Part of our Fixed Assets and Depreciation guide

What is the Sum of Years Digits Depreciation Method?

Sum of years Digits Methods or the sum of year depreciation method is an accelerated depreciation method whereby the method declines the asset’s value at an accelerated rate. Most of the depreciation of an asset is recognized in the first few years of its useful life. Therefore greater deductions are allowed in the starting life of the assets than in subsequent years, mainly in the case of those assets which are heavily used when they are new.

Although, the amount of depreciation remains the same whether the Company uses the straight-line depreciation method, double declining balance method, or the sum of year digits method. It is just that the amount of timing of the depreciation differs in all three approaches.

- The sum of the year’s digits method causes the Company’s net income variability. The assets are depreciated at a higher rate in the early years, and thus, the net income is lower in the early life of the asset. But as the useful life of the asset increases, the reported net income increases.

- However, using this method can indirectly impact the company’s cash flows. Since the depreciation amount is higher in the initial years, the reported net income is lower; hence, the tax implication is lower.

Steps to Sum of Years Digits Method

Below are the steps to the sum of years digits method –

- First, calculate the depreciable amount, which is equal to the asset’s total cost of acquisition minus thesalvage value. The acquisition cost is theCAPEXthe company had made to acquire the asset. Depreciable amount = Total acquisition cost – Salvage Amount.

- Calculate the Sum of Useful Years of the Asset.

- The depreciation amount is multiplied by a depreciation factor each year. The depreciation factor is the asset’s useful life divided by the sum of the good years of the asset.

- Thus, the Sum of years depreciation = Number of useful years/sum of useful years * (Depreciable amount)

- Let us say the useful life of an asset is 3. Then, the sum of useful years = 3 + 2 + 1 = 6. Thus, the factors for each year will be 3/6, 2/6, and 1/6, respectively, for the 1st, 2nd, and 3rd

Sum of Years Digits Method in Video

Sum of Years Digits Method Example

Let us understand the concept with an example below:

A Computer Company has purchased some computers worth $ 5,000,000. It cost them $ 200,000 to transport the Computer to their location. The Company considers that the useful life of Computers is five years and they can expire the computers at a value of 100,000.

Now, considering the above example, let us create a depreciation schedule for the asset using the Sum of year depreciation method.

Step 1 – Calculate the Depreciable Amount

- Total Acquisition Cost = 5000000 + 200000 = 5200000

- Salvage Value = 100000

- Useful life of Computers = 5 years

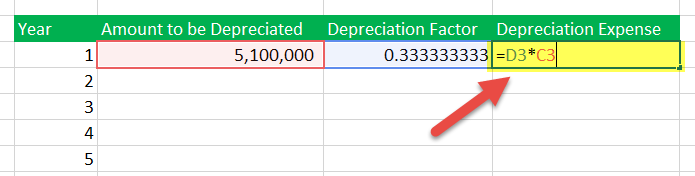

- Depreciation Amount = Acquisition Cost – Salvage Value = 5200000 – 100000 = 5,100,000

Step 2 – Calculate the Sum of Useful Life

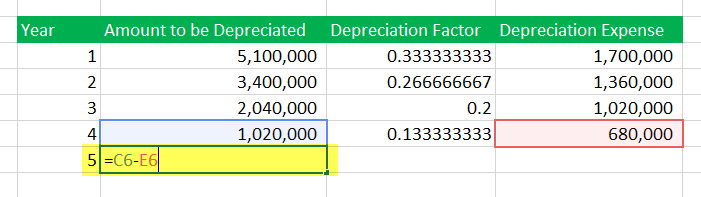

Sum of useful life = 5 + 4 + 3 + 2 + 1 = 15

Step 3 – Calculate Depreciation Factors

The depreciation factors are as follows

- Year 1 – 5/15

- Year 2 – 4/15

- Year 3 – 3/15

- Year 4 – 2/15

- Year 5 – 1/15

Step 4 – Calculate Depreciation for each year.

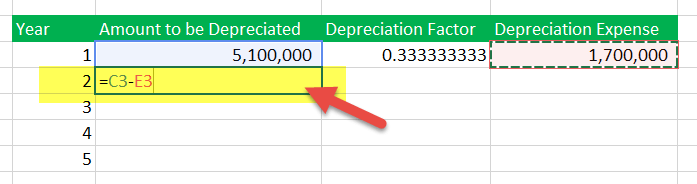

The depreciation expense of first year = $5,000,000 x 5/15 = $1,700,000

The amount left to be depreciated is calculated as $5,100,000 – $1,700,000 = $1,360,000

Likewise, we can calculate the depreciation expense for years 2, 3, and 4.

Year 5 depreciation is not calculated using the depreciation factor. As it was the well last year, we depreciate the full amount left for depreciation. In this case, it is $340,000

As seen from the above depreciation schedule of the year depreciation method, the depreciation expense is highest in the early years. It keeps decreasing as the asset life increases, and it becomes obsolete.

Advantages

- The sum of years digits method helps match the asset’s cost and benefit, which provides over the useful life of an asset. The benefit of the asset declines as its useful life decreases and the asset grows older. Thus, charging the asset’s cost higher in the early years and reducing the amount as years pass by reflects the economic condition and benefits from the asset.

- When the asset grows older and has been used for some good years, its repair and maintenance costs rise. The rising repair and maintenance costs can offset the low depreciation cost of the asset in the later period of its useful life. The repair costs are lower in the initial years, and the depreciation amount is high and vice versa. Suppose accelerated depreciation or the sum of year depreciation method is not used. In that case, the earnings might be distorted and vary as the depreciation charge will be lower in the initial period. During the end of the useful life of an asset, the charges will rise due to repair costs, thus decreasing the earnings.

- The sum of year digits method provides a tax shield, especially during the initial years. Since the depreciation expense is high, the Company can report lower net income, thus decreasing the tax expense.

- The sum of the year depreciation method is useful for depreciating an asset that may become obsolete quickly. E.g., Computers can become obsolete quickly due to technological advancements; thus, it makes sense to charge the expense in the early years of useful life.

Conclusion

The sum of years digits method is an accelerated depreciation method that can be used to depreciate the asset’s value over the useful life. The sum of the year depreciation method aims to depreciate the asset at an accelerated rate, i.e., higher depreciation expense in the early years and lower depreciation expense in later years. It is useful for deferring tax payments, especially for assets with a lower useful life, and may quickly become obsolete.

Recommended Articles

This has been a guide to what is the Sum of Years Digits Method of Depreciation. Here we discuss the steps to calculate the sum of a year’s depreciation along with practical examples and advantages. You may learn more about accounting from the following articles –