Part of our Accounts Payable & Receivable guide

Petty Cash Meaning

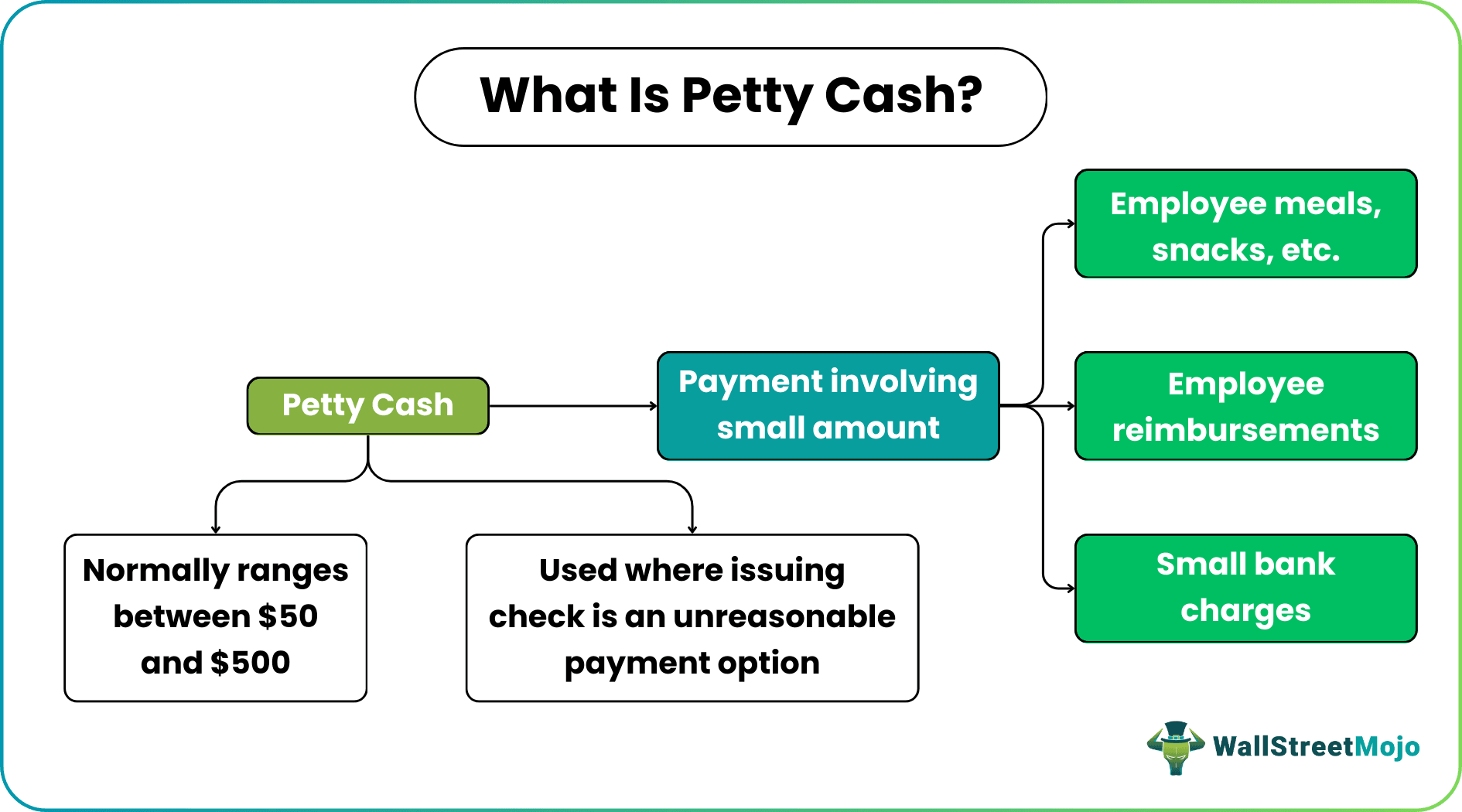

Petty cash refers to the amount used to pay for small expenses of a company issuing a check for which seems unreasonable. Payment by check involves a long encashing procedure found unnecessary to go through when the small payments could easily be settled in cash.

Petty cash is an integral part of the accounting function in most organizations and is well taken care of by an appointed custodian. A petty amount a company can spend on the daily expenditures varies between $50-$500.

