Part of our Profitability Ratios guide

What Is Return On Average Capital Employed (ROACE) Formula?

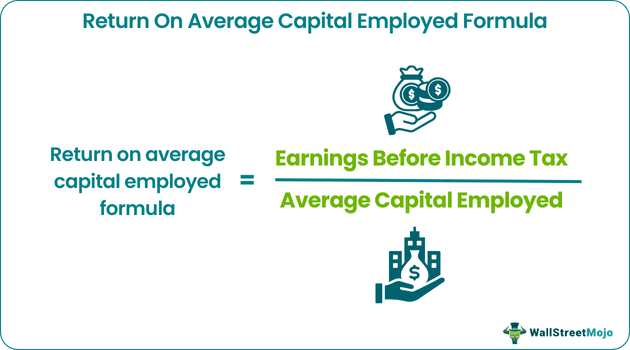

Return on Average Capital Employed (ROACE) is an extension of the Return on Capital Employed ratio. Instead of the total capital at the end of the period, it takes an average of the opening and closing balance of capital for some time. It is calculated by dividing the earnings before interest and taxes (EBIT) by Average total assets minus all the liabilities.

Return on Average Capital Employed Excel Template

Download Excel Template

Also, check out this detailed article on ROCE

- The return on average capital employed considers the closing and opening balances instead of the total capital employed.

- Calculate this by dividing the earnings before tax and interest by the average capital employed. It is a metric for assessing the productivity of the firm.

- The EBIT (earnings before interests and taxes) and the average capital employed are included in the two parts of the ratio.

- Companies use this measure for industries that are capital-intensive and require a considerable amount of base capital.

Return on Average Capital Employed Formula Explained

The return on average capital employed is a metric widely used in the financial market to measure the profit-earning capacity of a business concerning the average capital it employees to generate that profit. It is a valuable indicator used to assess the company’s efficiency level and management’s use of capital optimally to generate maximum earnings.

In the ratio, we have two parts.

- The first part is EBIT (earnings before interests and taxes). EBIT is operating income. If we look at the company’s income statement, we would see that after deducting the operating expenses from the gross profit, we get operating income or EBIT. You may ask why we are considering EBIT instead of net income. Operating income directly reflects the income generated from the business; moreover, operating income doesn’t include income from other sources.

- The second part is the average capital employed. To find out the capital employed, we can take two approaches.

- The first approach can simply add equity and long-term debt.

- But there’s a second approach that is better than the first approach. In the second approach, we deduct the current liabilities from the total assets or add up equity and the non-current liabilities.

- The second approach is better because it directly shows what has been directly invested in the business (meaning this approach also includes other non-current liabilities other than debt).

Return On Average Capital Employed Formula Video

Example

Let’s take a simple example to illustrate the ROACE formula.

Example#1

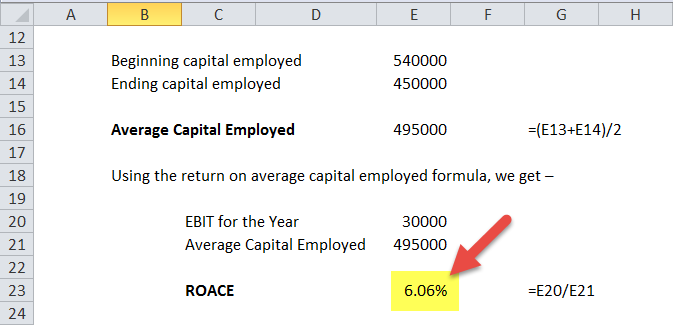

Benefits Inc. has the following information –

- EBIT for the year – $30,000

- The beginning capital employed – $540,000

- The ending capital employed – $450,000

Find out the ROACE.

First, we need to find out the average capital employed.

All we need to do is to do a simple average.

- Average Capital Employed = ($540,000 + $450,000) / 2 = $990,000 / 2 = $495,000.

- ROACE formula= EBIT / Average Capital Employed

- Or, ROACE formula = $30,000 / $495,000 = 6.06%.

