Part of our Fixed Assets and Depreciation guide

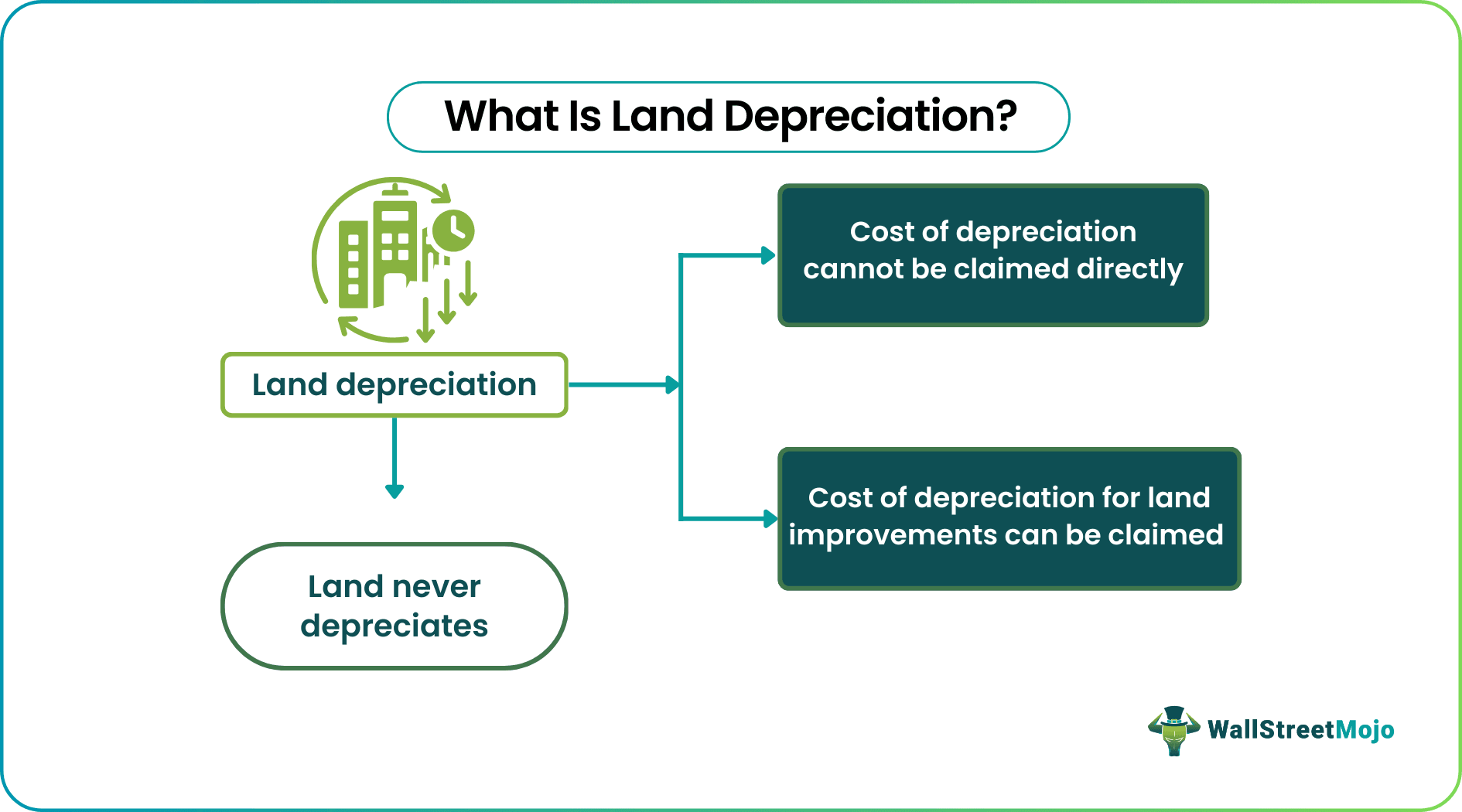

What Is Land Depreciation?

Land depreciation is a concept that is not practically used, but if indirect references are made, it may help owners to account for it. The depreciation cost is not applicable to a land property directly as it does not have a specified useful life, which makes it difficult to compute the cost of depreciation for it.

The land is an asset of the company which is having an unlimited useful life; therefore, no depreciation applies to the land, unlike the other long-term assets such as buildings, furniture, etc., which have a limited useful life and hence their costs to be allocated to the accounting period in which they are of some use to the company. But land, although a tangible fixed asset, does not depreciate.

Land Depreciation Explained

Land depreciation may not have a direct practical utilization, but firms can make such claims in certain scenarios. Depreciation is an important calculation in accounts. The amount deducted from the value of any tangible asset in cash flow or a balance sheet at any point in time can be claimed as a non-taxable item. As it gets reduced from the asset’s value, the tax, which is calculated on revenue after all deductions and additions, excludes depreciation.

However, everything said and done, it is important to understand that “Land does not depreciate.” In a literary sense, it does depreciate, meaning there may be deterioration in its value; however, from an accounting point of view, we cannot pass any entries in the system for such deterioration in the name of depreciation. When we use the term depreciate here, we sincerely refer to the accounting term “depreciation.”

