Owners Capital Definition

The money business owners (if it is a sole proprietorship or partnership) or shareholders (if it is a corporation) have invested in their businesses. Owners Capital is also referred to as Shareholders Equity. In other words, it represents the portion of the total assets funded by the owners/shareholders’ money.

Owners Capital Formula

It can be calculated as follows:

Owners Capital Formula = Total Assets – Total Liabilities

For example, XYZ Inc. has total assets of $50m and total liabilities of $30m as of 31st December 2018. Then Owners Capital is $20m (Assets of $50m fewer Liabilities of $30m) as of 31st December 2018. It can be interpreted from above that assets of $20m are funded by the Owners/ Shareholders of the business. The remaining $30m has been funded through externally sourced funds (i.e., loans from banks, issuance of bonds, etc.)

Components of Owners Capital

#1 – Common Stock

Common Stock is the amount of capital contributed by the company’s common shareholders. It is shown at the par value on the Balance Sheet.

#2 – Additional Paid-In Capital

Additional Paid-In Capital refers to the amount over and above the stated par value of the stock that the shareholders have paid to acquire the company shares.

Additional Paid-In Capital = (Issue Price- Par Value) x Number of Shares Issued.

Let’s assume that as of 31st December 2018, XYZ Company issued a total number of common shares of 10,000,000, having a par value of $1 per share. Further, assume that common shareholders paid $10 each to acquire all the company shares. In this case, additional paid-in capital would be reported at $90m (($10-$1) x 10,000,000)) under shareholder’s equity in the Balance Sheet.

#3 – Retained Earnings

Retained Earnings are the portion of net income available for common shareholders that have not been distributed as dividends. The company retains these for future investments and growth. Considering that the amount retained by the company belongs to its common shareholders, this is shown under shareholders equity in the balance sheet. It increases when the company makes profits and decreases when a company makes losses.

For example, if the company earned a net income (after paying preferred dividends) of $5m for the financial year ending 2018 and distributed $2m as dividends to its common shareholders. It means that the company’s management has decided to retain $3m in the company for its future growth and investments.

#4 – Accumulated Other Comprehensive Income/ (loss)

These are some income/expenses that are not reflected in the income statement. It is so because they are not earned incurred by the company but affect Shareholder’s equity Account during the period.

Here are some examples of items. Other Comprehensive Income includes unrealized gains or losses on available for sale securities, actuarial gains or losses on defined benefit plans, and foreign currency adjustments.

#5 – Treasury Stock

Treasury stock is the stock that has been reacquired by the company from the shareholders and thus reduces the shareholder’s equity. It is shown as a negative number on the Balance Sheet. There can be two methods for accounting treasury stock, i.e., Cost and Par Value Method.

Examples of Owner’s Capital Calculation

Below are the examples.

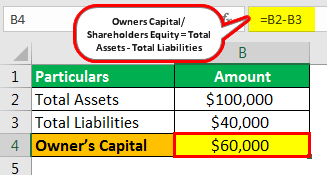

Example #1

Say ABC Ltd. has total assets of $100,000 and total liabilities of $40,000. Calculate the Owner’s Capital.

Calculation of the Owner’s Capital

- =$100000-$40000

- =$60000

Example #2

Let’s see a practical application. Tom runs a grocery store. He started it on 1st Jan’2019 with his savings of $40,000 and a loan he took from his uncle for $20,000. He purchased a laptop for $1,000; furniture for $10,000; stock for $45,000 and balance $4,000 was kept in bank for day to day expenses. At the end of the year, i.e., 21st Dec’2019, his balance sheet stood as follows:

| Liabilities | Amount ($) | Assets | Amount ($) |

|---|---|---|---|

| Owner’s Capital | 50,000 | Furniture | 9,000 |

| Loan | 20,000 | Laptop | 800 |

| Creditors | 1,200 | Stock | 55,000 |

| Bank | 6,400 | ||

| Total | 71,200 | Total | 71,200 |

How did these figures get changed? Let’s understand; Tom must have sold his stock at prices higher than the purchase price. He must have incurred expenses like electricity, insurance, accounts, finance charges, etc. Also, he might have made some connections, so he was able to purchase some stock on credit. All these events led to cash inflow as well as cash outflow. The profit he made after all these are now added to the Owner’s Capital.

Now, if we calculate Owner’s Capital by using the Assets – Liabilities formula, then we get:

- =$71200 – $21200

- =$50000

Change in Owner’s Capital

- #1 – Profit/Loss: The owner’s capital changes yearly due to profit or loss arising in business. Profit increases the owner’s capital while losing decreases it.

- #2 – Buyback: Buyback means the repurchase of capital the company once issued for various reasons such as idle cash, boosting financial ratios, etc. It results in a decrease in the owner’s capital.

- #3 – Contribution: The owner’s capital increases when existing or new owners contribute. When new owners enter the business, they contribute to the ownership they will acquire.

Advantages and Disadvantages of Owner’s Capital

Given below are some of the advantages and disadvantages of the owner’s capital.

Advantages of the Owner’s Capital

- #1 – No burden of Repayment: Unlike debt capital, there is no repayment burden in the owner’s capital. It is thereby considered a permanent source of funds. It helps management to focus on its core objectives and flourish the business. Given below are some of the advantages and disadvantages of the owner’s capital.

- #2 – No Interference: When a business has Debt as a major source of funds, the chances of interference by lenders are high. It can become a hindrance to the growth of a business. While in the case of the owner’s capital, management has sole discretion in deciding whatever is good for the business.

- #3 – No Impact of Interest Rate: If a company is highly dependent on variable rate debt capital, an increase in interest rate can significantly impact its cash flows, while in the case of the owner’s capital, there is no impact of changes in interest rate.

- #4 – Easy Accessibility to Debt Capital When the company has enough owner’s capital, it is always easy to get additional debt capital as it shows that the company is strong and working independently.

Disadvantages

- #1 – Higher Cost: The cost of the owner’s capital is the return such capital could have earned in any other investment opportunity. A tangible asset usually secures Debt Capital. Since business always possesses risk, the expected return from such capital is higher than the debt capital.

- #2 – No Leverage Benefit: Interest expense comes with the benefit of a tax shield, which means a company can claim it as a business expense. Like any other expense, it reduces the taxable profit. However, this tax saving is foregone in the case of the owner’s capital as the dividend doesn’t account for a business expense.

- #3 – Dilution: Raising the new owner’s capital dilutes the holding of existing owners. However, this doesn’t happen in the case of debt capital. Business can grow with the use of debt capital, and at the same time, the valuation of such a business doesn’t get diluted.

Conclusion

The owner’s Capital is a vital part of any business. It is the base upon which the whole company stands and grows. Business can be carried out with only the owner’s capital, debt, or a mix of equity and debt. An optimal mix of shareholders’ equity and debt is considered the best option for leverage benefits. However, the owner’s capital is highly appreciated when the cost of debt is higher than the return business provides.

Having a balanced owner’s capital shows that the company is secure and does not rely only on outsiders for its business.

Recommended Articles

This article has been a guide to Owners Capital and its definition. Here we discuss the formula to calculate the owner’s capital along with its components, examples, advantages, and disadvantages. You can learn more about finance from the following articles –