Part of our Fixed Assets and Depreciation guide

What Is Depreciation For Rental Property?

The depreciation of the rental property can be termed as the reduction in the rental property value over time due to wear and tear, age and deterioration. It is a systematic allocation of costs and could be used to write off the taxes. And therefore, it helps in lowering taxes.

The depreciation on the rental property offers a tax deduction to be claimed under schedule E of the internal revenue service. Therefore, this helps in the proper tax planning of the individual. Once the owner has sold the rental property, he can no longer claim depreciation on the rental property.

Depreciation For Rental Property Explained

Depreciation for rental property offers huge tax advantage, thereby making the real estate investments profitable for investors. The depreciation can be regarded as a non-cash expense that helps write off tax expenses, and it is an easier way to record the asset’s cost on the income statement.

When an owner purchases a real estate property, they have to work on improvement as days pass by. This helps them to keep the property in a sound condition so that it is of good value even after years of depreciation for rental property. Through this method, the owners get an opportunity to claim tax benefits for the expenses incurred for improvement.

Investors invest in a rental property and real estate with the intent of financial planning and having sustainable positive cash flows. The rental property can be utilized for both sustainable cash flows in rent, and enhanced equity value as the property rises in value. It makes liability of taxes as it is an expense that covers the cost of an asset and improves the rental property.

- As per the broad rules of the Internal revenue service IRS, the rental properties can be assumed and treated to have a useful life of 27.5 years.

- To arrive at an effective depreciation value, divide the cost of the rental property by the factor of 27.5.

- If a rental property is in the form of commercial property, then the useful life can be assumed to be up to 39 years.

- Land can never be utilized for depreciation; rather, the buildings and properties built on it would be regarded for depreciation.

- The land is considered to have an indefinite useful life.

- A fair tax assessment helps determine the effective value of the land.

- The depreciation is valid until the time the individual owns it. Once it is sold, the individual can claim depreciation on it.

- The individual or the owner can start accounting for depreciation once the rental property is ready for the rental business.

How To Calculate?

To calculate the value of IRS depreciation for rental property, one can determine it as the division of cost basis of the rental property with a useful life.

The following would be the relationship: –

Depreciation = Cost of the Rental Asset / Useful Life of the Asset

Moving forward, there are a few elements that need to be computed first for the formula to work better. Let us have a look at them below:

- Calculate cost basis of depreciation for rental property

The first thing is to figure out the cost of the real estate property. Cost basis is the difference between the property value and the value of the land the property stands on plus closing costs (depreciating).

- Depreciation expense of the property in question

This is the amount that is calculated by dividing the cost basis amount by the years of rental property depreciation, which, according to the IRS, is 27.5 years. These years mark the useful life of the property.

Rules and Requirements

The IRS lists down a few rules that make depreciation for a rental property work for a property owner. Some of them have been mentioned as follows:

- As per the IRS, the individual should own the depreciation property.

- The utilization of the property is for business purposes or income generation activity.

- There is a determined useful life of the property wherein the property is anticipated to have a useful life of more than one year. The standard value is 27.5 years for residential property.

- It defines and categorizes which types of properties can be depreciated and would be considered for a tax deduction.

- The property doesn’t need to be depreciated if it is put into service and disposed of in the same year.

- One should note that the land cannot be depreciated.

- The depreciation costs cannot include clearing costs, planting costs, and costs of landscaping.

- The effective cost of the property is termed the cost basis.

- The cost basis of the rental property is composed of any assumed debts corresponding to the property, legal costs in the acquisition of the property, fee of recording, the survey costs on the property, taxes on ownership transfers, and costs of title insurance.

- One can adjust this cost over the lifetime of the property.

- Legal costs are the costs that the individual has to bear to acquire the rental property.

- The recording fee is the fee payable by the individual to a government agency. It is for property registering or recording the sale of rental property.

- The survey fee is the fee that an individual has to bear towards inspecting the rental property.

Examples

Below are some examples explained in detail.

Example #1

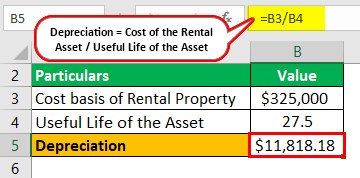

Let us take the example of residential property. The cost basis of rental property is $325,000. Per the IRS guidelines, it is assumed that the residential property would have a useful life of 27.5 years. A straight-line depreciation method, helps the owner determine the depreciation on the rental property.

Solution:

- = $325,000 / 27.5

- = $11,818.18

Therefore, the depreciation is $11,818.18.

Example 2

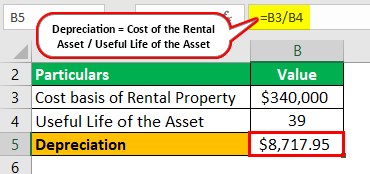

Let us take the example of commercial property. The cost basis of rental property is $340,000. Per the IRS guidelines, it is assumed that the residential property would have a useful life of 39 years. A straight-line depreciation method helps the owner determine the depreciation on the rental property.

Solution:

- = $340,000 / 39

- = $8,717.95

Therefore, the depreciation is $8,717.95.

Advantages

Depreciation for rental property Is easy to calculate and with the guidelines provided by the IRS, the requirements related to the type of real estate properties that are eligible for these benefits, are clearer. The merits of this method have been mentioned below:

- The rental property could be utilized for effective tax planning.

- The rental property could be utilized for comprehensive retirement planning.

- With time, the value of the rental property appreciates.

- If the acquired rental property is in the best and most desirable location, it helps create a steady stream of cash flows for the owner.

- Other rental property-related expenses and depreciation have to be reported in Schedule E of the tax returns to benefit from the deductions on the rental income stream.

Disadvantages

Besides the benefits that helps property owners know how the method can enable them make profits, there are multiple demerits too that one must be aware of. Listed below are some of them. Let us have a quick look at them:

- If the owner has undertaken the rental property at an undesirable location, it is difficult to generate a steady income stream.

- The above situation can reduce the net investment which, in turn, increases the depreciation expense.

- Other rental property-related expenses can’t be recovered as there is an insufficient generation of an income stream from the rental property.

Recommended Articles

This article has been a guide to what is Depreciation For Rental Property. Here, we explain how to calculate it along with its examples, advantages & disadvantages. You can learn more about financing from the following articles –