- Petty cash is the small amount used to pay for expenses for which issuing a check might not be a sensible option.

- The time taken to encash a check makes companies prefer paying in cash for small expenses on the spot.

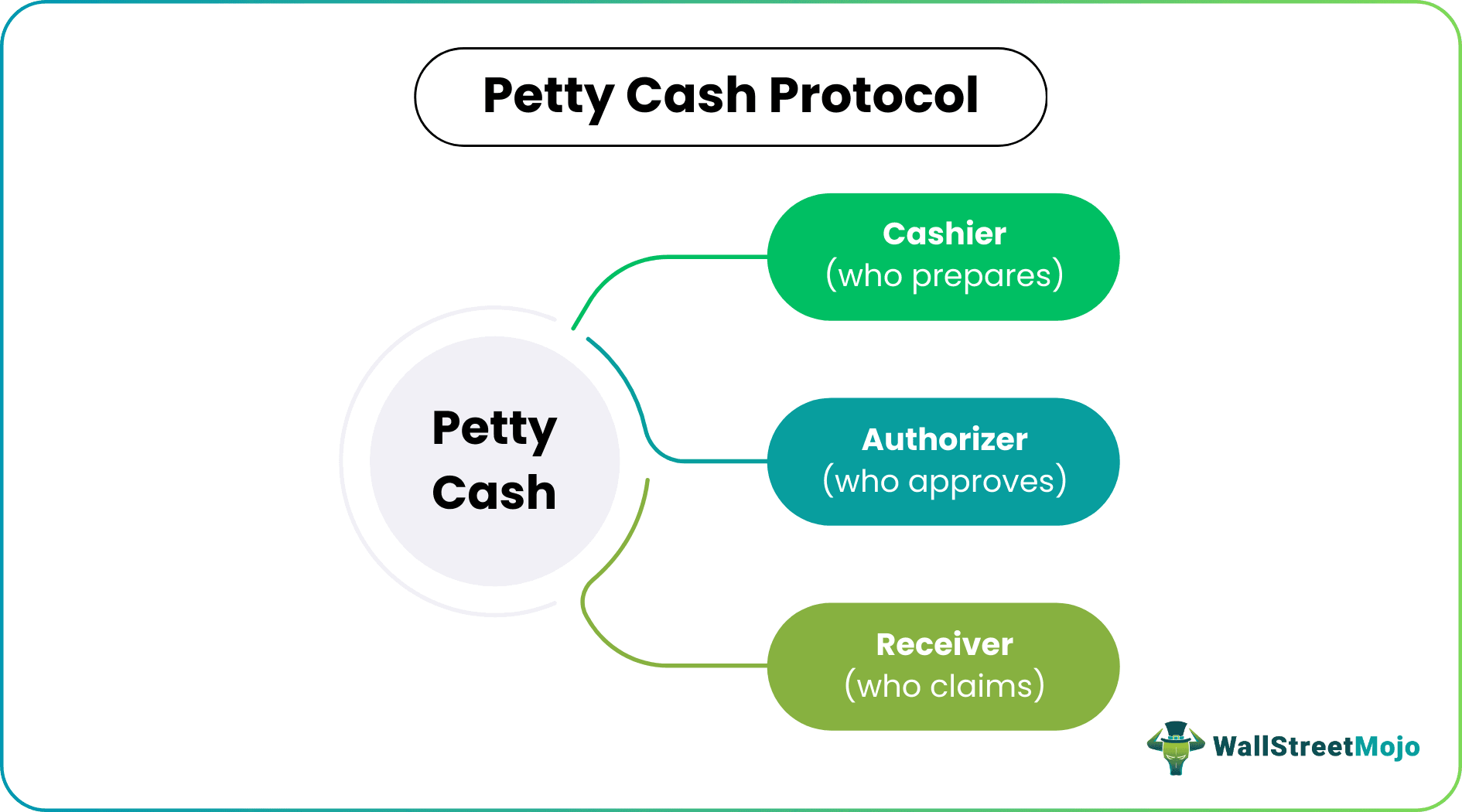

- There is a Cashier (who prepares), an Authorizer (who approves and authorizes the fund), and a Receiver (who claims) for proper petty fund transaction implementation.

