Part of our Accounts Payable & Receivable guide

What Is Petty Cash Book?

A petty cash book is an accounting book used to record petty cash expenditures, i.e., small amounts that a company occurs in its day-to-day operations. The date-wise arrangement of records makes it simple to maintain, manage and retrieve data when the date is known.

Calling it a formal summarization of expenditures involving petty cash expresses the petty cash book meaning better. These expenses are the regular day-to-day expenses of a business that are not related to the company’s direct line of business. Therefore, it is an accounting book for recording small expenses with little value.

- Petty cash books maintain day-to-day transactions that a company incurs, such as refreshments, water, etc.

- Accounting’s core lies in the journal, ledger, and petty cash book. Most transactions in the petty cash book are recorded in the cash account.

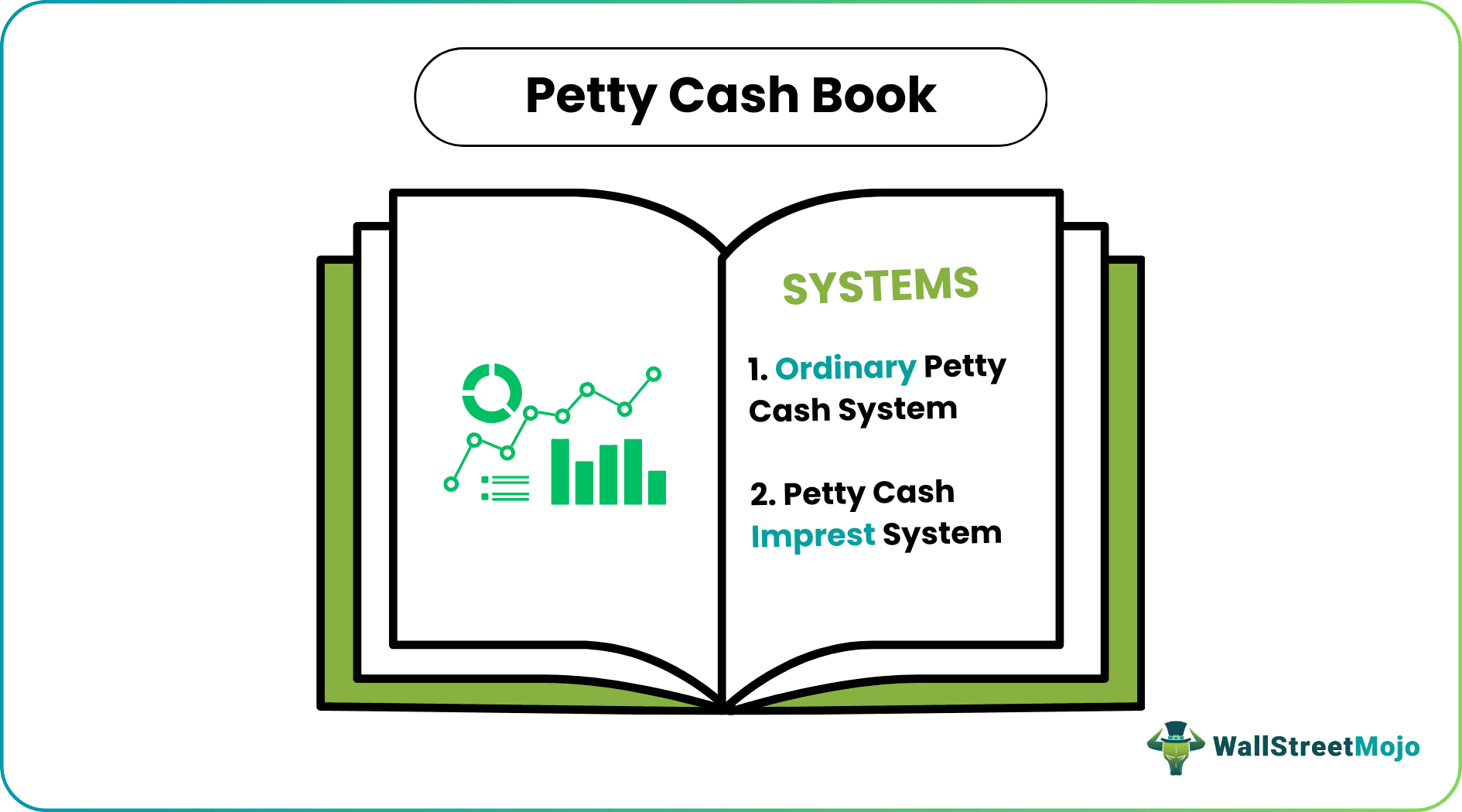

- There are two systems to record expenses in the petty cash book, the ordinary petty cash system and the petty cash system. Both are widely taught and used.

- Under the ordinary system, a bigger cash amount is given to the petty cashier. In the system, the petty cashier amount is fixed for a given period, usually a month or a week.

