Part of our Profitability Ratios guide

What is Unit Contribution Margin?

Unit contribution margin is the amount of the product selling price over and above the variable cost per unit; put in simple words, it is the selling price of the product minus the variable cost that was incurred to produce the product. Overall, per unit contribution margin provides valuable information when used with other parameters in making major business decisions.

While the contribution margin per unit formula is beneficial for managers to consider while maximizing their profits, making decisions solely based on it or even cutting out on products with the lowest margin might not always be right. Managers should also consider the fixed cost associated with the production alongside.

Unit Contribution Margin Explained

The unit contribution margin is a financial metric used to assess the profitability of individual units or products sold by a company. It represents the amount of revenue generated by each unit after deducting the variable costs associated with producing or selling that unit. In simpler terms, it measures the incremental profit earned from each unit sold, which contributes to covering fixed costs and generating overall profits for the business.

To use the unit contribution margin calculator, one subtracts the variable costs per unit from the unit selling price. Variable costs include expenses such as direct materials, direct labor, and variable overhead directly attributable to the production or sale of the unit. The resulting figure represents the amount of revenue that remains to contribute towards covering fixed costs and generating profit after accounting for the variable costs associated with producing or selling the unit.

This margin is a critical financial measure for businesses as it helps management make decisions regarding pricing, product mix, and resource allocation based on numbers. A higher unit contribution margin indicates that a product is more profitable and contributes more towards covering fixed costs and generating profits. Conversely, a lower margin may signal the need to review costs, pricing strategies, or product offerings to improve profitability.

By analyzing the unit contribution margin of different products or units, companies can identify their most profitable offerings and allocate resources accordingly. Additionally, it assists in setting pricing strategies to ensure that products are priced appropriately to cover both variable and fixed costs while maximizing overall profitability. Overall, the unit contribution margin provides valuable insights into the financial performance of individual products or units and helps guide strategic decision-making within organizations.

Formula

Let us understand the formula that shall act as a basis of our understanding of the concept of per unit contribution margin through the discussion below.

Here, the variable costs per unit refer to all those costs incurred by the company while producing the product. These include variable manufacturing, selling, and general and administrative costs as well—for example, raw materials, labor & electricity bills. Variable costs are those costs that change as and when there is a change in the sale. An increase of 10 % in sales results in an increase of 10% in variable costs.

How To Calculate?

Let us understand the step-by-step process of how to calculate using a unit contribution margin calculator through the points below.

- Identify the price at which each unit is sold to customers.

- Subsequently, identify the costs directly attributable to the production or sale of each unit, such as direct materials, direct labor, and variable overhead.

- Subtract the total variable costs per unit from the selling price per unit.

- The resulting figure represents the unit contribution margin, which indicates the amount of revenue generated by each unit after deducting variable costs. This amount contributes towards covering fixed costs and generating profits for the business.

- Use the Formula- Unit Contribution Margin = Selling Price per Unit – Variable Costs per Unit.

- A higher unit contribution margin indicates that a product is more profitable, as it contributes more towards covering fixed costs and generating profits. The opposite is when a lower margin may signal the need for cost reduction or pricing adjustments to improve profitability.

Explanation of Contribution Margin in Video

Examples

Now that we understand the basics, formula, and how to calculate per unit contribution margin, let us also understand the practicality of the concept through the examples below.

Example #1

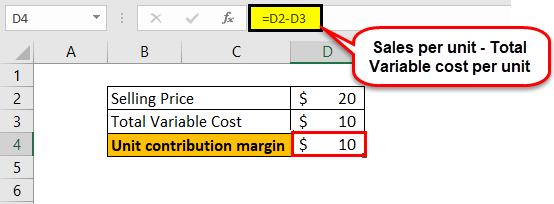

Let us start by taking an example from the introduction. Also, let us assume that the selling price of a single cupcake is $20. The variable cost part of making a single cupcake is $10. Hence, the contribution margin per additional unit of the cupcake will be:

$20 – $10 = $10

It simply means that by selling this cupcake, the net income or profit increases by $10.

An important point to be noted here is that fixed costs are not considered while evaluating the contribution margin per unit. As a result, there will be a negative contribution to the contribution margin per unit from the fixed costs component.

