Part of our Shareholder Equity guide

What Are Appropriated Retained Earning?

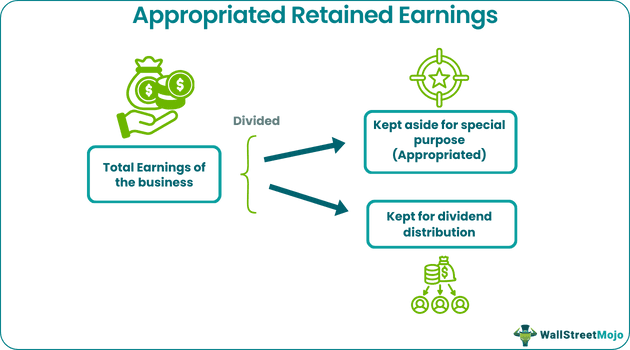

Appropriated Retained Earnings are the portion out of the total retained earnings that have been kept aside by the company’s board of directors to use for the specific purpose as mentioned by them and thus are not available to be distributed as dividends.

In simple words, Appropriate retained earning is the part of the retained earnings that the board has approved of Directors for specific purposes, including research and development, stock repurchase, reduction of debt, acquisition, etc. The Company can have more than one appropriated account, and different accounts will suggest the purpose of using such earnings.

Appropriated Retained Earnings Explained

The retained earnings the company has earmarked for a specific purpose are called appropriated retained earnings. Such appropriation is voluntary by dividing the retained earnings into various headings, denoting the use for which appropriation has been made.

The purpose of such appropriation or setting aside of earning, as determined by the board of directors or management of the company is specified and outlined clearly in the annual reports, financial plans and any other official documents that the stakeholders can access. Thus, this portion of profits are not for general use.

The money can be set aside to meet any capital expenditure like purchase of new plant, machinery, equipments, expansion plans, buying property. It may also be used for investment in research and development purpose so as to bring in innovation, new projects, upgradation of system or products and services.

It may also be used to repay debts, and which is an obligation that puts pressure on the financial resources of the company and may bring down the creditworthiness. The company may also create a fund or reserve using the appropriated earnings to pay dividends in future in case it predicts that the future earnings may not be enough to do so, thus ensuring a steady flow of dividend for shareholders.

In contrast, unappropriated retained earnings are part of retained earnings that are not classified for a specific use. Although the retained earnings are specified in various accounts, if there is a liquidation case, such accounts will have no meaning, and all the retained amounts will be available to be paid to the creditors or shareholders.

Retained Earnings Explained in Video

List Of Appropriated Retained Earnings Accounts

Given below is a list of accounts that are commonly created in the company for the purpose of using the appropriated part of profits earned by the company.

- Acquisitions

- Debt reduction

- Research and Development

- New Construction

- Marketing campaigns

- Product development

- Stock buyback

- Reserve for future losses

- Reserve for insurance payments/ guarantees

- Reserve for loan/ bond covenants imposed by creditors or bondholders

The intention behind having this is that the board clearly defines the purpose of the earnings it has retained (and not given to the shareholders as the dividend). It also shows that the Company has better planning as it specifies the amount it will spend on various activities.

It should be noted that the Company is not bound by a legal contract to appropriate retained earnings. It’s the prerogative of the Company to set aside the profits of the Company for various purposes. A voluntary transfer of retained earnings is done to multiple appropriated accounts.

Examples

Let us understand the concept with the help of some suitable examples.

- A pharma company spends the right amount on research and developing new medicines and cures for diseases. They would like to maintain a healthy balance sheet for research purposes. Thus, the Company may decide to appropriate a portion of retained earnings for this purpose such that the shareholders cannot withdraw all the profits. It will ensure the Company can fund its research and development programs without facing a liquidity/ funding crunch.

- A real estate company in the business of building residential and office spaces must purchase land and build the property. Thus, it can appropriate a portion for purchasing such lands and may use the amount as and when the Company feels an excellent opportunity.

