Part of our Shareholder Equity guide

What Are Equity Examples?

Equity is anything invested in the company by its owner or the sum of the total assets minus the sum of the company’s total liabilities. E.g., Common stock, additional paid-in capital, preferred stock, retained earnings, and the accumulated other comprehensive income.

The equity value is a critical metric to understand a company’s or firm’s financial position on any reporting date. Positive equity with an increasing trend is always a good sign for any company. In contrast, a declining trend in equity value is indicative of weak management, and it could be a signal that the company is nearing insolvency.

Equity Examples Explained

The term equity examples refer to the various options that signify ownership interest in the business operations of an asset, property, or organization. The examples of such ownership can be varied and similarly, the asset can also vary based on the type of organization and business objective. Owners equity examples is a very critical and useful financial concept.

They can be in different forms, as given in the list below. It shows or evaluates gains and losses based on fluctuations in the asset valuation.

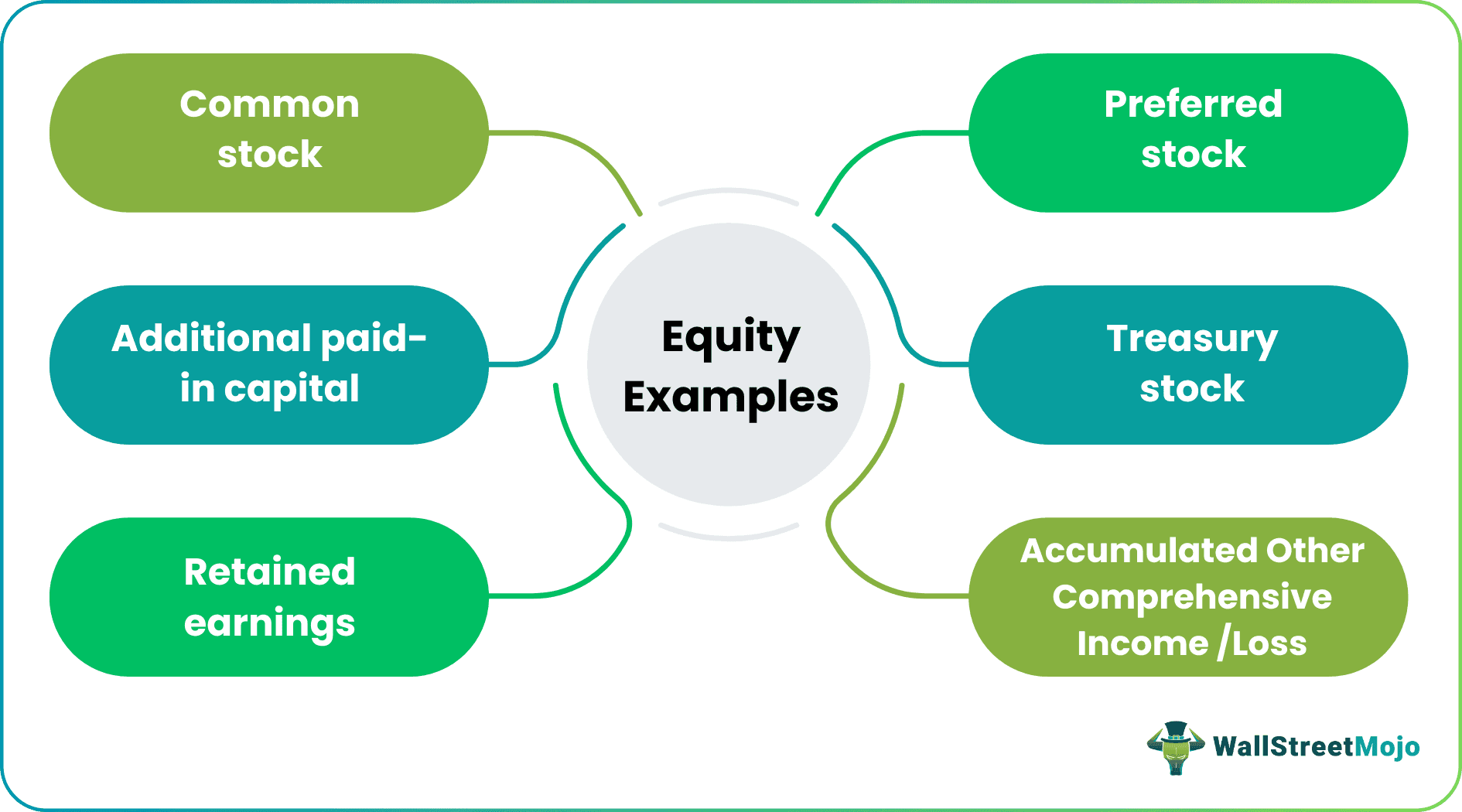

Most common shareholders’ equity examples include the following –

- Common Stock – Common stock represents the total number of shares multiplied by its par value.

