Written byAshish Kumar SrivastavAshish Kumar SrivastavEditorial HeadAshish, a seasoned finance professional, content editor, and blogger, brings over a decade of expertise. As Editorial Head at WallStreetMojo, he mentors writers and ensures quality. A self-published author and with a passion for financial literacy, Ashish's extensive knowledge covers investment banking,12+ years of experienceM.Sc.Investment bankingView Full Profile

Reviewed byDheeraj Vaidya, CFA, FRMDheeraj Vaidya, CFA, FRMContent Reviewer & Course DirectorDheeraj is a former J.P. Morgan and CLSA Equity Analyst with nearly two decades of experience in financial modeling, valuation, equity research, and corporate finance. He specializes in helping students and professionals develop practical and in-demand finance skills through structured and AI-powered,20+ Years of experienceCFA, FRM, IIT Delhi, IIM LucknowFinancial ModelingView Full Profile

A statement of retained earnings is a financial statement that shows how the retained earnings have changed during the financial period and provide details of the beginning balance of retained earnings, ending balance, and other information required for reconciliation. These funds can be used towards the development of the company such as research and development or infrastructure development.

The statement of retained earnings holds significance as it provides a snapshot of a company’s accumulated profits that have not been distributed to shareholders as dividends. It reflects the reinvestment of earnings into the business for growth, debt reduction, or other purposes. Analyzing this statement helps investors gauge a company’s financial health.

Statement of Retained Earnings Explained

The statement of retained earnings is a financial statement that outlines the changes in a company’s retained earnings over a specific accounting period. It begins with the balance of retained earnings at the beginning of the period and adjusts for net income or loss generated during the period.

Additionally, it incorporates dividends paid to shareholders, which reduces retained earnings. The statement of retained earnings provides insights into how a company reinvests its profits back into the business or distributes them to shareholders as dividends. It is an essential component of the overall financial reporting framework, offering stakeholders visibility into the company’s earnings retention and distribution policies.

Retained earnings are part of the net income retained by the company after dividend payments to the shareholders. Retained earnings are also called ‘retained surplus’ or ‘accumulated earnings.

A company retains a part of its net profit earned in the financial year for future growth, which could be by launching new products, R&D investments, acquiring other businesses, or paying off its debt. It is calculated using the following formula:

Retained earnings are reported on the balance sheet as well as the statement of retained earnings.

Retained Earnings Video Explanation

How To Prepare?

The preparation of a statement of retained earnings consists of various steps involving different departments and stakeholders of the organization. Let us understand the step-by-step process through the discussion below.

Below are the steps to prepare the statement of retained earnings –

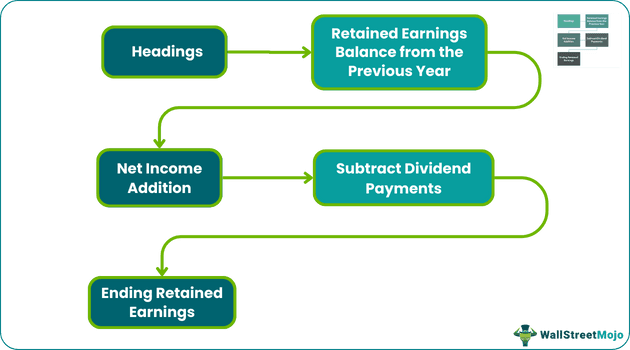

Headings

Its’ heading comprises three lines:

– Name of the Company – The second line gives the ‘Statement of retained earnings.’ – The third line represents the financial year for the retained earnings numbers that have been prepared, i.e., ‘Financial Year Ended 2018’ etc.

Retained Earnings Balance from the Previous Year

The first entry on the statement is the previous year’s carried-over balance. This entry can be taken from the previous year’s balance sheet or the ending balance of the previous year’s retained earnings. This is also called the beginning of retained earnings.

Let us consider the previous years retained earnings balance or the beginning retained earnings of a Company ABC Inc. is $ 500000.

Thus, the first entry will be:

Retained Earnings for the year ended 2017: $ 50000

Net Income Addition

Net income is added to the income statement. It comes as the second entry to the retained earnings. Therefore, to record net income in the statement, the company should prepare the income statement first and then the retained earnings statement.

Let’s assume the Company ABC Inc. had a net income of $ 100000.

