Double Entry Meaning

Double-entry is an accounting system thatrecords a transaction in a minimum of two accounts. It is based on a dual aspect, i.e., Debit and Credit, and this principle requires that for every debit, there must be an equal and opposite credit in any transaction. The double entry system is a more comprehensive way to maintain an entity’s overall accounts.

Double Entry is the first step in maintaining a complete set of accounting. If the transactions are recorded correctly, the profit and loss account and balance sheet will provide accurate and complete results.

Double Entry Explained

Double-entry is the first step of accounting. To understand any accounting entry, one should know about this system. Each accounting transaction is recorded in a minimum of two accounts, one is a debit account, and another is a credit account. Also, the transaction should be balanced, i.e., the credit amount should be equal to the debit amount.

When a business engages in a transaction, it records both the debit and credit aspects of the exchange in separate accounts. For instance, when a company makes a sale, it not only records the increase in its cash or accounts receivable (debit) but also acknowledges the corresponding increase in revenue (credit). This dual recording system serves several critical purposes.

Firstly, it helps prevent errors and fraud by necessitating a cross-verification of entries. If the books are not in balance, it signals an inconsistency that requires investigation. Secondly, double entry facilitates the creation of financial statements, enabling businesses to generate accurate reports that reflect their financial performance and position.

Therefore, the double entry accounting is the cornerstone of reliable accounting, providing transparency, accuracy, and a systematic approach to financial management, which is indispensable for informed decision-making and regulatory compliance.

Features

Let us understand the features of the double entry system through the discussion below.

- Two Parties: Two parties are involved, one is the receiver, and another is the giver. The receiving party is debited, and another party is credited. For example, A purchases goods from B, where A is a receiver party, and B is a giver party.

- Equal Effect: Each transaction should have an equal financial effect. The debit amount should be equal to the credit amount.

- Separate Legal Entity: This accounting system records the transaction separately from its owners.

- Debit and Credit: There are two aspects for recording any transaction, the Debit aspect, and the Credit aspect.

Principle

Double entry accounting is based on a simple principle, that for every debit, must have equal and opposite credit. There should be at least two accounts involved in any transaction.

Debit Side = Credit Side

The double entry is based on the debit and credit accounts of the transaction. So, we need to understand what account kind of debits and what credits.

