Part of our Banking Ratios & Metrics guide

What Are Leverage Ratios for Banks?

→ Explore all 23 Leverage Ratios articles

Leverage ratio for banks indicates its financial position regarding its debt and capital or assets. One may calculate it by Tier 1 Capital divided by consolidated assets, where Tier 1 Capital includes common equity, reserves, retained earnings, and other securities after subtracting goodwill. Minimum leverage ratios for banks help them to have enough liquidity in hand to pass certain stress tests.

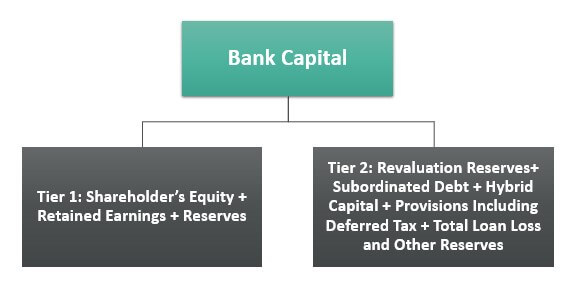

In simple words, this is a metric used to evaluate the level of debts possessed by the company and assess its capability to repay its financial obligations. This ratio assumes additional significance for a bank as a bank is a highly levered entity. A bank’s capital signifies its net worth (assets – liabilities) and is majorly split between two categories: Tier 1 and 2.

- A bank’s leverage ratio displays the economic position concerning the debt and capital or assets.

- To calculate, one must divide Tier 1 Capital by consolidated assets. Tier 1 Capital involves common equity, reserves, retained earnings, and other securities after deducting goodwill.

- A careful ratios investigation shows the debt-paying bank’s capability and funds management. It also identifies its profits.

- It also helps to determine whether the banks can withstand a financial crisis which one would only understand the actual effect once it strikes.

Leverage Ratios For Banks Explained

Leverage rations for banks is a clear indicator of the financial health of a bank. It is the capital in the bank its assets. Ideal leverage ratios for banks increase the creditworthiness of a bank significantly.

Tier 1 Capital is its core capital and includes items you will traditionally see on a bank’s balance sheet. The Tier 2 Capital is a supplementary type and mostly includes all the other forms of a bank’s capital, including undisclosed reserves, revaluation reserves, hybrid instruments, and subordinated term debt. A bank’s total capital is the sum of Tier 1 and Tier 2 Capital.

Hence, the Tier 1 Capital is naturally more indicative of whether a bank can sustain bankruptcy pressure and is the majorly used item to calculate the leverage ratios.

Leverage ratios are a powerful medium to gauge the effectiveness of a bank, whose entire business depends on the lending of funds and paying off the interest on deposits. A careful investigation of these ratios will reveal not just the debt-paying capacity of the bank but also how a bank manages its funds and recognizes profits.

Leverage Ratio Explained in Video

Top 3 Ratios

These ratios have been curated keeping in mind that banks lend out money that has been borrowed from their depositors and other institutional creditors as well. Therefore, there has to be a threshold on the ratio or portion of the such borrowed sum being borrowed.

Let us understand the top three types of minimum leverage ratios for banks that indicate the creditworthiness, liquidity, financial health and other such important metric to customers, investors, and regulators through the detailed discussion below.