- Preferred Stock – Preferred stock is similar to common stock. However, they get precedence in dividend payments.

- Additional Paid-in Capital – This is the amount over par value contributed by the shareholders and is an important concept in the owners equity examples.

- Treasury Stock – Treasury stock shares that the company has reacquired from the shareholders;

- Accumulated Other Comprehensive Income / Loss- This includes the gains and losses excluded from the income statement and reported below the net income.

- Retained Earnings – The portion of the income retained in the company to invest in the business.

We represent the Equity Formula as:

Equity = Total Assets – Total Liabilities

In the case of a corporation, we call the equity value either shareholder’s equity or stockholders equity examples. For a proprietorship, it is known as owner’s equity.

In the article below, we will find some the calculation examples of Shareholders’ Equity.

Examples

Let’s see some simple, practical examples of shareholder’s equity or stockholders equity examples to understand it better.

Example #1

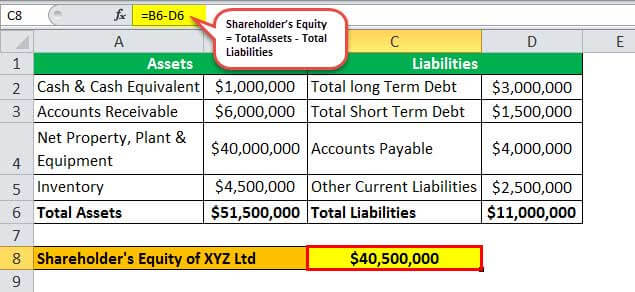

XYZ Ltd is a company that is engaged in the manufacturing of industrial paints. Recently the annual report for the year ending on December 31, 2018, was published. Given below are some excerpts from the balance sheet. Based on the following financial information, determine the shareholder’s equity of XYZ Ltd as of December 31, 2018.

Given, Total Assets = Cash & Cash equivalent + Accounts receivable + Net property, plant & equipment + Inventory

= $1,000,000 + $6,000,000 + $40,000,000 + $4,500,000

Total Assets = $51,500,000

Again, Total liabilities = Total long term debt + Total short term debt + Accounts payable + Other current liabilities

= $3,000,000 + $1,500,000 + $4,000,000 + 2,500,000

Total liabilities = $11,000,000

Therefore, the equity examples accounting of XYZ Ltd can be calculated using the below formula as,

= $51,500,000 – $11,000,000

Shareholder’s Equity of XYZ Ltd = $40,500,000

Therefore, the shareholder’s equity of XYZ Ltd stood at $40,500,000 as of December 31, 2018. A healthy positive equity value indicates a strong financial position of the company that confirms its going concern.

Example #2

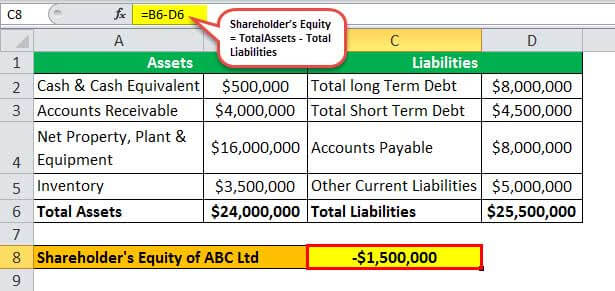

Now, let us take the example of ABC Ltd, an ice cream manufacturing company. The following information is made available as per the annual report released for the year ending on December 31, 2018.

Based on the following financial information, determine the shareholder’s equity of ABC Ltd as on December 31, 2018.

Given, Total Assets = Cash & Cash equivalent + Accounts receivable + Net property, plant & equipment + Inventory

= $500,000 + $4,000,000 + $16,000,000 + $3,500,000

Total Assets = $24,000,000

Again, Total liabilities = Total long term debt + Total short term debt + Accounts payable + Other current liabilities

= $8,000,000 + $4,500,000 + $8,000,000 + 5,000,000

Total liabilities = $25,500,000

Therefore, the shareholder’s equity of ABC Ltd can be calculated using the below formula as,

= $24,000,000 – $25,500,000

Shareholder’s Equity of ABC Ltd = – $1,500,000

Therefore, the shareholder’s equity of ABC Ltd stood at – $1,500,000 as of December 31, 2018. This negative equity value indicates a very weak financial position which may be close to bankruptcy or winding up.