Land cannot deteriorate in its physical condition; hence we cannot determine its useful life. It is almost impossible to calculate land depreciation. The value of land is not constant on a long-term basis – it may enhance or may as well deteriorate. In other words, it is fluctuating. Hence, it gives an uncertain picture of the asset value, which is why calculations are difficult.

Though it is true that the land does not depreciate, the improvement or other activities conducted on that property is countable. Plus, such improvements have a useful life for which the cost of depreciation can be computed. Some of the examples of such improvements include, building a fence, driveway, or installing outdoor lights, etc. Hence, entities must not ignore ways in which they may claim for the lad depreciation costs.

Reasons To Claim

Despite land depreciation not being a direct part of the accounting process, it is recommended that entities claim for the costs of depreciation incurred in the land improvement procedures. The reason behind such claims being important are as follows:

- When the depreciation counts, it becomes a non-cash expense record in the income statement. This entry is tax-deductible, As a result, it offers tax benefits to firms by reducing the tax amount on the profits.

- The depreciation claim here can be made for older assets or properties. For example, a new owner can opt for improving an old property and can recoup the amount in the later stage.

- The businesses, by keeping such records, can have activities listed to track the processed enabling expansion.

Examples

Let us consider the following instances to understand the concept well and see how it works:

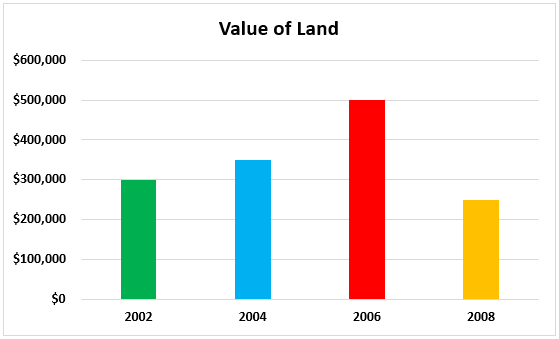

Example #1

In a hypothetical example, a value of a particular piece of land was $300,000 in 2002. After two years, the value increases steadily to $350,000. Due to the real estate boom in the location during 2006, the value went up to $500,000 (prices shooting up on the graph). However, due to a crisis in 2008, the value then went down to $250,000 (nearly half in 2 years). If a graph is drawn for these values, it would be like this:

In this case, the value of land fluctuates. Understanding from a depreciation point of view, an asset whose value reduces within a given period can be used for calculating depreciation.

Example #2

A piece of land was a marshy area in 2005. It was converted into usable land in 2008 when real estate products were at their peak by dumping sand and other material and were turned into a solid lot of land. The value of this piece went up manifold, and the land was in great demand. As and how developments were done, the property prices went up and up. In 2010, unfortunately, the land was hit by an earthquake, and the entire development made over the land was devastated. The land itself got worn out in a manner that could not be used again. In this case, the land value dropped drastically. It shows that although the land is vulnerable, its value cannot be periodically and equally reduced over time. Moreover, understanding this example, we can say that land does not have its own particular useful life. It was due to the earthquake in 2010 (which may have occurred in any other year later or earlier) that the value went down, or the development made in 2008 due to which its value rose high.

In accounting practices, depreciation can be calculated only for items with a particular value at the beginning of their useful life. That particular value deteriorates over some time. This is the reason why “land” does not qualify for depreciation.

Accounting Effects

The value of land can change over a period of time.

- As per the above example, the land was worth $1 million in 2015. If there are developments in the location which are beneficial for the value of the area, the value of this piece of land will go up to $1.5 million in 2018.

- On the other hand, if the same piece is agricultural land, and if there are natural calamities in the location due to which agriculture is unfavorable in the future, then its value goes down considerably. However, this loss in value cannot be termed as depreciation, one because it is unpredictable, second because it depends on an external force.

- Thirdly, it may happen that the value may again go up due to some other external factor. Hence, it is not right to call this change in value a part of depreciation.

- The land value reduction can be claimed only at the time of sale. If the landowner holds the asset, then a change in value will not affect or get claimed. However, if the value increases, profit can be claimed under capital gain, at the time of sale, and vice versa, the reduced value is claimed as a capital loss. Although land itself cannot depreciate, the assets on such land can always qualify for Land depreciation. Even though these other assets may cause the land value deterioration, they hardly have any significance over the depreciation aspect of this land.

- On the other hand, if the land needs improvements for such other assets, the cost of such improvements can also qualify for land depreciation. For example, Suppose the land currently serves as a dumping ground, and a developer wishes to construct a building over this land. In that case, there will be rubbish removal charges to the developer. It can be a lot of expense for him, and so he may opt for depreciating this expense over some time. It may be a capital improvement for the building to be constructed and so can be amortized over time.

Hence, the land per se does not affect depreciation, although the value of such land grows manifold after the building is constructed.

Recommended Articles

This has been a guide to what is Land Depreciation. Here, we explain the concept along with the examples, and accounting effects. You may learn more about accounting basics from the following articles –