Part of our Accounts Payable & Receivable guide

What is Cash Book?

Cash Book is the one in which all the cash receipts and cash payments, including the funds deposited in the bank and funds withdrawn from the bank, are recorded according to the date of the transaction. All the transactions recorded in the cash book have two sides, i.e., debit and credit.

The difference between the sum of balances of the debit and credit sides shows the cash balance on hand or bank account. Cashbook plays a dual role as it is the book of the original entry of the company and the book of the final entry.

Cash Book Explained

The cash book is a separate book of accounts in which all the company’s cash transactions are entered concerning the corresponding date, and it is different from the cash account where posting is done from the journal. There is no requirement to transfer the balances to the general ledger, which is required in the case of the cash account. Entries are then posted to the corresponding general ledger.

cash book accounting has two sides, i.e., the left-hand side and the right-hand side, where all the receipts in cash are recorded on the left side, whereas all the payments in cash are recorded on the right side. Therefore, cash book helps in effective cash management as management can know the balances of cash and bank and take the necessary decisions accordingly.

Types

Among the different types of maintaining a petty cash book or a full-fledged one, the three types are as discussed below.

#1 – Single Column

Single column cash-book contains only the cash transactions done by the business. Single column cash book has only a single money column on debit and credits on both sides. It does not record the transaction-related, which involves banks or discounts. The transactions done on credit are not recorded while preparing the single-column cash–book.

#2 – Double Column

The double-column cash book contains two money columns both on the debit and the credit sides. One column is for the transactions related to the cash, and the other column is for the transactions related to the business’s bank account. So, under the double-column cash book, the business also records cash transactions and transactions through the bank. But on the other hand, the transactions on credit are not recorded while preparing the double column cash–book.

#3 – Triple Column

It is also referred to as a three-column cash book format, and it is a complete form with three columns of money on both receipt and payment sides and records transactions about the cash, bank, and discounts. This book is generally maintained by the large firms that do transactions in cash mode and through the bank and frequently allow and receive cash discounts.

Format

Let us understand the format of maintaining a petty cash book or a detailed cash book through the detailed explanation below.

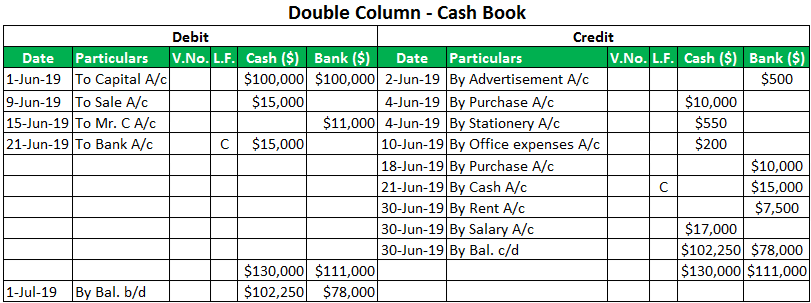

Mr. X started the business in the month of June-2019. X invested a capital of $200,000, in which the cash contribution is $100,000, and the rest of the $100,000 he deposited in the business bank account of a business. On June 19, the following transactions took place in the business. Prepare the necessary double-column Cash Book using the data given below:

| Date | Transactions |

|---|---|

| 1-Jun | Initial capital contribution. Cash : $100,000 an Bank $100,000 |

| 2-Jun | Paid for Advertisement $ 500 from check |

| 4-Jun | Raw material purchased from Mr. A of $ 10,000 by paying cash |

| 4-Jun | Purchased stationery for cash worth $ 550 |

| 7-Jun | Raw material purchased from Mr. B of $ 20,000 on credit |

| 9-Jun | Goods sold to the customer for $15,000 by cash |

| 10-Jun | Paid $ 200 for the office expenses in cash |

| 13-Jun | Goods sold on credit worth $ 11,000 to Mr. C |

| 15-Jun | Received a check worth $ 11,000 for the goods sold on credit on 13-July-2019 to Mr. C; |

| 18-Jul | Raw material purchased $ 10,000 by paying through check |

| 21-Jun | Withdrew from bank $ 15,000 for business |

| 25-Jun | Goods sold on credit worth $ 5,000 |

| 30-Jun | Paid rent by check of $ 7,500 |

| 30-Jun | Paid the salaries to staff of $ 17,000 in cash |

Solution:

Importance

Despite being difficult to maintain on a large scale, organizations ensure maintaining cash book accounting for a handful of reasons. Few of which are as discussed below.

- Cash-book plays a dual role as it is the book of the company’s original entry and the final entry.

- It has two the identical sides, i.e., the left-hand side (debit side) and the right-hand side (credit side)

- The difference between the total of the two sides gives cash in hand or bank account balance.

- The transactions which are done on credit are not recorded in this book.

Advantages & Disadvantages

Let us understand the advantages and disadvantages of cash book accounting through the points below.

Advantages

- It helps save time and labor, as in the case of recording cash transactions in the journal, tremendous time and labor are required, whereas, in the case of a cashbook, cash transactions are recorded straight away in the form of the ledger.

- Management can know the balances of cash and bank at any time. It helps in effective cash management.

- Cashbook is balanced regularly, which helps in avoiding fraud. Also, discrepancies, if any, arise and can be found and rectified.

Disadvantages

- It may take a lot of time to start and maintain this book.

- In the case of a large organization, maintaining it involves high costs

Recommended Articles

For more on Accounts Payable & Receivable, explore these related articles from our Accounts Payable & Receivable guide.