Thus, it will be

Retained Earnings for the year ended 2017: $ 500000 Plus, Net Income 2018: $ 100000 Total: $ 600000

Subtract Dividend Payments

A dividend is any payment made by the company to its shareholders. It is subtracted from the net income for the year, as the remaining part is the retained earnings for that year. For example, let us say the Company ABC Inc. paid a dividend of $ 50000 to the shareholders.

Thus, it is:

– Retained Earnings for the year ended 2017: $ 500000 – Plus, Net Income 2018: $ 100000 – Total: $ 600000 – Minus: Dividend $ 50000

Ending Retained Earnings

After subtracting the dividend from the net income, we arrive at the ending retained earnings, which becomes the last entry to this statement.

– Retained Earnings for the year ended 2017: $ 500000 – Plus, Net Income 2018: $ 100000 – Total: $ 600000 – Minus: Dividend $ 50000 – Ending retained earnings: $ 550000

Thus, the above entries are shown on the Statement of Retained Earnings.

Additional Information

Although this statement is pretty straightforward, additional information can be provided in the footnotes to the statement. This additional information can provide details about the stock purchase, new issuance of stock or rights issue, etc. All these corporate actions affect the dividend payment. Hence additional information can be provided to the investors.

Examples

Let us understand how retained income statementis useful for an organization and what it indicated about the financial health of the organization through a couple of examples.

Example #1

Let us summarize the above example and prepare the Statement of Retained Earnings for the Company ABC Inc. The beginning retained earnings of the Company ABC Inc. is $ 500000, the company had a net income of $ 100000 and paid a dividend of $ 50000 to the shareholders.

The Statement at the end of the financial year is as below:

Example #2

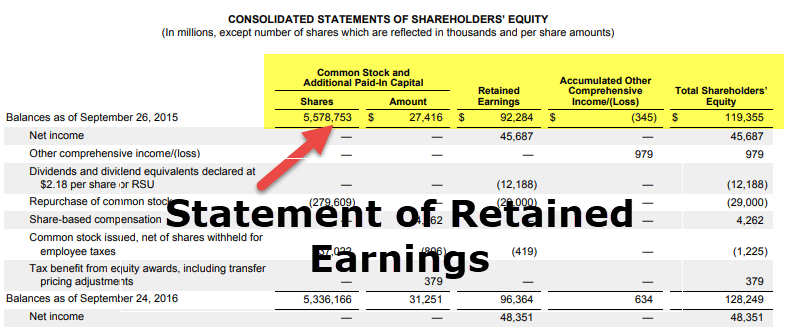

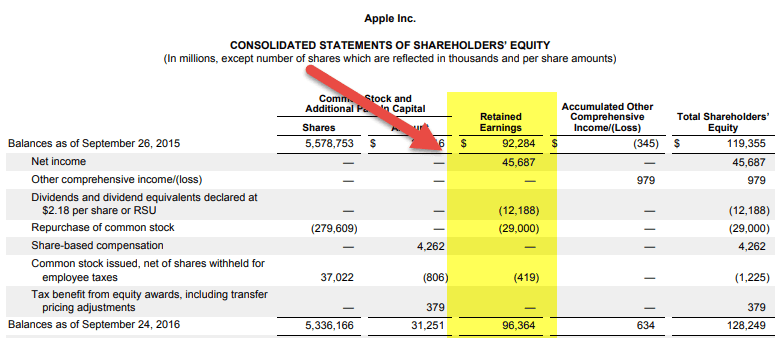

The below snapshot shows the Consolidated shareholder’s equity statement for Apple Inc. for the year ended 2018.

The retained earnings statement is very helpful to investors. Investors who have invested in a Company gain either from dividend payments or the share price increase. A mature firm is expected to pay a regular dividend. In contrast, a growing Company is expected to retain the income and invest in future business, thus expecting an increase in the share price.

Hence, it helps investors in both ways:

It shows dividend payments to the investors or helps them predict future dividends based on the earnings.

From retained earnings, the investors can analyze how much money is reinvested in the business, which may lead to a future increase in the share price.

Also, it can be used by investors to compare companies in similar kinds of business. However, it is not always prudent to compare two Companies only based on the retained earnings as retained earnings depend on various factors like the company’s age, dividend policy, and the business’s nature, thus affecting the dividend policy of the Company, and the nature of the business, thus affecting the profitability of the company.

Recommended Articles

This article has been a guide to what is Statement Of Retained Earnings. Here, we explain how to prepare it, examples, relevance, and uses in detail. You may learn more about accounting from the following articles –