- When such a petty amount is utilized to settle expenses, it needs to be replenished.

How Petty Cash Works?

Petty cash is the cash amount used to settle small expenditures that companies make from time to time. As the cost of writing, signing, and processing the checks take a lot of time, companies prefer paying in cash on the spot for a smaller amount. In addition, the companies appoint custodians who are responsible and accountable for making sure these cash entries are accurately completed and reconciled at regular intervals.

Companies keep the small amount of cash in the office under the control of a cashier, who keeps a check on each cash transaction for correct entries and appropriate recordkeeping. Expenditures such as day-to-day snacks, tea for employees, employee reimbursements for occasional traveling, etc., small bank charges, like notary, etc., greetings or sweets to clients or customers on festivals or special occasions – are all paid through a petty fund.

In an organization, there is three personnel to take care of the whole petty money transaction flow:

- Cashier – who prepares the petty cash voucher and receipt

- Authorizer – approver, who belongs to the higher management

- Receiver – the claimant

The frequency at which petty cash is withdrawn differs hugely from organization to organization. For example, a small shopkeeper needs to have more cash readily available than a big organization, mostly settling payments through checks.

Petty Cash Accounting

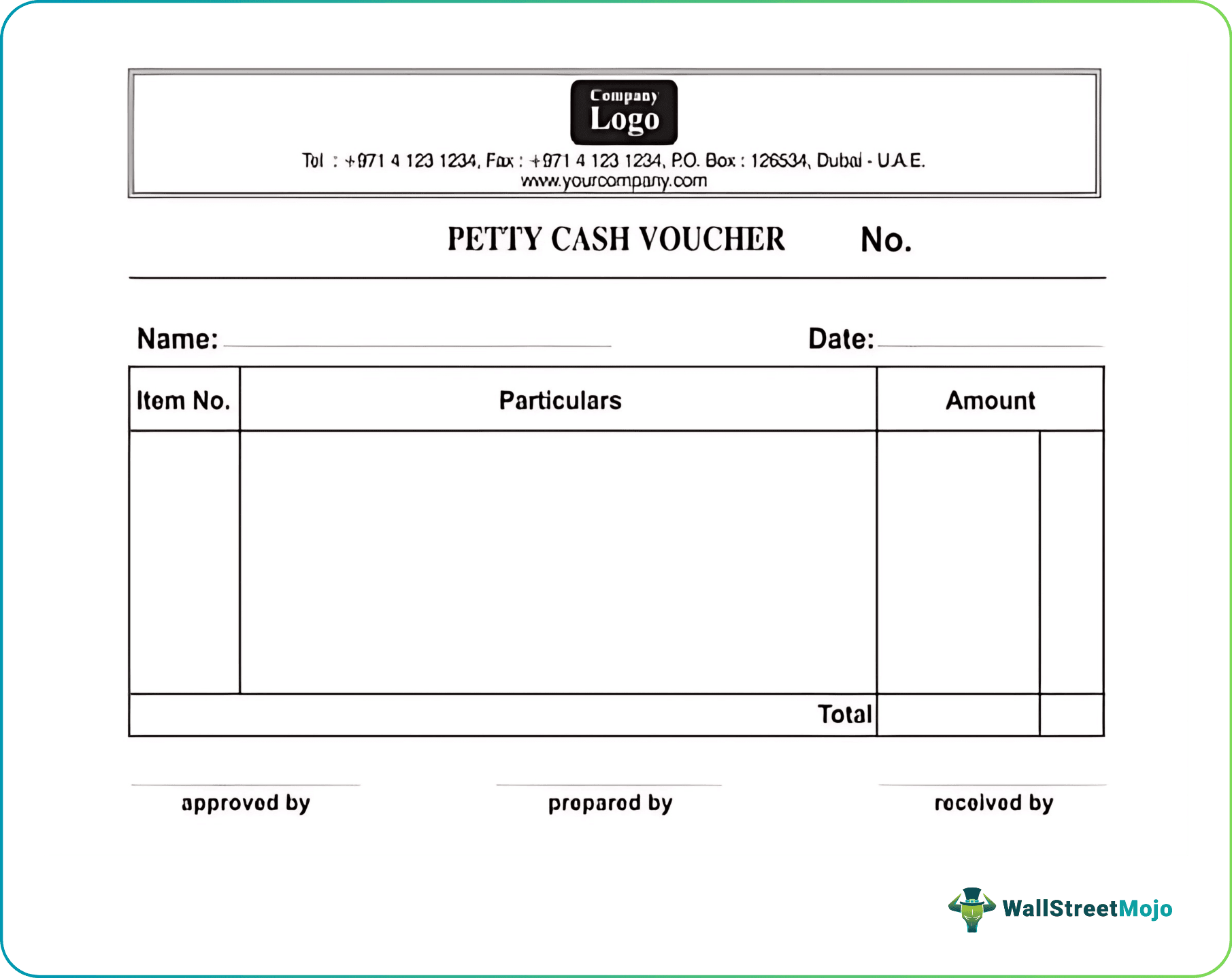

An organization, as per its estimate, gets approved the cash required for a specific range of time, be it weekly or monthly. Then, the amount is withdrawn from the bank to settle cash expenses based on the approved limit. Finally, the amount withdrawn in the form of paper money or coins gets deposited with the custodian, who issues receipts and a petty cash voucher for the required cash.

A petty cash transaction is recorded on financial statements even when it is already in use. The expenditures or purchases made using these cash amounts are not part of the journal entries. The journal entry, however, is only made when the custodian needs more cash than what has been approved by the company. The journal entries are made when the custodian receives new funds in exchange for the receipts.

When a small amount is utilized to settle expenses, it needs to be replenished. Therefore, the custodian gathers all slips and vouchers issued to different individuals in the organization. The details are recorded in General Ledger as credits to the petty cash account, while the same is kept as a debit detail to multiple other expense accounts. As soon as the petty fund is replenished, it is recorded as a debit to the petty cash account and credit to the cash account.