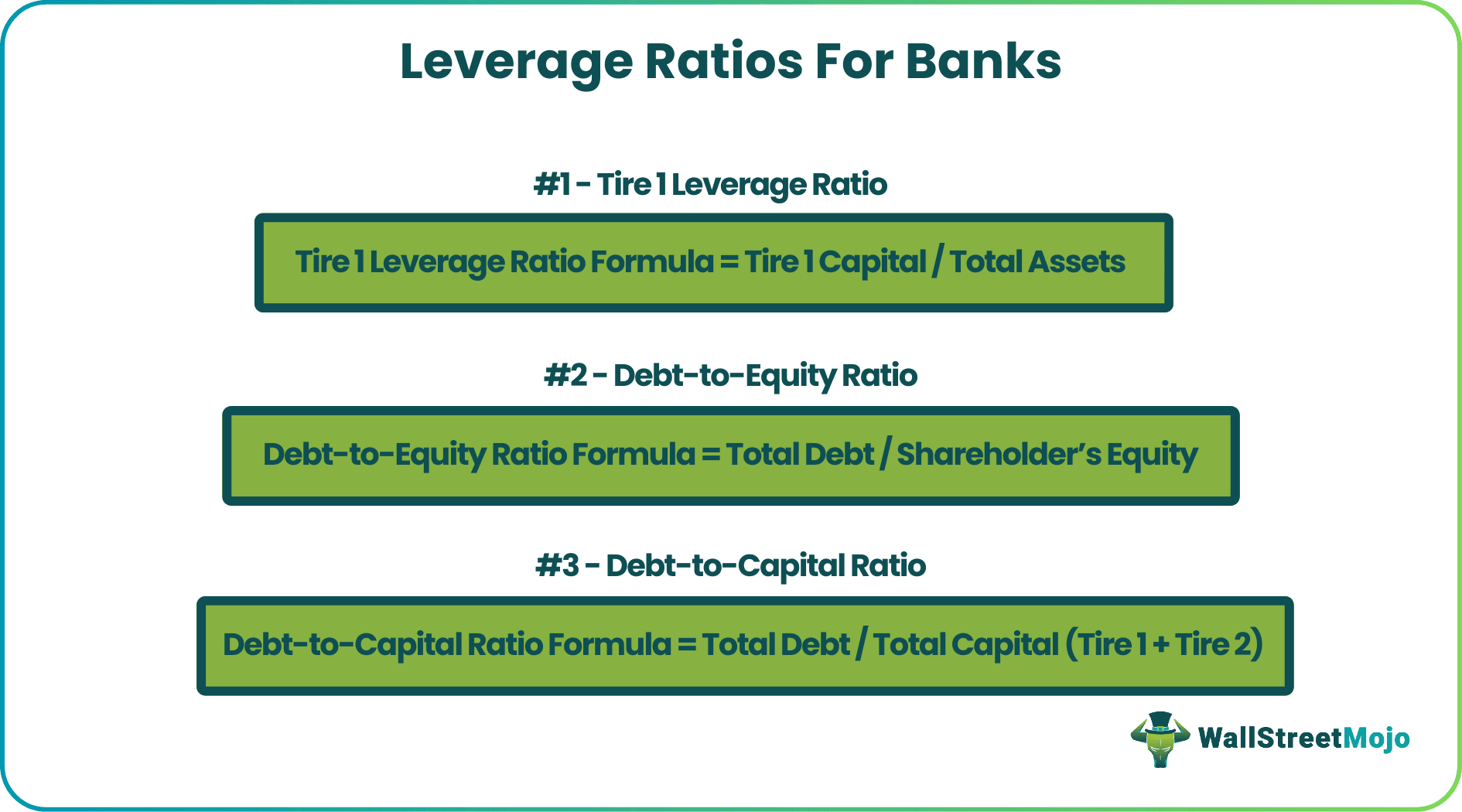

#1 – Tier 1 Leverage Ratio

Tier 1 Leverage Ratio Formula = Tier 1 Capital / Total Assets

This ratio measures the amount of core capital a bank has about its total assets. It was introduced to check a bank’s leverage and reinforce the risk-based requirements through a back-stop safeguard measure.

If a bank lends $10 for every $1 of capital reserves, it will have a capital leverage ratio of 1/10 = 10%.

According to the Basel III standards, this ratio must be at least 3%, though country-wise regulations may vary.

