Part of our Profitability Ratios guide

What is Segment Margin?

Segment Margin means the profitability of an individual product line of a large business selling multiple products/services or to ascertain profit or loss or for a particular geographic location operating in multiple geographical regions and is used for comparing the profitability of different components of the company and relevant decision making.

- Segment margin is the profit or loss of a specific product line or location within a business that sells multiple products or operates in different regions, used to compare profitability and inform decision-making.

- Businesses utilize segment margins to assess the performance of various areas and analyze their profitability. This information can help determine whether to continue investing in those segments.

- Segment margin is the analysis and reporting of financials for each operating area of a multinational company to determine its profitability and financial position.

Explanation

Large multinational companies operating over a varied region or selling various products/ services would be interested in knowing how their different business segments are performing. You can evaluate the performance better if the company breaks down its operations into segments and determines segment margins. It is important to evaluate it to understand which part of the business performs above or below average. Also, it helps businesses to decide where there exists a need to invest additional funds. This concept is irrelevant for small business organizations since they don’t have multiple operating segments. According to generally accepted accounting principles, a public company must report profit and loss according to its segment separately if the total assets or revenue are 10 percent or more of the total companies’ profit or assets.

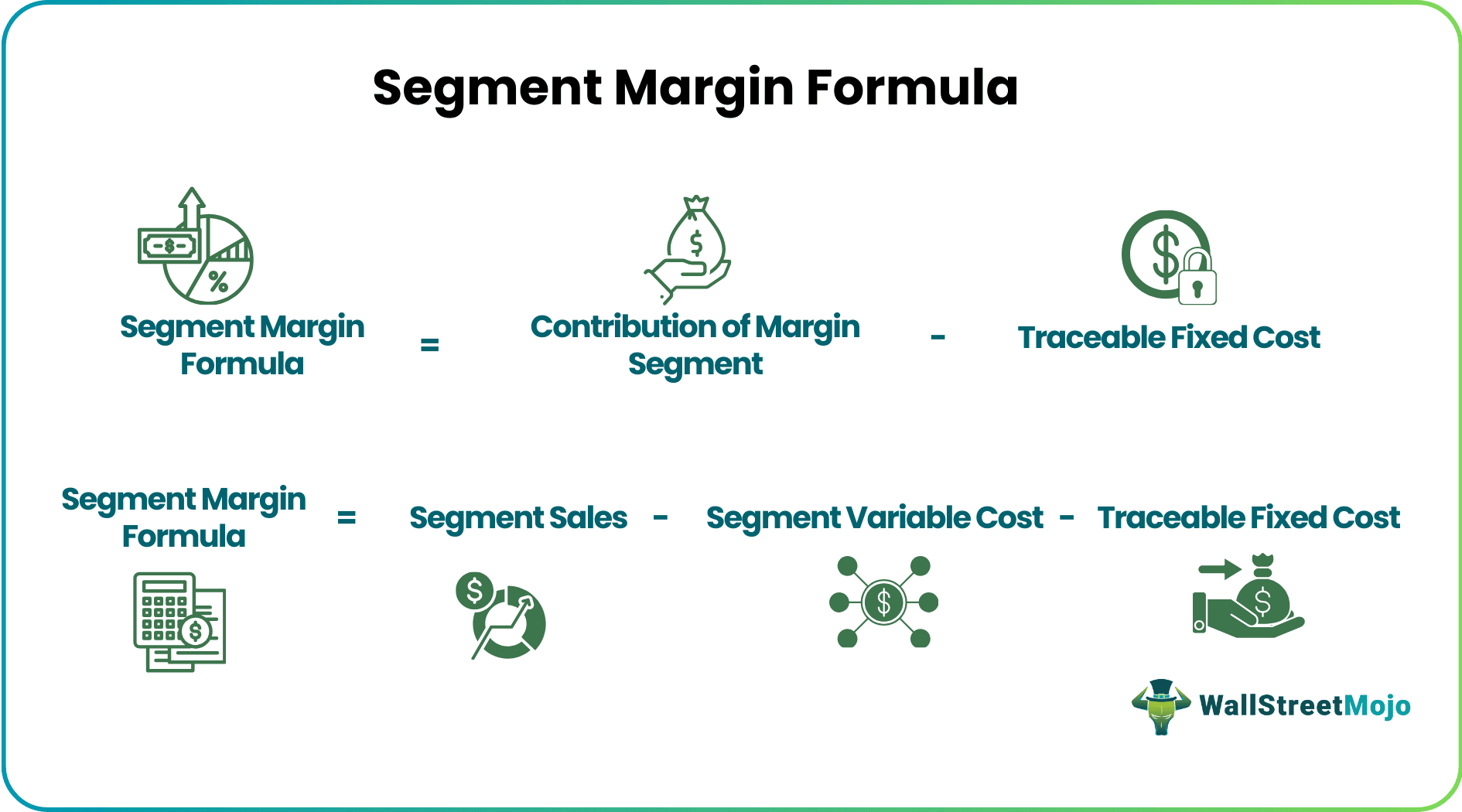

Segment Margin Formula

Segment Margin = Contribution Margin of Segment – Traceable Fixed Cost

OR

Segment Margin = Segment Sales – Segment Variable Cost – Traceable Fixed Cost

Here,

- Segment contribution margins = Segment Revenue – Segment Variable Cost

- Traceable fixed costs are those fixed costs directly attributable to a particular segment, and there will be no such cost if the segment shuts down.