Example #2

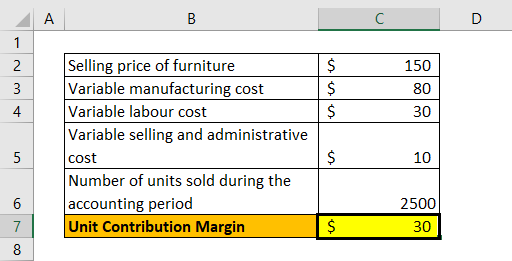

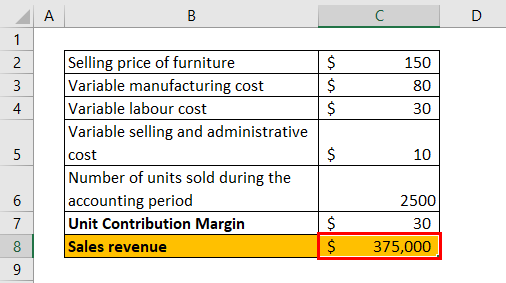

Let’s look at another example where a company manufactures furniture sets. The required data is as follows:

- The selling price of the furniture set = is $ 150

- Variable manufacturing cost = $ 80

- Variable labor cost = $ 30

- Variable selling and administrative cost = $ 10

- Number of units sold during the accounting period = 2500

As unit contribution margin formula = Sales per unit – Total Variable costs per unit

= $ [150 – (80+30+10)]

= $ [150-120] = $30

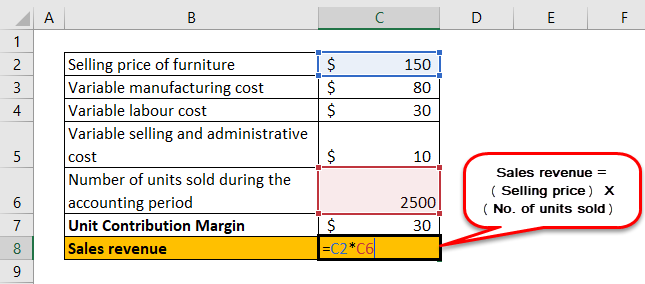

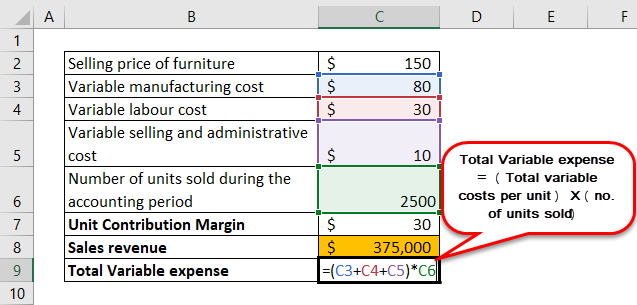

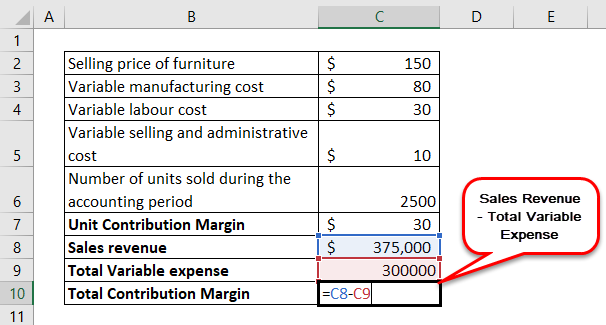

In the above example, the Total Contribution Margin would be calculated as follows:

- Total contribution margin = Sales Revenue – Total Variable Expenses

- Sales revenue = (Selling price)*(No. of units sold) = 150*2500

Sales Revenue will be:

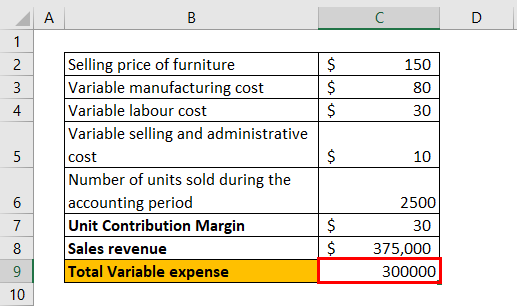

- Total Variable expense = (Total variable costs per unit)*(no. of units sold)

- = (80+30+10)*(2500)

So, the Total Variable expense will be:

So, Total Contribution Margin = 375000-30000 = $ 75000

Total Contribution Margin will be:

Example #3

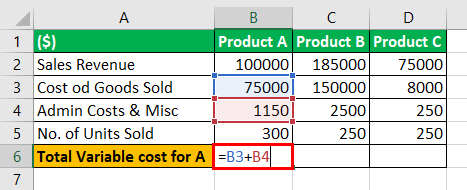

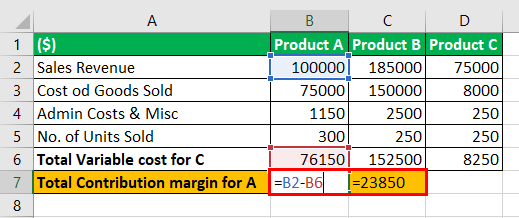

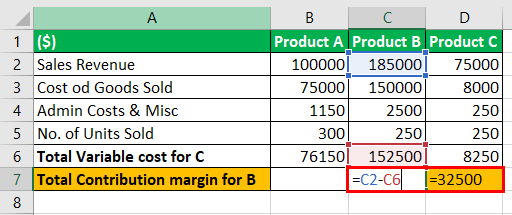

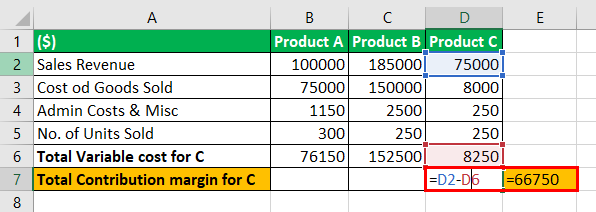

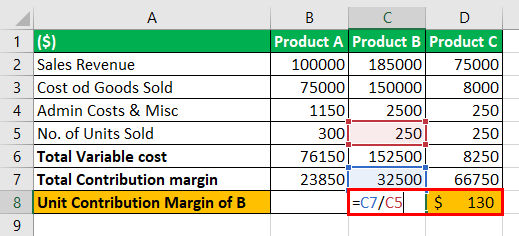

In this example, we’ll consider a case where a corporation is into multiple product manufacturing. Consider the below table for the required business data:

| (S) | Product A | Product B | Product C |

|---|---|---|---|

| Sales Revenue | 100000 | 185000 | 75000 |

| Cost of Goods Sold | 75000 | 150000 | 8000 |

| Admin Costs & Misc. | 1150 | 2500 | 250 |

| No. of Units Sold | 300 | 250 | 250 |

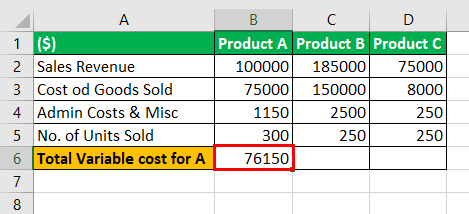

Total Variable cost for A = 75000+1150

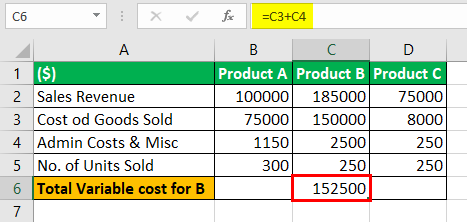

Total Variable cost for B = 150000+2500

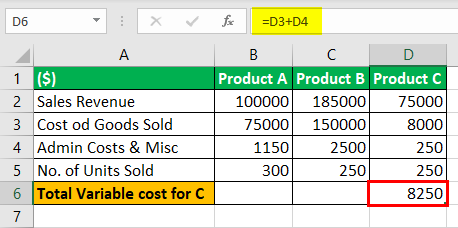

Total Variable cost for C = 8000+250

And,

Total Contribution margin for A = $(100000-76150) = $ 23850

Total Contribution margin for B = $(185000-152500) = $ 32500

Total Contribution margin for C = $(75000-8250)= $ 66750

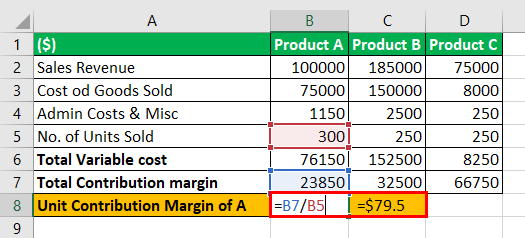

So,

Contribution Margin of A = $ (23850)/ (no. of units of A sold) = $ 23850/300 = $ 79.5

Contribution Margin of B = $ (23850)/ (no. of units of B sold) = $ 32500/250 = $ 130

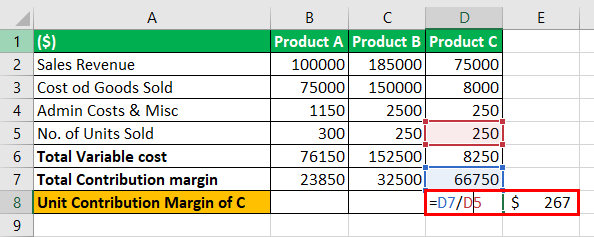

Contribution Margin of C = $ (23850)/ (no. of units of C sold) = $ 66750/250 = $ 267

Note: As we can see here, while the revenue share is largest for Product B, Product C has the highest Unit Contribution margin. So in effect, it is product C that has the most profitability.

How is It Helpful to a Business?

Let us understand how a unit contribution margin is helpful to a business through the discussion below.

- It helps us determine how an additional unit of a product affects the company’s profit. It is obtained by subtracting variable costs incurred while producing that additional product unit from its sale.

- It helps a business understand how profitable it is at the product level. It gives managers an essential insight into various aspects of the business and helps them make better-informed decisions. Again, referring to our earlier example, knowing the unit contribution margin of each of the products sold at the bakery will help the manager make several decisions.

- These decisions could range from deciding which product to continue or discontinue producing and selling, how many additional units of a product to be produced, how to set the product’s price, or how to determine the commissions on sales.

Recommended Articles

This article has been a guide to what is Unit Contribution Margin. Here we discuss its formula, how to calculate, examples, and how it is helpful to a business. You may learn more about financial analysis from the following articles –