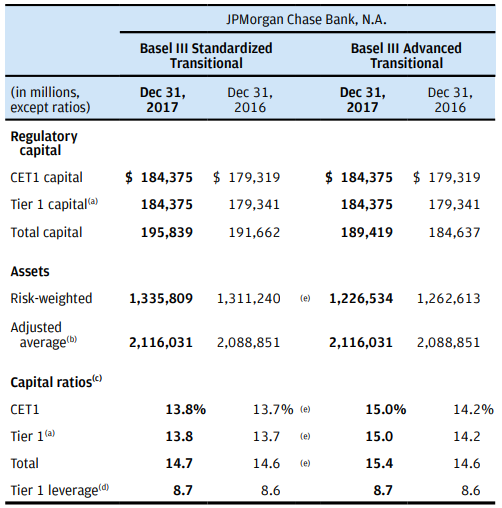

For example, in Dec 2017, JP Morgan reported a Tier 1 capital of $184,375 million and an asset exposure of $2,116,031 million, resulting in its Tier 1 leverage ratio of 8.7%, well above the minimum requirement.

Source: JPMorgan.com

This measurement metric was introduced in the aftermath of the global financial crisis in 2008 and served as the most important ratio for assessing a bank’s health.

Other commonly used leverage ratios are:-

#2 – Debt-to-Equity Ratio

Debt-to-Equity Ratio Formula = Total Debt / Shareholder’s Equity

This ratio measures a company’s amount of financing from debt versus equity. A debt-to-equity ratio of 0.4 means that for every $1 raised in equity, the company raises $0.4 in debt. Although a very high D/E ratio is generally undesirable. Banks tend to have a high debt-to-equity because they carry huge amounts of debt on their balance sheet. In addition, they have a significant investment in fixed assets in the form of a branch network.

#3 – Debt-to-Capital Ratio

Debt-to-Capital Ratio Formula = Total Debt / Total Capital (Tier 1 + Tier 2)

Like the debt-to-equity ratio, the debt-to-capital ratio indicates the amount of debt possessed by a bank concerning its total capital. Again, this is usually higher for a bank because of its operations, creating higher exposure to loans. For example, a bank with a debt of $1,000 million and equity of $2,000 million will have a debt-to-capital ratio of 0.33x but a debt-to-equity ratio of 0.5x.

Interpretation

Since we understand the ideal leverage ratios for banks in detail now, it is also equally important to understand how to interpret the data that is generated through the calculations. As in, one must be able to determine if a particular ratio shows healthy signs for the bank or otherwise. Let us do so through the discussion below.

- A higher leverage ratio is generally safer for a bank as it shows that the bank has higher capital than its assets (majorly loans). It is particularly useful when the economy falters, and the loans are not paid off. That is because banks have relatively fewer creditors than debtors, which makes it difficult to write off the loans, and hence at such times, a high equity capital pays off well.

- A high leverage ratio means the banks have more capital reserves and are better positioned to withstand a financial crisis. However, it also means less money to loan out, reducing the bank’s profit.

- The Tier 1 leverage ratio is a direct outcome of the crisis, and so far, it has worked well amidst all the amendments. However, investors still rely on banks to calculate this number, which may feed an inaccurate picture.

- Additionally, we would not know the true effect until the next financial crisis, which helps determine whether the banks can withstand a financial crisis.

Frequently Asked Questions (FAQs)

What is the operating leverage ratio for banks?

The operating leverage ratio for banks is the comparison of revenue growth with non-interest expense growth. Moreover, a positive balance displays that revenue is increasing more rapidly than expenses. Conversely, the bank accumulates costs faster than revenue if the operating leverage ratio is negative

What is a good leverage ratio for a bank?

During leveraging, lenders or banks may utilize this ratio to understand whether the company can pay its dues in due course. Typically, 1.5 to 2 is considered an ideal ratio.

How to calculate the leverage ratio for banks?

For the bank’s leverage ratio calculation, one must divide the bank’s Tier 1 capital by total consolidated assets to reach the Tier 1 leverage ratio. Next, multiply the result by 100 to convert the number to a percentage.

What is the average leverage ratio for banks?

Usually, the average leverage ratio for banks is 1.5 to 2. Therefore, it is regarded as an ideal ratio.

Recommended Articles

This article is a guide to Leverage Ratios for Banks. We discuss what leverage ratios and 3 major leverage ratios for banks are. Here are the other articles on financial analysis that you may like: –