When petty cash fund is replenished by check, it is represented as follows:

| Particulars | Debit | Credit |

|---|---|---|

| Petty Cash A/c Dr. | XXXX | |

| To Bank A/c | XXXX |

Petty Cash Explained in Video

Reconciliation

Petty cash reconciliation is required to be done at regular intervals to make sure the fund balance is correct. The custodian has to get the total of all the receipts to make sure that the resulting figure matches the amount taken out from the office drawer. In case a new fund is required, cashiers can write a new check.

If there is a shortage of funds or over the required limit, a journal line entry is recorded into a short/over an account. If the fund is over, it is a credit entry, which indicates gain. On the other hand, it is a debit entry as a loss if the petty cash fund is short. In such a scenario, reconciliation is observed to balance the funds forcefully.

Example

Let’s take a look at the following petty cash example to understand how it is used in accounting:

Company A has a petty cash fund for which it approved $100. The entry made is as below:

| Particulars | Debit | Credit |

|---|---|---|

| Petty cash | $100 | |

| Cash | $100 |

The custodian lets the cash balance decline to $10 before replenishing. Thus, the cashier issues a check worth $90 for replenishment. Accordingly, the entry looks like this:

| Particulars | Debit | Credit |

|---|---|---|

| Petty cash | $90 | |

| Cash | $90 |

The expenses as recorded by the cashier along with the amount used for replenishment are entered as:

| Particulars | Debit | Credit |

|---|---|---|

| Office expenses | $90 | |

| Petty cash | $90 |

The petty fund amount, therefore, is now back to the authorized amount worth $100.

Frequently Asked Questions (FAQs)

What is petty cash?

Petty cash, as the name suggests, is a small amount stored in office boxes or drawers to be used to pay for small expenses, including employee meals and snacks. It is the best mode of payment in situations in which paying by check seems an insensible option. Normally, such an amount that a company can spend on the daily expenditures varies between $50 and $500.

A custodian takes care of the transactions done in petty paper money.

Is petty cash an asset or expense?

In financial accounting, the petty cash account is a current asset. Therefore, the funds are entered as a normal debit balance.

Is petty cash equivalent to cash on hand?

Though the petty fund is available in cash and can be considered cash on hand, the cash on hand is not always petty cash. Thus, we can say it is not equivalent to cash on hand.

Recommended Articles

This article has been a guide to petty cash and its meaning. Here we discuss how does petty cash works along with its format, Accounting, and examples. You may learn more about financing from the following articles –