Most businesses have departments based on the markets they serve, and all departments have various products. Each department’s product has some variable costs attached. Moreover, some of the fixed costs might incur due to the product. The rest of the fixed costs can be of different products, and some fixed costs might be common for all. And if the segment is a business unit, the margin of the segment will depend on the margin of contribution for all products, and the fixed cost will be traced to the department.

Example

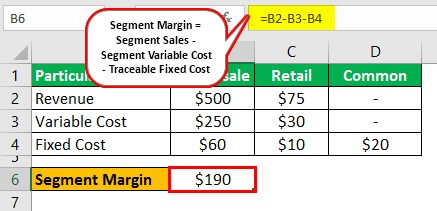

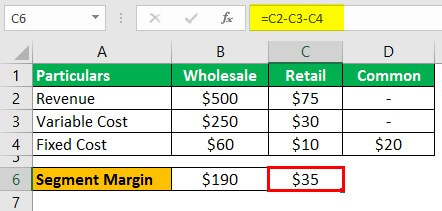

Ceat Tyre Inc. manufactures automotive tyres. It has two departments, retail and wholesale. Below are the cost and revenue of each department.

The wholesale department has two products, Light Motor Tyre (LMT) and Heavy Motor Tyre(HMT). Details are as under –

The company wants to know whether products of the wholesale department are profitable or not –

Solution

Segment margin calculation can be done as follows –

- Margin (Wholesale) = $500 – $250 – $60 = $190

- Margin (Retail) = $75 – $30 -$10 = $35

Margin calculation can be done as follows –

- Margin (LMT) = $100 – $100 – $25 = ($25)

- Margin (HMT) = $400 – $100 -$25 = $275

LMT of wholesale depart has a negative segment margin. The wholesale department can improve the profits by closing the LMT department.

(Please note that overall company profit is not overall, as common fixed costs are not deducted in any of the above calculations).

Segment Margin and Fixed Cost

Segment cost includes three types of fixed costs – avoidable fixed costs, unavoidable fixed costs, and common fixed costs. Avoidable fixed costs are very important in the decision-making process regarding continuing a product line or discontinuing it. This cost gets terminated if the product or segment line is discontinued. On the other hand, unavoidable fixed and common expenses are not relevant in decision-making for a product line. Unavoidable fixed expenses are essential to carry on a segment or product line and cannot be eliminated. This cost will still get incurred if the product line or segment is closed. Discontinuation of a segment will force the unavoidable expenses to be allocated to another product or segment line. Common expenses are the expenses forming part of the company and are allocated to various segments of the product line and cannot be eliminated as a part of a single segment margin analysis.

Advantages

- Companies use segment margin to check, document, judge, and analyze different business areas’ performance.

- By this, one can determine the profit earning capacity of the business segments and decide to carry on the segment or not.

- Business gets to know the worst sectors of its units.

- It increases transparency in reporting.

- Segment reporting can undertake drastic changes if the business operating in the overseas market is more demanding than business operations in the domestic market.

Disadvantages

- Focus on Short-Term Goals – Segment margin focuses on short-term numbers. Breaking down these numbers given the data point will help create pressure to reduce the losses and increase short-term earnings. If a business started a new division, in the beginning, this division would incur a loss in the beginning due to a non-efficient workforce and improper infrastructure. Still, eventually, over some time, it may generate profits. ·

- Data Manipulation – Identification and fixation of any particular sector as a different segment is not regulated by any ruling law. Still, it is left open for management to decide and mark different operating units as separate segments. It generates an open area for management to decide and manipulate the operating segment’s information, leading to misleading investors and other stakeholders

Conclusion

Segment margin can be described as determining and reporting financials of any large-scale multinational company’s separate individual operating area individually. The basic objective of this concept is to determine the profitability and financial position of the different operating segments. Segments can be identified at the product service level or a geographical level. Segment reporting helps management determine which segment needs greater attention and which should be scrapped.

Frequently Asked Questions (FAQs)

What is the difference between segment margin and contribution margin?

The contribution margin is the amount left over after subtracting variable expenses from sales revenue. The segment margin is what is remained after deducting traceable fixed costs from the contribution margin.

What does segment margin depend on?

If the segment is a business unit, its margin will be based on the contribution margin of all products, and the fixed cost will be assigned to the department.

What should not be included in the segment margin?

The formula for segment margin is calculated by deducting expenses from revenue, including only the variables directly related to the segment. Corporate overhead is not included in the segment margin as it is not involved in generating income or expenses for a specific segment.

How often should segment margin analysis be performed?

The frequency of segment margin analysis depends on the company’s size, complexity, and reporting requirements. Typically, large corporations conduct such investigations quarterly or annually, while smaller businesses do it less frequently.

Recommended Articles

This has been a guide to what is Segment Margin and its definition. Here we discuss the formula for calculation of segment margin along with advantages, disadvantages, and differences. You may learn more about financing from the following articles –