Example #3

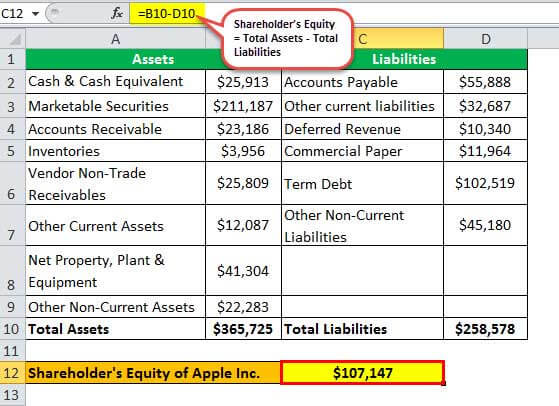

Let us now take the example of a real company – Apple Inc. and understand the equity examples accounting. The annual report for the period ended on September 29, 2018. As per the publicly released financial data, the following information is available. Based on the information, determine the stockholder’s equity of Apple Inc. as on September 29, 2018.

All amounts in millions

Given, Total assets (in Mn) = Cash and cash equivalents + Marketable securities + Accounts receivable + Inventories + Vendor non-trade receivables + Other current assets + Net property, plant & equipment + Other non-current assets

= $25,913 + $2,11,187 + $23,186 + $3,956 + $25,809 + $12,087 + $41,304 + $22,283

Total Assets = $365,725

Again, Total liabilities (in Mn) = Accounts payable + Other current liabilities + Deferred revenue + Commercial paper + Term debt + Other non-current liabilities

= $55,888 + $32,687 + $10,340 + $11,964 + $102,519 + $45,180

Total liabilities = $258,578

Therefore, the stockholder’s equity of Apple Inc. as on September 29, 2018 can be calculated as:

= $365,725 Mn – $258,578 Mn

Shareholder’s Equity of Apple Inc = $107,147 Mn

Therefore, Apple Inc.’s stockholder’s equity, as of September 29, 2018, stood at $107,147 Mn.

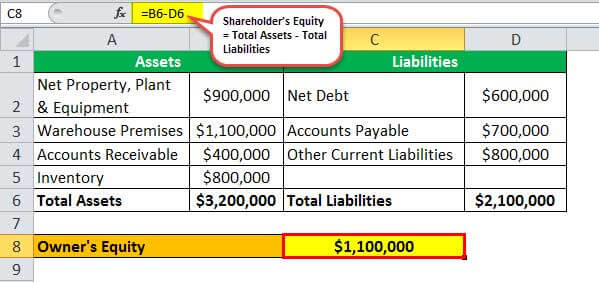

Example #4

Let us now take the example of a small business owner who is into the computer accessories business in the US. As per the balance sheet of the proprietorship firm for the financial year ended on March 31, 2018, the following information is available. Determine the owner’s equity of the firm. [since it has a single owner, as such owner’s equity instead of shareholders or stockholder’s equity]

Given, Total Assets = Net property, plant & equipment + Warehouse premises + Accounts Receivable + Inventory

= $900,000 + $1,100,000 + $400,000 + $800,000

Total Assets = $3,200,000

Again, Total liabilities = Net debt + Accounts payable + Other current liabilities

= $600,000 + $700,000 + $800,000

Total Liabilities = $2,100,000

Therefore, the owner’s equity of the firm as on March 31, 2018, can be calculated as,

= $3,200,000 – $2,100,000

Owner’s Equity = $1,100,000

Therefore, the owner’s equity of the firm, as on March 31, 2018, stood at $1,100,000.

The above equity examples in business give us a very good idea about the calculation of equity using data and financial information taken from the financial statements of companies. The companies are from different sectors, and are of different scale of operation, from small business to multinational enterprises.

Equity Examples Vs Equality Examples

The above are two different concepts and deal with completely different situations. Some points highlighted below will explain the basic differences of the two.

- The former deals with ownership rights or interests in various forms of assets whereas the latter deals with equal distribution of various services.

- The equity examples in business deals with assets like various forms of stocks which may includes preferred shares, common shares or retained earnings, which are the part of profits kept aside for use in the business, etc. But the latter deals with equality in accessing different opportunities related to the basic amenities in life like the food, clothing and shelter, equality in the workplace , equal rights to health benefits, etc.

- The former seeks to provide the details about the share of the owners in the business or the interest of investors in the share capital whereas the latter strives to give equal treatment or sameness in every sphere of the society and eliminate any disparity of opportunity.

Thus, the above points clarify the basic differences between the two concepts.

Recommended Articles

This article has been a guide to what are Equity Examples. We explain them with a few examples and the differences with equality examples. You may learn more about accounting from the following articles –