Example#2

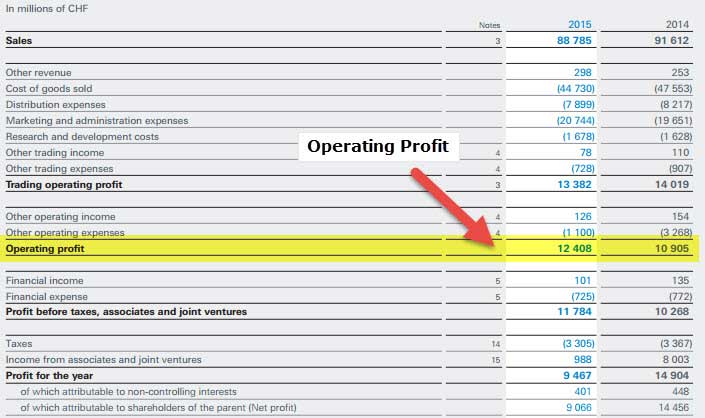

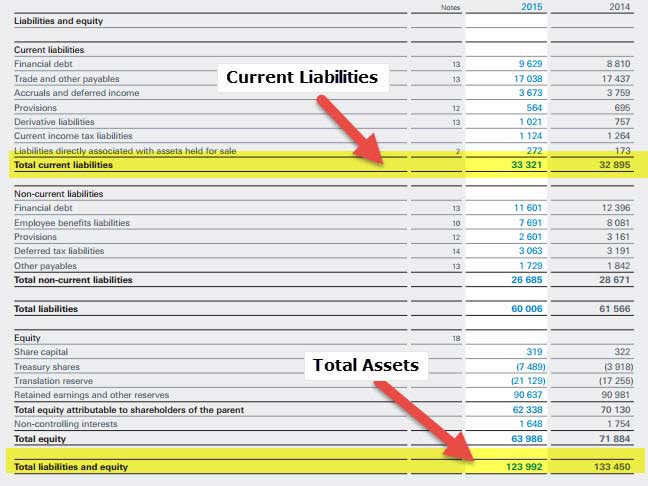

Below is the snapshot of Nestle’s Income Statement and Balance Sheet. For calculating ROACE, we require EBIT or the Operating profit.

Consolidated income statement for the year ended 31st December 2014 & 2015

source: Nestle Annual Report

Here three figures are important, and all of them are highlighted. First is the Operating Profit for 2014 and 2015. And then, the total assets and total current liabilities for 2014 and 2015 are needed to be considered.

- Operating Profit of 2015 = CHF 12,408

- Capital Employed (2015) = 123,992 – 33,321 = 90,671

- Capital Employed (2014) = 133,450 – 32,895 = 100,555

- Average Capital Employed = (90,671 + 100,555)/2 = 95,613

- ROACE = CHF 12,408 / 95,613 = 12.98%

The above examples clearly explains the concept using suitable case studies. The cases, both hypothetical and real, points out how to use the data available in the financial statements of the business to calculate the metric and interpret it in the correct manner.

Uses

Let us identify some important uses of the financial concept.

- Return on average capital employed is best used for capital-intensive industries.

- Companies that need a lot of capital upfront to start and run the business are capital-intensive industries. For capital-intensive industries, the ROAD would be lower.

- In other cases (if the company is not capital intensive), the ROACE should be higher.

- An investor should be careful about capital assets. It may so happen that these capital assets are depreciated, and as a result, the ROACE has been higher. But it is not because the profit is higher; rather, the ROACE is lower.

- It is a very important tool that is commonly used for evaluation of company performance and operational efficiency levels. Consistency in the value indicates a high efficiency level.

- It can be used as a benchmark for comparison between industry peers and competitors to assess where the business stands in the market.

- Investment decisions depend a lot on its value. Since it helps to evaluate the potential investment opportunity and helps the business select a good option for return, the stakeholders also feel satisfied with the company decisions and find the future potential of the company attractive.

- It helps to align the objective of the business with that of the financial goal and in the process, improve management performance.

- If the return on investment or capital is good, it gives a boost to the creditworthiness of the company since it has enough funds to pay off its debts. The lenders are also satisfied that the company is financially strong and this reduces the chance of default, thus give the company more opportunity to borrow.

- The business can predict a good profitability and growth opportunity for itself since the return generated from its capital are high and enough to fiancé future projects and investments for expansion. Thus leads to overall financial improvement.

- The relation with shareholders, creditors and other stakeholders of the organization improves based on the fact that the company is now better equipped to handle risks, pay off its liabilities, and also meet the return expectation, enhancing its position in the market.

Thus, it is important to note that it is a versatile and valuable metric that improves the overall company performance and can be comfortably used as a tool to evaluate the capital and resource utilization, management efficiency and profit earning capacity of the company in the field of corporate finance.

Calculator

We can use the following calculator to calculate the metric in a precise manner, without error.

Return on Average Capital Employed in Excel (with excel template)

Let us now do the same example above in Excel. This is very simple. First, you need to find out the average capital employed and provide the two inputs of Ebit and Average Capital Employed.

You can easily calculate the ratio in the template provided.

You can download this template here – Return on Average Capital Employed Excel Template.

Frequently Asked Questions (FAQs)

What is the difference between the return on capital employed and the return on average capital employed?

The return on capital employed is the total amount of assets a business utilizes instead of its liabilities. It helps the investors understand how well the business uses its assets. However, return on average capital employed construes the average liabilities and assets, the closing and opening balances.

What is a good figure for return on average capital employed?

A decent figure for this depends on the industry benchmark. Presently, a benchmark of 35% would be prevalent. Thus, any company with a ROACE of 20% would look good.

What factors affect the return on average capital employed?

To improve the return on average capital employed, the firm can start by paying off liabilities and increasing sales to earn enough revenue to acquire more assets; the overall balance sheet would look desirable.

Recommended Articles

This has been a guide to what is Return On Average Capital Employed Formula. We explain it with examples, uses along with calculator and video. Learn more from the below articles –