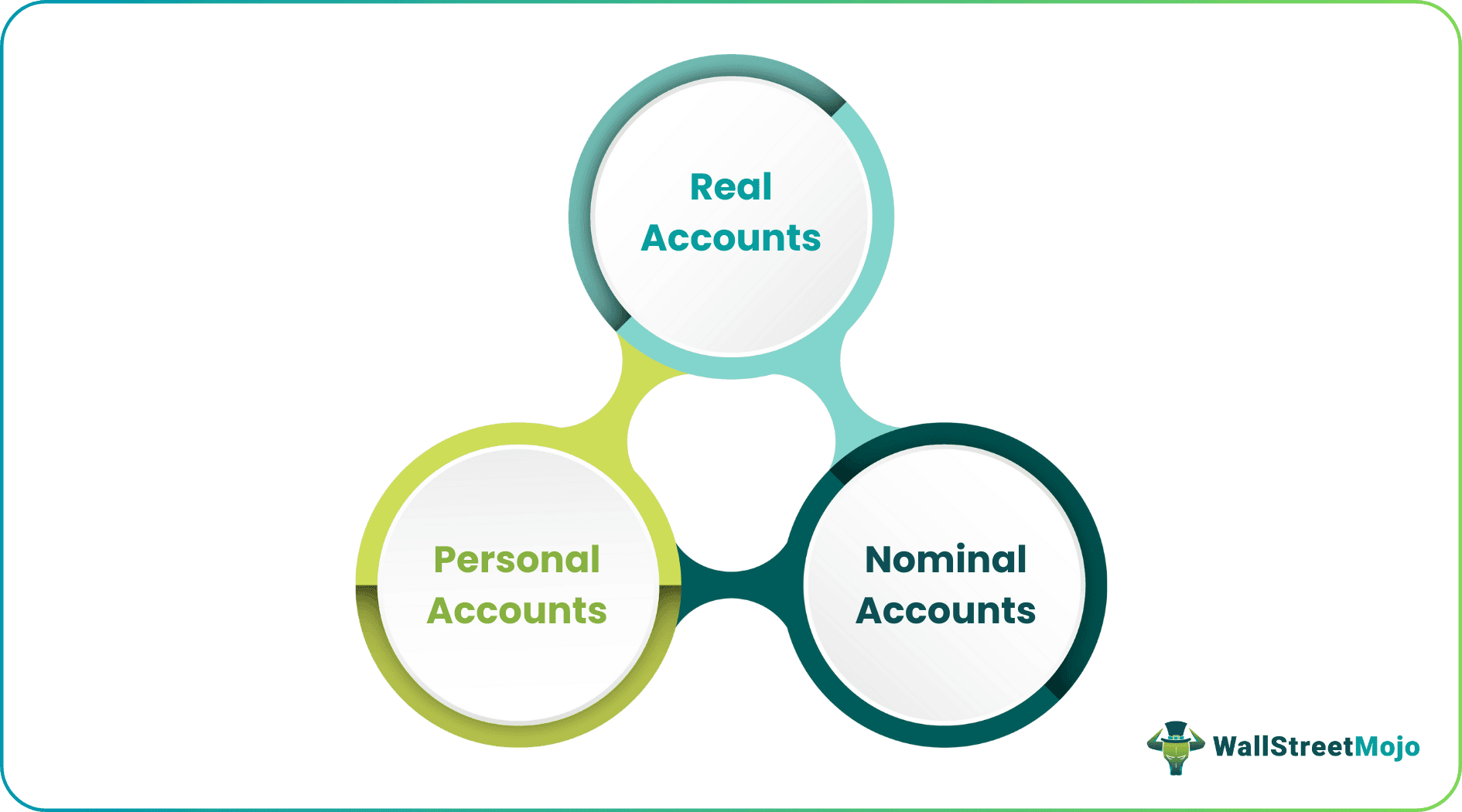

There are three different types of accounts, Real, Personal, and Nominal Accounts. Rules of recording the transactions are decided based on the type of account.

#1 – Real Accounts – Debit what comes in and Credit what goes out. Real accounts include Pant & Machinery, Buildings, Furniture, or any other Asset account. So when we purchase Machinery, the Machinery account is debited, and when we sell Machinery, the Machinery account is credited.

#2 – Personal Accounts – Debit the Receiver and Credit the Giver. The personal account includes the account of any person, such as an owner, debtor, creditor, etc. When we make payment to our creditors, the receiver account is debited, and when we receive the payment, the giver account is credited.

#3 – Nominal Accounts – Debit all Expenses and Losses and Credit all Incomes and Gains. Nominal accounts include all the Expenses, Income, Profit, and Loss accounts. For example, the Salary Paid account is debited, and the rent received account is credited.

Examples

Now that we understand the basics and features of double entry accounting, let us apply the knowledge to practical application through the examples below.

Example #1

Here are a few transactions for which Journal Entries are to be recorded. Record the entries in the Books of A Limited.

A Limited Purchases Goods worth $2,500 from B Limited on Credit.

| Particulars | Debit | Credit |

|---|---|---|

| Purchase A/c | $2,500 | |

| B Limited A/c | $2,500 |

A Limited makes a payment for the Goods next Month.

| Particulars | Debit | Credit |

|---|---|---|

| B Limited A/c | $2,500 | |

| Cash A/c | $2,500 |

A Limited Purchases Machinery worth $30,000 by paying cash:

| Particulars | Debit | Credit |

|---|---|---|

| Machinery A/c | $30,000 | |

| Cash A/c | $30,000 |

A Limited received Rent on Building $1,500:

| Particulars | Debit | Credit |

|---|---|---|

| Cash A/c | $1,500 | |

| Rent Received A/c | $1,500 |

Example #2

In 2023, a Triple Entry Accounting (TEA) conference was held in Malta where the seven papers were published and discussed. The conference brought to light auditing, Hollywood, sports, Artificial Intelligence (AI), Bitcoin, blockchain, and how all of these phenomena trail back to accounting.

