Part of our Fixed Assets and Depreciation guide

What Is Asset Retirement Obligation?

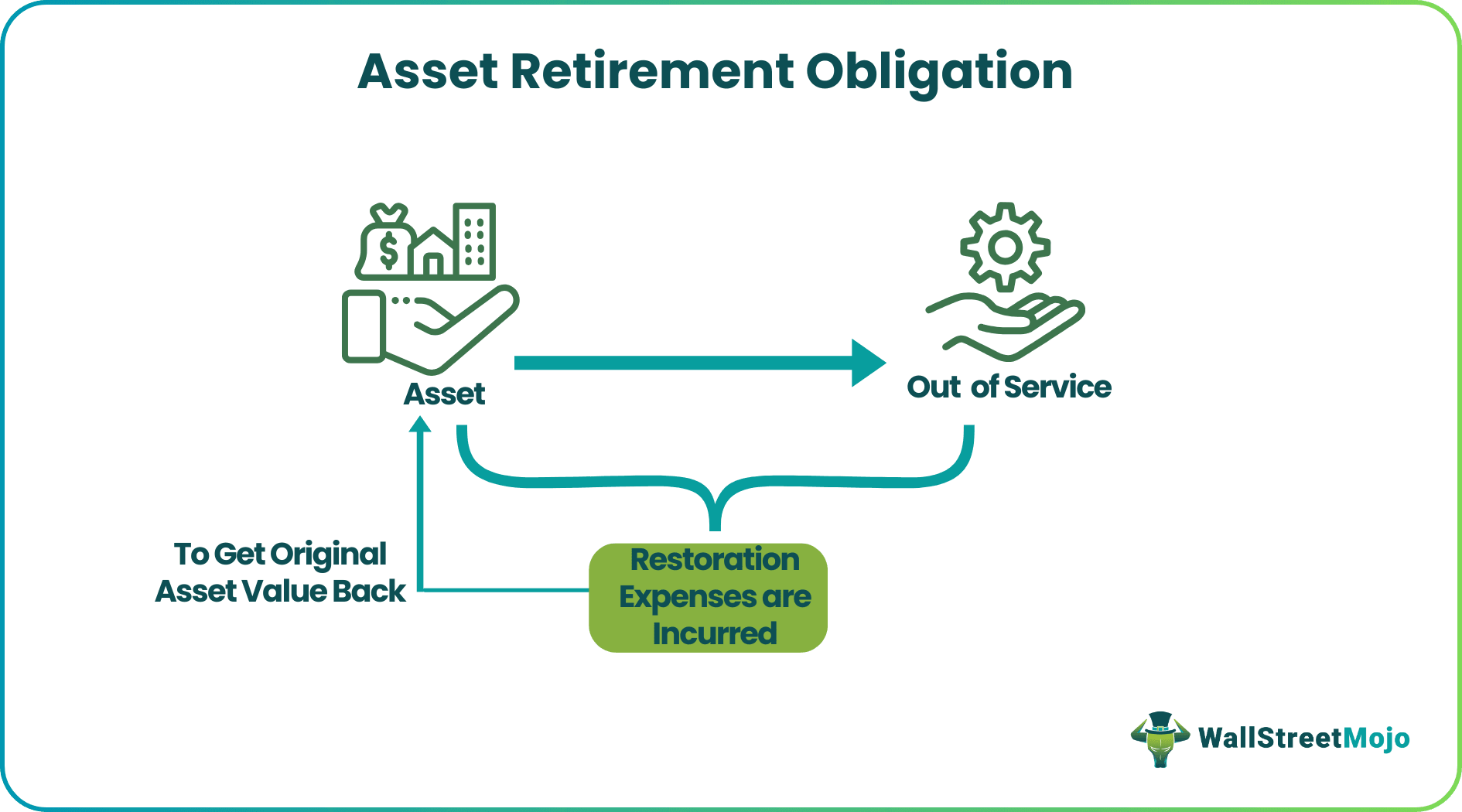

Asset Retirement Obligation is a legal and accounting requirement. A company needs to make provisions for the retirement of a tangible long-lived asset to bring the asset back to its original condition after the business is done using the asset.

Asset Retirement Obligations are essential from an accounting point of view. Had it not been the regulatory requirement, businesses would have used their discretion in disclosing these costs. It could have hurt the stakeholders badly as these costs could cause a severe drain on the company’s cash balances and may adversely impact the business. Accounting for the obligation well in advance gives the business the time to plan and set aside resources for the event.

- Asset retirement obligations are a requirement in terms of law and accounting. When a firm is finished utilizing a long-lived physical asset, the corporation must establish plans to retire the asset and restore it to its original state.

- FASB and IFRS in the US have guidelines for identifying and accounting for asset retirement obligations. They offer clear instructions on how to handle them.

- Obligations are crucial for businesses to disclose charges adequately. Failing to do so can hurt financial reserves and stakeholders. By providing notice, companies can plan and allocate resources in advance.

Asset Retirement Obligation Explained

Companies in several industries have to bring an asset back to its original state after the asset is taken out of service. It may involve oil drilling, power plants, mining, and many other industries. It also applies to the properties taken on lease, where the properties have to be brought back to their original shape. After the use, the asset may have to detoxicate like in nuclear plants, or machinery must be removed like in oil drills. The expected expenses to be incurred on such restoration are taken care of by the conditional asset retirement obligation.

The restoration expenses are incurred at the end of the asset’s useful life. However, a discounted liability is created on the balance sheet and a corresponding asset right after construction or initiation of the project; or on the determination of the fair value of restoration. This liability is then gradually increased at a fixed rate to match the expected obligation at the end of the asset’s life.