The above examples give us a clear idea about the concept and explains why and how a company may keep aside its profits for uses in some special purpose and how such fund arrangements lead the company towards growth and expansion without raising money from outside sources, thus avoiding the financial pressure and obligation to pay back the amount to lenders or investors.

Journal Entries

→ Explore all 30 Journal Entries articles

Let us see how the appropriate retained earnings are recorded in the financial statements. The recording does not involve setting aside cash, but only two different entries are made, i.e., relevant retained earnings and unappropriated retained earnings.

The Board of Directors directs these separate entries.

Suppose a company had to set aside $ 50000 from the retained earnings as a separate account for Research and development purposes. In that case, it will debit the retained earnings account and credit the appropriated retained earnings account.

| Particular | Debit | Credit |

|---|---|---|

| Retained Earnings | $50,000 | |

| Retained Earnings Appropriation for Research and Development Purposes | $50,000 |

On the balance sheet, the retained earnings appropriation appears in the equity section, and it can be shown as below:

| Shareholder’s Equity | Amount ($) |

|---|---|

| Common Stock | $25,000 |

| Preferred Stock | $20,000 |

| Total Paid in Capital | $45,000 |

| Retained Earnings: | |

| Appropriated for research and development purposes | $50,000 |

| Unappropriated | $30,000 |

| Total Retained Earnings | $80,000 |

| Total Stockholder’s Equity | $1,25,000 |

As seen above, the appropriated retained earnings do not decrease the shareholders’ equity or the retained earnings but restrict the use of the amount only for a specific purpose.

However, nowadays, the formal use of appropriated earnings is decreasing. Instead, companies mention any such amount in the footnotes to the financial statements.

For example, – Note 9. Retained earnings restrictions. According to the provisions in the loan agreement, retained earnings available for dividends are limited to $25,000.

Such footnotes appear after the formal financial statements in “Notes to Financial Statements.” So, for example, the Retained Earnings account on the balance sheet would be referenced as follows: “Retained Earnings (see note 7)… $25,000″.

Is Restricted Retained Earnings The Same As Appropriated Retained Earnings?

Restricted retained earnings are before retained earnings, which the Company must keep or retain due to a contractual agreement, law, or covenant. A third party requires the Company to retain some amount, and the shareholders can be distributed dividends after such an amount is retained.

Appropriated retained earnings should not be confused with the restricted retained earnings. Since Appropriated retained earnings are voluntary, the company is not bound by a third party to retain such amounts. Also, such appropriation is not bound by contract or law, and it is on the Board of Directors that such an entry is made in the balance sheet, whereas the contract limits restricted retained earnings.

Appropriated Retained Earnings Vs Unappropriated Retained Earnings

The above two financial concepts refer to two different categories of retained earnings that the business keeps in its books, Let us study the differences between them in details.

- The former refers to the part of the profits earned by the business that is kept aside for meeting some special needs but the latter refers to the part of profits that are not set aside for any specific purpose but may be used for meeting any general needs.

- The purpose of the former may be situations like capital expenditure, legal requirements, debt repayment, research and development, etc whereas latter can be used for anything related to the ongoing operations of the business.

- It is necessary to disclose the appropriated part of the profits in the fianmcial statements of the company for the knowledge of the stakeholders but is it not the case with the unappropriated part.

- The former successfully provides an insight into the usage or the fund in financial planning which gives an idea to its stakeholders about its financial commitment, whereas the latter does not give any specific idea about the usage of funds by the business.

- Since the former puts aside the money for special purpose, there is less flexibility in the usage of the amount because it is already reserved. But the unappropriated part gives a flexibility to the business to use it for any useful purpose as and when need arises.

Thus the main difference between them lies in the fact that how the funds are used and accounted for in the organization.

Recommended Articles

This article has been a guide to what are Appropriated Retained Earnings. We explain its differences with unappropriated retained earnings & journal entries. You may learn more about accounting basics from the following articles –