Part of our Financial Statement Analysis guide

What is Common Size Balance Sheet Analysis?

→ Explore all 93 Balance Sheet articles

Common size balance sheet refers to percentage analysis of balance sheet items based on the common figure as each item is presented as the percentage which is easy to compare, like each asset is shown as a percentage of total assets and each liability is shown as a percentage of total liabilities and stakeholder equity as a percentage of total stakeholder’s equity.

Building a common size statement balance sheet is convenient because it helps build trend lines to discover the patterns over a specific period. In short, it is not just an upgraded variety of the balance sheet per se. Still, it also captures each single line item as a percentage of total assets, total liabilities, and total equity besides the usual numeric value.

- The common size balance sheet analyzes a balance sheet that presents each item as a percentage of a standard figure.

- Assets are expressed as a percentage of total assets, liabilities as a percentage of total liabilities, and shareholder equity as a percentage of total shareholder equity.

- This approach allows for easy year-on-year performance comparison of the same company or comparison of different companies of varying sizes.

- By expressing each item as a percentage of the standard figure, the common size balance sheet enables analysts to compare companies of different sizes and make meaningful comparisons.

Examples of Common Size Balance Sheet Analysis

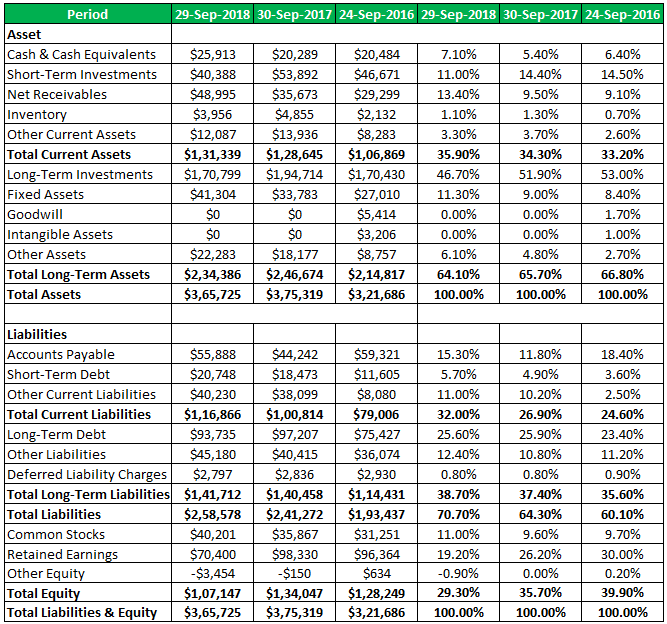

Let us take the example of Apple Inc. to see the trend in the financials of the last three years.

All amount in Millions

For instance, it can be seen that there is a relative decrease in the long-term investments from 2016 to 2018, while the current liabilities have witnessed an uptrend during the same period. An analyst can further deep dive to determine the reason behind the same to make a more meaningful insight.

Detail screenshot of the excel template with formula

Explanation of Common Size Balance Sheet in Video

Common Size of Colgate’s Balance Sheet

- Cash and Cash equivalents as a percentage of total assets increased substantially from 5.6% in 2008 to 8.1% in 2014.

- Receivables percentage decreased from 16.6% in 2007 to 11.9% in 2015.

- Inventories percentage decreased from 11.6% to 9.9% overall.

- Other current assets percentage increased from 3.3% to 6.7% of the total assets over the last 9 years.

- On the liabilities side, Accounts payable currently stands at 9.3% of the total assets.

- There has been a significant jump in the Long Term Debt to 52,4% in 2015.

- Non controlling interests has also increased over 9 years and is now at 2.1%

Advantages

- It aids the reader of the statement to clearly understand the ratio or percentage of each item in the statement as a percentage of the company’s total assets.

- It aids a user in determining the trend related to the percentage share of each item on the asset side and the percentage share of each item on the liability side.

- A financial user can also use it to compare the financial performances of different entities at a glance since each item is expressed in terms of percentage of total assets, and the user can determine any required ratio quite easily.

Disadvantages

- A common size balance sheet is regarded as impractical since there is no approved standard proportion of each item to the total asset.

- In case the balance sheet of any particular company is not prepared year after year consistently. It will be misleading to perform any comparative study of the common size statement balance sheet.

Limitations of Common Size Balance Sheet Analysis

- It does not aid in making decisions because there isn’t any approved standard proportion regarding the composition of assets, liabilities, etc.

- If there is inconsistency in preparing the financial statements due to changes in accounting principles, concepts, conventions, then a common size balance sheet becomes meaningless.

- It does not convey proper records during seasonal fluctuations in various components of assets, liabilities, etc. Therefore, it fails to provide the essential information to the financial users of the statements.

- One can’t ignore the ill effects of window dressing in financial statements. Sadly, a standard-size balance sheet fails to identify the same to provide the real positions of assets, liabilities, etc.

- It fails to identify the qualitative elements while gauging a company’s performance, although it is not a good practice to ignore the same. Examples of qualitative elements may include customer relations, quality of work, etc.

- They can’t measure the solvency and liquidity position of a company. It merely measures the percentage increase or decrease in various components of assets, liabilities, etc. In other words, a common size balance can’t be used to determine the debt-equity ratio, capital ratio, current ratio, liquidity ratio, capital gearing ratio, etc. which are usually applied in ascertaining the solvency and liquidity position of a company.

Conclusion

In conclusion, it can be said that a common size balance sheet facilitates easy comparison of the year-on-year performance of the same company or comparison of different companies of varied sizes. It also enables an analyst to compare companies of varied sizes irrespective of their size difference, which is in-built in the raw data. To elaborate, not only can a user effortlessly see how well a company’s capital structure is allocated, but they can also compare those percentages to other periods in time or to other companies.

Frequently Asked Questions (FAQs)

1. How a common-size balance sheet helps financial managers?

A common-size balance sheet helps financial managers by providing a more detailed analysis of a company’s financial position. Expressing each item on the balance sheet as a percentage of total assets allows for easy comparison of different categories and helps identify trends over time. This information can be useful in making investment decisions, identifying areas of financial strength and weakness, and developing strategies to improve financial performance.

2. What is a vertical common-size balance sheet?

A vertical common-size balance sheet is a financial statement that expresses each item as a percentage of total assets. Doing so highlights the relative importance of each item on the balance sheet and allows for easy comparison of different categories. This can help financial managers identify trends and make informed decisions about the company’s financial position.

3. What is a horizontal common-size balance sheet?

A horizontal common-size balance sheet is a financial statement that compares the percentage change of each item from one period to another. It helps identify the relative importance of different balance sheet items and highlights changes in the company’s financial position over time.

Recommended Articles

This article has been a guide to Common Size Balance Sheet Analysis. Here we discuss Common Size Balance Sheet Format and examples of Apple and Colgate. You may learn more about from the following articles –