How Does Petty Cash Book Work?

A petty cash book is a manual system recording expenditure and is often prone to errors. It also becomes cumbersome to keep the books and record each transaction, especially in big companies. However, many companies are scrapping the old bookkeeping system to overcome this. Instead, they are now moving to modern bookkeeping methods like corporate credit cards or tally software, which are highly efficient systems for recording nominal and considerable business transactions.

The basis of accounting lies in the three main accounting terms and accounts: journal, ledger, and the petty cash book. Each transaction in the books of accounts goes through these three accounts to get captured.

Journal is an integral part of bookkeeping, the starting point of accounting, and it records all the business transactions. From the initiation of the journal, the ledger account is prepared, with the help of which the final books of accounts of the company are prepared. In contrast, the petty cash book records the transactions related to the cash account.

However, several transactions during the ordinary course of the business are of negligible amounts and are not recorded in the cash book account. For transactions of such nature, the petty cash book is used.

Though the petty cash book account has lost its importance over time, it is still used as a handy tool to record companies where modern technology has not been introduced.

Types

The cash is given to the petty cashier on the following petty cash system basis:–

#1 – Ordinary Petty Cash System

Under this system, a lump sum amount of cash is given to the petty cashier. The cashier is responsible for keeping a record of all the expenses for the review of the head cashier. They must present it before requesting new funds to run the day-to-day expenditure again.

#2 – Petty Cash Imprest System

The companies have widely adopted Imprest Petty Cash System to run their petty cash account. Under the petty cash Imprest System, the petty cashier amount is fixed for a given period, usually a month or a week. Under this period, the cashier must run the petty cash account under the given budget. At the end of the period, the cashier submits the report, and the amount spent by him is reimbursed so that the amount becomes equal to the beginning balance at the starting of the previous month. If the expenditure exceeds the amount, a special request stating the requirement needs to be raised to the head cashier to replenish the funds for a given time.

Petty Cash Video Explanation

Example

Below is the sample format of the petty cash book:

| Date | Voucher No. | Particulars | Quantity | Purchase Amount | Balance |

| 31/03/2018 | Opening Balance | 1 | 250 | ||

| 4/5/2018 | 123343 | Kitchen Supplies | 1 | -50 | 200 |

| 4/8/2018 | 123344 | Birthday Cake | 1 | -24.15 | 173.05 |

| 4/11/2018 | 123345 | Pizza Lunch | 1 | -81.62 | 91.43 |

| 4/14/2018 | 123346 | Taxi Fare | 1 | -25 | 66.43 |

| 4/24/2018 | 123347 | Newspaper | 1 | -10 | 56.43 |

The person responsible for recording the receipts and the payments is known as the petty cashier. The company’s administrative department usually maintains the petty cash book as the accounts departments generally take care of more significant business transactions. Additionally, the admin department is also responsible for such kinds of expenses.

Advantages

The benefits of using this system of recording finances are as follows:

- It is quite simple to maintain and manage. Here, the actual cash requirement is realized effectively. For example, if $1,000 is only spent a month on such expenses, the initial amount floated to the responsible party can be immediately increased or decreased after analyzing the period and the occurrence of expenses.

- The head cashier periodically reviews it, therebyminimizing the probability of any error during bookkeeping. .

- It has been a tried and tested, efficient and less time-consuming method. This system of bookkeeping helps in recording little and frequent expenses.

- This method enhances cost savings. The amount incurred in petty cash expenses is analyzed carefully and checked periodically to realize how much cash is required and where the company can cut down on unnecessary expenses in the petty items.

- The imprest petty cash system allows staff members to handle cash effectively to prove their worth to their seniors and be seen as future cash managers.

Disadvantages

The flaws of the method include the following:

- The frequent transaction recording makes the bookkeeping lengthy. As a result, retrieving records becomes time-consuming. The overall structure makes tracking and tracing records difficult.

- The system needs thorough review periodically. In fact, arranging records from time to time and reconciling things over and over again makes bookkeepers put extra efforts, making it an unnecessary engagement for them.

Frequently Asked Questions (FAQS)

What is the difference between cash book and petty cash book?

The difference between a petty cash book and a cash book is that a petty cash book is used to record small and repeated transactions, whereas a cash book is used to record transactions of larger sums.

What is the petty cash book formula?

The balance of the on-hand petty cash is calculated as the difference between the total of the debit and credit items. The book where little payments are made that are inconvenient to record in the main cash book is known as a petty cash book.

What guidelines apply to petty cash?

Petty-cash accounts must be kept in installments. To ensure that the available cash and the authorized petty cash vouchers add up, the custodian(s) should balance the fund daily. Petty cash withdrawals are restricted to $50 or less per person each month.

Recommended Articles

This article has been a guide to what is Petty Cash Book. Here we explain the format through an example along with its types, advantages, and disadvantages. You may learn more about accounting basics from the following articles –