less useful over some time, in other words, it refers to reducing or providing an amount to decrease the value of computers and to report profits accurately.

How to Calculate?

The depreciation for computers can be calculated using the Straight Line Method and WDV Method of Depreciation.

The difference between the methods mentioned above is that in the straight-line method, the fixed amount is calculated equally to be written off every year until the value reaches zero.

In the written down value method, a different amount based on the amount calculated based on written down value or the opening value of an asset for the year for which depreciation is to be calculated is charged as depreciation. The amount charged in the initial years is high in the written-down value method. It can be derived by using the following steps:

Step 1: Calculate the total value of computers on which depreciation is to be calculated.

Step 2: Determine the rate of depreciation at which the depreciation is to be charged or provision for depreciation is to be made.

Step 3: Finally, take the product of the total cost of computers purchased with the depreciation rate for the period of use during the year. Mathematically, it is represented as:

Depreciation = Written Down Value * Rate of Depreciation * Number of Days or Months/365 or 12 Months.

Examples of Depreciation for Computers

Let’s discuss the following examples.

Example #1

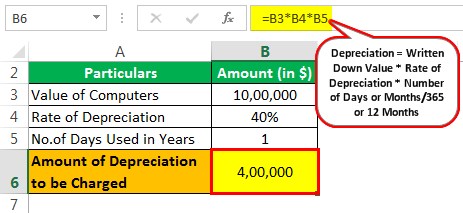

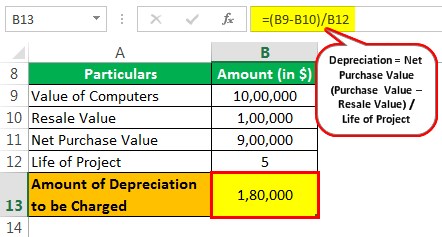

ABC inc. purchased computers for $1,000,000 on 01.04.2019. The project has a life of 5 years. At the end of the project, the purchased computers could be sold for $100,000. The depreciation rate per governing law is 40% p.a. We have to calculate the value of depreciation to be charged as of 31.03.2020.

Solution:

Now, the amount of depreciation as per written down value method as on 31.03.2020 is as follows:

- Depreciation = $(1,000,000 * 40% * 1 year) = $400,000

- The amount of depreciation to be charged as on 31.03.2020 is $400,000.

Amount of depreciation as per the straight-line method as on 31.03.2020 is as follows:

- Depreciation = $(1,000,000 – 100,000) / 5 = $180,000

- The amount of depreciation to be charged as on 31.03.2020 is $180,000.

Example #2

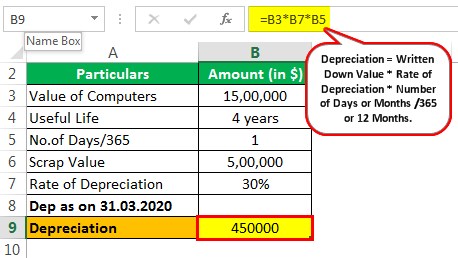

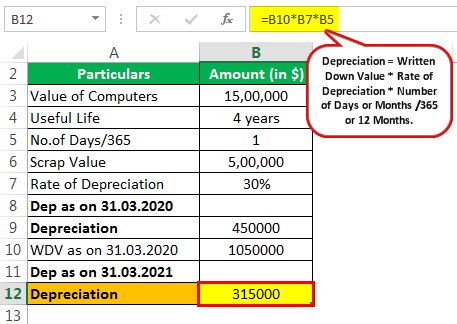

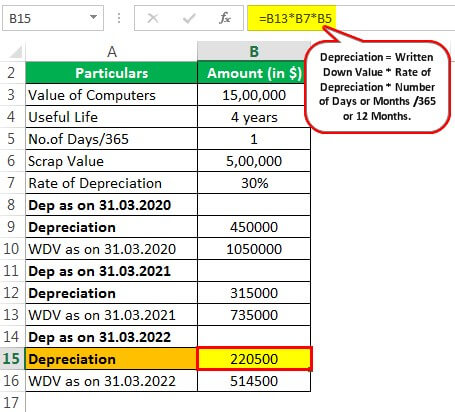

PQR INC. had computers that had written down value (WDV) as of 01.04.2019 is $1,500,000. The remaining project life is four years. After the project life ends, the computers could be sold for $500,000. The depreciation rate per governing law is 30% p.a. We have to calculate the value of depreciation to be charged using the written down value method as on 31.03.2020, 31.03.2021, and 31.03.2022.

Solution:

Now, the amount of depreciation as per Written down Value method as on 31.03.2020 is as follows:

- Depreciation = $(1,500,000 * 30%* 1 year) = $450,000

- The amount of depreciation to be charged as on 31.03.2020 is $450,000.

- Written down value as on 31.03.2020 = $(1,500,000 – 450,000) = $1,050,000

The amount of depreciation as per the Written down Value method as of 31.03.2021 is as follows:

- Depreciation $(1,050,000 * 30% * 1 year) = $315,000

- The amount of depreciation to be charged as on 31.03.2021 is $315,000.

- Written down value as on 31.03.2021 = $(1,050,000 – 315,000) = $735,000

Amount of depreciation as per Written down Value method as on 31.03.2022 is as follows:

- Depreciation = $(735,000 * 30% * 1 year) = $220,500

- The amount of depreciation to be charged as on 31.03.2022 is $220,500.

- Written down value as on 31.03.2021 = $(735,000 – 220,500) = $514,500

Rate of Depreciation for Computers

In India, as per the provisions of Income Tax Act, 1961, the rate of computer depreciation for computers was 60% p.a. which was later revised to 40% p.a.

Recommended Articles

This article has been a guide to Depreciation for Computers. Here we discuss how to calculate depreciation for computers with examples and their rate. You can learn more about it from the following articles –