Causes of Depreciation

Depreciation is the value reduction in the carrying amount of the fixed asset (or property plant & equipment) from period to period, which is charged in the statement of profit & loss of the organization for the same period to provide the reasonable cost of the asset which has been used during that period. Common causes of depreciation include wear and tear due to usage, compliance with accounting standards, technological advancements, etc.

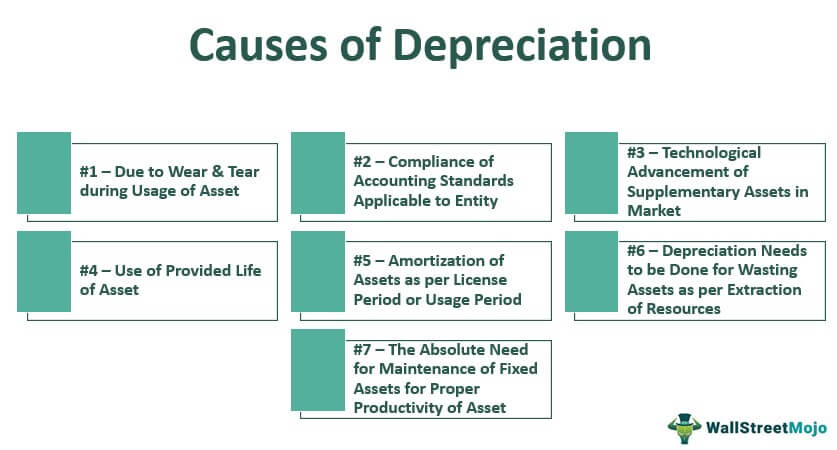

The reduction in the carrying amount of fixed assets throughout its useful life is due to many reasons. Some of them are as follows:

Key Takeaways

Top 7 Causes for Depreciation

#1 – Due to Wear & Tear during Usage of Asset

It is one of the primary reasons for the depreciation of assets. Most of the assets are worn off or deteriorate due to the continuous usage of the asset. Such as Plant & Machinery used to produce goods, buildings, vehicles, etc. As in the case of machinery used for production, the continuous usage & running of machinery, the working or production capacity of the machinery diminishes over the period & the value of the machinery also decreases in the market. So for the fair presentation of the entity’s financial position, it is necessary to reduce the proportionate value of the machinery in the books.

#2 – Compliance of Accounting Standards Applicable to Entity

As per the applicability of accounting standards to the entity, the entity needs to follow the provisions mentioned in the bars. It is done as per the matching concept that needs to be followed in the entity’s accounting. As per the matching concept, the depreciation is to be charged for the respective as the income through the asset has also been booked for the period mentioned above in the books of accounts.

#3 – Technological Advancement of Supplementary Assets in Market

The value of the fixed assets used by the enterprise gradually decreases if the new upgraded version of the asset with the better technological advanced features is present in the market, providing more benefits to the customer than the old obsolete version of the asset. In such a case, the requirement of the old asset gradually decreases, and so does its recoverable amount in the market. Hence it is necessary to show the value of the asset at a fair amount or reasonable amount in the financials.

#4 – Use of Provided Life of Asset

In some fixed assets, the useful life of the assets is provided in consumption units like an asset ‘X’ will run for 10000 hours. Hence the allocation of the asset’s cost is as per the consumption or its usage in hours.

#5 – Amortization of Assets as per License Period or Usage Period

Some of the assets like license, patent, copyrights, leasehold properties, etc., can only be used for the provided period. At the lapse of such time, the asset could not be used. Hence its cost needs to be allocated or amortized as per the usage period of the assets. At the end of the useful period, assets should be written off from the books of accounts.

#6 – Depreciation Needs to be Done for Wasting Assets as per Extraction of Resources

In case of wasting assets like coal mine, well of oils, etc., are amortized and used per the extraction of natural resources done from them during the period. In the case of such types of wasting assets, there are limited resources that an entity can extract from such assets for the organization’s use. Therefore, as per the estimated total extraction that will be done from the wasting asset and the amount already extracted, the respective period will be considered for the asset’s depreciation during that period.

#7 – The Absolute Need for Maintenance of Fixed Assets for Proper Productivity of Asset

The plant & machinery used in the manufacturing of products in a manufacturing company needs regular maintenance for full-time productivity to be received from the usage of such machinery. Even after a certain period, some essential parts of the machinery will be replaced with brand new parts. For such, the depreciation needs to be charged so that the parts that are to be replaced in the future are appropriately accounted for and written off during its life.

Conclusion

The companies act or the statutory laws allow the depreciation and amortization. It applies to the entity for writing off the used part or cost of the asset in the entity’s statement of profit & loss account of the entity for the period mentioned above as per the matching principle in accounting. There are many causes or reasons for doing such treatment. This matching concept provides a fair presentation of the financials of an entity as the cash inflow generated from the asset has been booked, and the respective usage cost of the asset is also written off during the same period as per the matching concept in accounting. The income tax laws and statutory laws (including accounting standards) mandate the treatment and chargeability of depreciation in the books of accounts for the respective period.

Recommended Articles

This article is a guide to the Causes of Depreciation. Here we discuss what depreciation is, and significant causes of depreciation include Due to Wear & Tear during Usage of Asset, Use of Provided Life of Asset, etc. You may learn more about financing from the following articles –