The recognition and accounting of asset retirement obligations are published by the Financial Accounting Standards Board (FASB) in the United States and the International Financial Reporting Standards in the rest of the world. These institutions provide detailed guidelines on the treatment of Asset Retirement Obligations excel.

For the right measurement of the liability, the company must determine the liability’s fair value when it incurs it. If the fair value of the liability cannot be determined, the liability should be recognized later when the fair value becomes available. Prompt recognition of the liability can benefit stakeholders as these liabilities are high-value liabilities, asset retirement obligation calculation and recognition shows a better picture of the liabilities.

Accounting

Accounting for asset retirement obligation requires recognizing the present value of the expected retirement expenses to be recognized as a liability and fixed asset. The liability is then increased every year at the risk-free rate and measured at subsequent periods for the change in expected cost. The interest rate used for discounting is the risk-free rate adjusted for the effect of the entity’s credit standing.

The asset recognized on the balance sheet is depreciated, and the expense is recorded on the income statement. The increase in liability is recognized as an accretion expense on the income statement and is calculated by multiplying the liability amount by the risk-free rate. Any change in the expected expense is adjusted to the liability balance after every revision of the conditional asset retirement obligation.

Proper accounting for the above process ensure the fact that the companies account for the future cost of the assets that are no longer useful, in a proper and responsible manner and are also correctly reported in the financial statements.

Accounting for asset retirement obligation provides a transparent picture of the company to the investors, creditors and any other stakeholder, which informs them about the potential costs and liabilities in the business’s long term asset. Further, proper recognition of the retiring asset enable companies to manage and make plans regarding the financial impact of the retired asset.

Example

Assume a power company builds a power plant with a 50-year lease at a site. The asset takes three years to be built and has to be necessarily retired at the end of 47 years after it was built. The cost of dismantling the equipment, detoxifying the site, and cleaning the site is $50,000 in today’s dollars. Because retirement has to be done after 47 years, this cost will be higher at that time. Consider that the retirement cost will increase at the rate of inflation. Assuming an inflation rate of 3%, the cost of retirement at the end of 47 years will be $200,595. Assuming a risk-free rate of 7%, the present value of this obligation comes out to be $8.342. See the illustration below for details of the asset retirement obligation calculation.

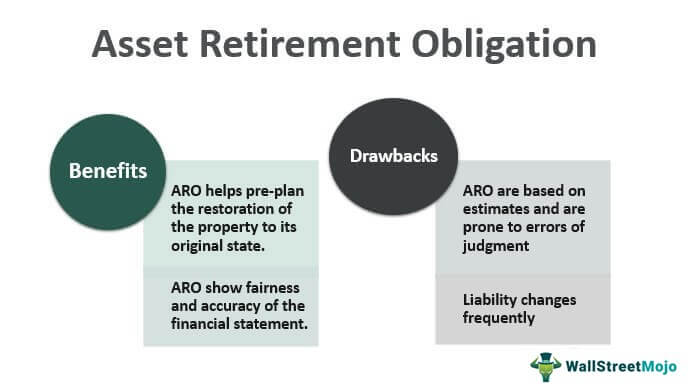

Benefits

Just as every financial concept has some benefits as well as limitations, so does this concept. Now, let us try to identify the benefits of the same.

- The obligation will be a real and significant expense; it makes sense to provide for the expense as soon as the liability’s fair value can be determined.

- It helps pre-plan the restoration of the property to its original state.

- It shows the fairness and accuracy of the financial statements.

Drawbacks

Here are some important drawbacks that should be considered in the process.

- Asset retirement obligations excel are based on estimates and are prone to errors of judgment.

- Liability changes frequently.

- The rates used while recognizing the liability may change going forward and may lead to a change in the liability.

- These obligations do not cover work done after other events that affect the assets like natural calamities (earthquakes, floods, etc.)

Accounting Treatment In US GAAP Vs IFRS

The accounting treatment of the retired asset under the two methods given above are different. Let us identify the differences between them.

| Subject | US GAAP | IFRS |

|---|---|---|

| Initial Measurement of Asset Retirement Obligation (ARO) Liability | The fair value is recognized as a liability when it becomes available. The discount rate used is the risk-free rate. | The liability is measured as the best expenditure estimate to settle the obligation discounted at the pre-tax rate. |

| Asset recognition from ARO | ARO amount is added to fixed assets at the time of the estimate. | Generally included in property plant and equipment. Recognized in inventory if incurred when the property was used to produce an inventory. |

| Subsequent Measurements | Revision is done from time to time to either the amount or timing of cash flows. Upward and downward revisions are discounted using current and actual risk-free rates. | Checked for change on every balance sheet date. The expected cash flow and the discount rate can be changed, and adjusted liability can be shown based on new assumptions. |

Frequently Asked Questions (FAQs)

Are asset retirement obligations tax deductible?

The long-lived physical asset and the ARO obligation have different book and tax bases since, in most cases, these liabilities are not tax deductible when recorded for financial statement reporting.

Is asset retirement obligation a liability?

Asset retirement obligations (AROs) are liabilities related to the eventual retirement of fixed assets. Restoring a site to its initial state is sometimes a legal necessity.

What is rule no 143 accounting for asset retirement obligations?

Under FAS 143, if a reasonable estimate of fair value can be established, the fair value of the asset retirement obligation (ARO) liability must be recognized in the period it is incurred. The retirement of long-lived physical assets is subject to AROs, which are legal responsibilities.

Recommended Articles

This article has been a guide to what is Asset Retirement Obligation. We explain the accounting with example, benefits and drawbacks. You may learn more about Financing from the following articles –