A majority of accounting in all these regards is done in double-entry systems. However, the possibility of introducing a new dimension and making it a Triple Entry Accounting system was discussed in detail in the two-day conference.

Importance

The importance of double entry system lies in its role as a systematic financial management tool. Let us understand why through the discussion below.

- Double entry accounting ensures accuracy in financial records by requiring each transaction to have equal and opposite effects on the accounting equation. This inherent balancing act serves as an immediate check, making it easier to detect errors or discrepancies in the books.

- The systematic recording of transactions in double entry accounting facilitates the preparation of accurate and reliable financial statements. This, in turn, provides stakeholders, including investors and creditors, with a clear and transparent view of the company’s financial health.

- With precise financial data readily available, businesses can make informed decisions. Double entry accounting provides a comprehensive overview of assets, liabilities, and equity, enabling management to analyze financial trends, assess profitability, and plan for the future.

- Many regulatory bodies and tax authorities require businesses to maintain accurate financial records. Double entry accounting ensures compliance with these regulations, reducing the risk of legal issues and financial penalties.

- The dual recording of transactions creates a reliable audit trail, allowing for thorough examination by internal or external auditors. This transparency enhances trust among stakeholders and can contribute to the company’s credibility.

Advantages

Let us understand the advantages of double entry accounting through the points below.

- Modern and Scientific: Double entry is a scientific and systematic system of recording and maintaining books of accounts. There are the Rules and Principles which have to be followed rigorously.

- Complete System of Accounting: This form of accounting records both aspects of a transaction; hence, it is a complete form of accounting.

- Fewer Errors: There are fewer chances of errors as both the debit and credit sides of the transaction have to be equal.

- Fraud Prevention: This accounting system helps in the prevention and early detection of fraud.

- Decision Making: A complete set of books helps in decision making for management, investors, creditors, and auditors.

Disadvantages

Despite the various advantages mentioned above and throughout the article, there are a few points that prove to be a hassle for accountants and businesses alike with respect to following a double entry system. Let us discuss them through the explanation below.

- Complex: This is a more complex form of accounting. The person must know the rules of accounting to ensure the books are maintained correctly.

- High Cost: Since this system of accounting required skilled personnel hence the cost of hiring them would also be high.

- Not suitable for Small Business: Small businesses with fewer transactions would not find this method of accounting suitable for them.

Difference Between Double Entry and Single Entry

Let us understand the differences between double entry accounting and single-entry accounting through the comparative table below.

| Basis | Double Entry System | Single Entry System |

|---|---|---|

| Meaning | It is the method of accounting where the dual aspect of the transaction is recorded | It is the method of accounting where only one side of the transaction is recorded |

| Nature | It is a complex form of accounting. | It is a simple form of accounting. |

| Accuracy | It provides more accurate financial results | Since it records only one side of the transaction hence less accuracy. |

| Scale of Business | Preferable for large-scale business | Preferable for small-scale business |

| Level of Completion | It is a complete form of accounting | It provides incomplete results |

| Detection of Errors | Errors can be detected easily | Difficult to detect errors as only one side of the transaction is recorded |

| Cost | Higher cost as skilled staff is required to maintain the book of accounts | Less cost as it is a simple form of accounting |

Recommended Articles

This has been a guide to Double Entry. Here we discuss its principles examples, advantages and disadvantages, and compare it with singe entry system. You may also have a look at the following articles –