Part of our Banking Ratios & Metrics guide

What is the Full Form of NPA?

The full form of NPA is Non-Performing Assets. It is a classified asset used for differentiating loans and advances on which principal and/or interest is overdue, i.e., payments are in default/ arrears and generally per set standards by regulatory authorities. The assets are considered NPA, where no recovery has been done within the last 90 days.

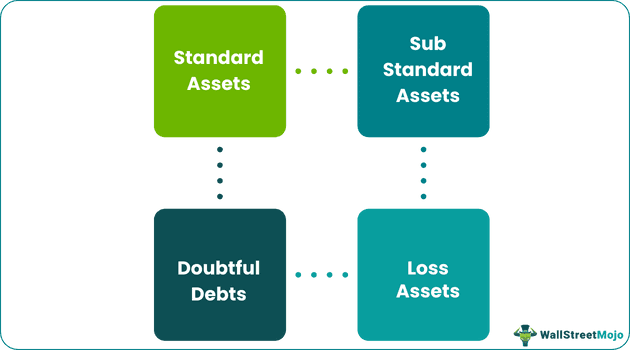

Types

#1 – Standard Assets

These are NPA, which remained overdue for more than 90 days but less than 12 months. These assets bear the nominal risk as the borrower fails to make payments regularly or on time.

#2 – Sub Standard Assets

These are NPA, which are overdue for more than 12 months, these loans have more risk, and the borrow has weak creditworthiness. So, banks create a haircut to such NPA as there is a risk of non-payment.

#3 – Doubtful Debts

These are Non Performing Assets, overdue for more than 18 months, banks having a danger of recovery, and are known as doubtful debts. Such NPA affects bank creditworthiness as more of them could put the bank at risk.

#4 – Loss Assets

It is the last classification of NPA as under these, the loan amount is classified as non-recoverable by the bank itself. Therefore, the bank can either write off the outstanding amount or make provision for the full amount, which will be written off in the future.

How NPA Works?

NPA are normal loans and advances, but non-recovery, usually 90 days, is categorized as NPA after a prolonged time. After the specified period and giving prior notice to the borrower, the lender has the right to force the borrower to sell the asset pledged against the loan and realize proceedings for recovery. Still, if no asset is pledged, the lender has to write off/advance as bad debts and will align it with the collection agency at a discounted rate. A loan can be classified as NPA at any point during the tenure of the loan. As a result, it is placed on the financial institutions, balance sheet, negatively impacting their image.

Example

Justin Inc. borrowed $100 million from a loan company and paid $200,000 monthly. But due to some reasons, the company couldn’t pay the installments for three consecutive months. As a result, the lending company will be forced to classify this loan as a non-performing asset to meet the legal requirements.

Impact

The problem of NPA is alarming nowadays in our banking system. The most important is the NPA. The least is the confidence of depositors, lenders, or investors. It makes credit availability difficult and disrupts the institution’s image. The following are some major impacts:

- Profitability – It directly affects the profit of the institution. The more the NPA, the less profit is as the institution must make provisions for NPA, which causes 25% – 30% more provisions leading to lower profits.

- Liability Management -To manage NPA, banks have to lower the interest rates on deposits and increase the lending rates, affecting a bank’s business and economic growth.

- Asset Contraction – An increase in NPA slows down the rotation of funds, lowering the bank’s interest income.

- Capital Adequacy – Banks must maintain required capital on risk-weighted assets per Basil norms. The more NPA, the more required capital induction, leading to increased capital cost.

- Public Confidence – NPA disrupts banks’ creditworthiness. The public is frightened to make deposits with the bank having more NPA because they fear losing their money, as the bank’s liquidity endangers.

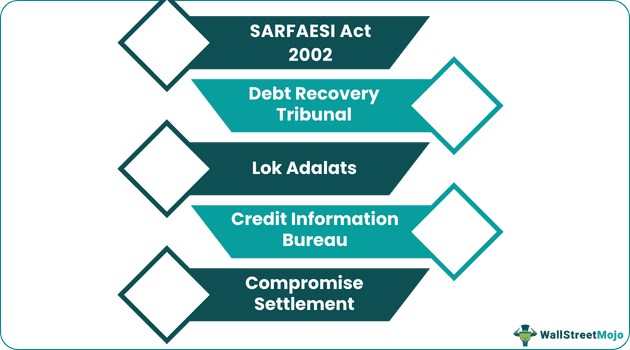

How to Reduce NPA – Indian Example

#1 – SARFAESI Act 2002 – This act gives the power to the bank to deal with NPA without the involvement of the courts. It gives the bank right to:

- Asset reconstruction

- Securitization

- Enforcement of security

#2 – Debt Recovery Tribunal – In 1993 Indian Parliament Act brought DRT into existence, which empowers banks to recover loans of ₹10 lakh and above.

#3 – Lok Adalats – This mechanism can recover small loans up to ₹5 lakhs per the guidelines of RBI.

#4 – Compromise Settlement – Used to settle loans up to ₹10 crore amounts where the borrower experiences genuine difficulties repaying the amount under this method, the proportionate amount recovers from the borrower.

#5 – Credit Information Bureau – Third-party agencies such as CIBIL keep the record of the defaulters and the financial health of the borrowers. Banks may seek the help of such agencies before lending money to them.

Limitations

NPA is the most important tool to determine any bank or financial institution’s soundness, performance, and health. The more the NPA, the lower the performance of other banks or institutions, and the less the bank is creditworthy. It creates a negative effect on the goodwill of a bank, and this can be judged only by total NPA. So it is a very important measure to be carried out. The mentioned below are some disadvantages:

- Reduced Income – With the increase in NPA assets, financial institution’s profitability reduces as it reduces the realization of assets.

- Falling Financial Strength – As NPA is nothing other than assets with reduced chances of realization, these directly affect the financial strength of a business.

- Disrepute to Business Image – It drastically affects the financial image of the organization.

- Falling Credibility – It adversely affects the image of lending institutions. As a result, lenders also do not show interest in lending due to the increased risk of non-repayment.

- Loss of Capital/Reserves – Due to increased chances of non-recovery, an organization not only loses future profitability but also incurs a loss of the principal amount granted.

Conclusion

Non-Performing Assets (NPA) are assets classified based on non-recovery of installments as per the agreed terms and conditions, usually classified after 90 days of non-recovery. They are further classified as standard, sub-standard, doubtful, and lost assets. It harms the organization’s profitability, financial strength, capital adequacy, and public image. Various government organizations are set up under the parliament act or other statutes for monitoring the NPA of financial institutions, thereby reducing NPA and increasing the profitability of the organization and the economy as a whole.

Recommended Articles

This article has been a guide to the Full Form of NPA(Non-Performing Assets). Here, we discuss types, NPA works, examples, impacts, and limitations. You may refer to the following articles to learn more about finance: –