Part of our Shareholder Equity guide

What Is A Partnership Capital Account?

A partnership capital account is an account that contains all the transactions occurring between the partners and the partnership firm, such as the initial contribution of capital in partnership, the interest of capital paid, drawings, the share of profit, and other adjustments. It is required to maintain proper accountability and transparency between the partners and the firm.

It records different types of transactions. While the opening balance of the account is equal to the contribution that each partner makes in the firm, the ending balance obtained after recording the details is the amount that each partner in the partnership set up is meant to receive.

Partnership Capital Account Explained

A partnership capital account is an account in which all the transactions between the partners and the firm are to be recorded. It maintains records of different types of transactions, which include:

- The contributions by partners to the firm. Starting from the initial contribution to the subsequent ones, each and every transaction detail is recorded. The partners can either make contributions in the form of cash or market value of the assets.

- The account also records the profits made and losses incurred by the business. It determines the allocation of the same based on the specified proportions of the partners based on the partnership agreement.

- Lastly, the account also clears the picture, indicating the distributions to be made to the partners based on their shares.

With the preparation of the partnership capital account, it becomes easy to distribute the assets and liabilities to the partners and becomes easy to settle the account at the time of admission or retirement of partners. But in the case of a partnership other than a limited liability partnership, the capital account becomes useless as the partners have to pay from the personal estate in case assets are less than liabilities, and the capital account cannot be enforced for limitation of liability. Moreover, the basis of the partnership can be changed with the transactions like salary and interest to partners, which can sometimes create conflicts between the partners.

A business entity in which two or more persons doing business together agree to share the profits arising from business in the pre-defined profit ratio as partners is called the partnership firm. The partnership agreement can be oral as well as written. The profit-sharing can also be based on capital contribution or mutually decided.

The accounts of the partnership firm differ from that of the proprietorship. It also contains the partners’ capital account in which the capital contributed by partners and all the transactions between the firm and partners are to be recorded. The partner’s capital account can be of two types, i.e., current and fixed capital. If the account is a fixed capital account, then the only capital contribution is to be credited, and all other transactions are to be recorded in the current account.

Format

The standard partnership capital account format to show how the details of transactions and contributions are recorded is presented below:

How to Calculate?

Usually the capital contribution depends upon the share of profits like if business of partnership firm requires the investment of $ 1,000,000 and there are four partners in the partnership firm and profit sharing ratio is equal then each partner’s contribution will be $ 250,000 ($ 1,000,000 /4) whereas if the profit sharing ratio is 2:5:1:2 then the capital contribution of partner A will be $ 200,000 ($ 1,000,000 * 2/10), partner B will be $ 500,000 ($ 1,000,000 * 5/10), partner C will be $ 100,000 ($ 1,000,000 * 1/10) and partner D will be $ 200,000 ($ 1,000,000 * 2/10).

By the mutual decision, Partners can contribute more or less, which may not be as per the profit sharing ratio, and sometimes, in partnership, one should contribute the capital. Others will invest the time and talent.

The steps for calculating the partnership capital account are as under:

- Step #1 – Credit the capital account with the capital contributed by partners, the share of profit, remuneration of partners, interest on capital, and any receipt or asset directly associated with the partner.

- Step #2 – Debit the capital account by drawings, any liability directly related to the partner, etc.

- Step #3 – Share of profit is distributed in the profit-sharing ratio before calculating closing capital.

- Step #4 – Closing capital is calculated by reducing the debits from the credits to calculate the effective capital contribution.

- Step #5 – The closing capital is transferred to the balance sheet as a partner capital account.

Examples

Let us consider the following instances to understand the concept better:

Example 1

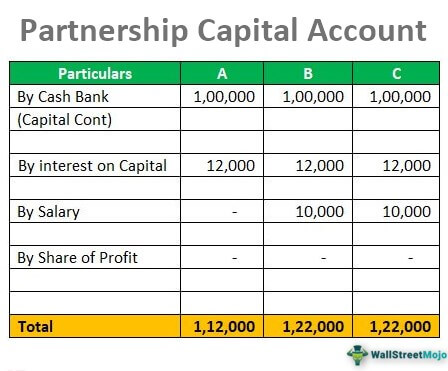

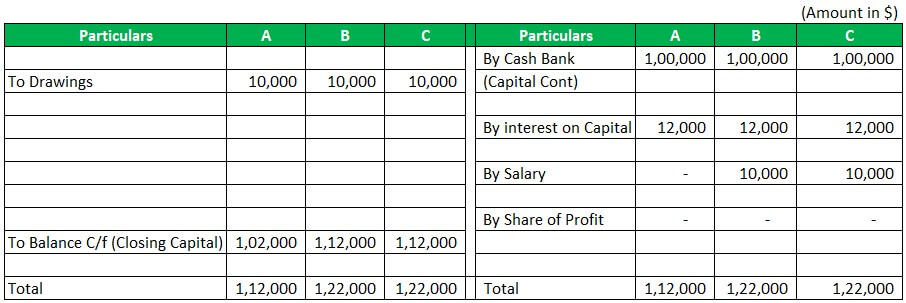

ABC and Co are a partnership firm with the three partners, A, B, and C. Profit sharing ratio of each partner is equal, and the capital contribution of each partner is also equal. The total requirement of investment in the business is $ 300,000. The firm does not maintain a separate current account and all the transactions are to be recorded in the capital account itself. Other details are as under:

Draw the Partners Capital account and record the above transactions.

Solution:

- Capital Contribution = $ 300,000 / 3 = $ 100,000

- Interest on Capital = $ 100,000 * 12% = $ 12,000 per partner.

- Profit Share =$75,000/3 =$25,000 per partner

Example 2

Sec 704 (a), which has been ruling the partnership capital account for long, underwent an amendment, given the way the taxpayers used it to abuse the provisions. Hence, Sec 704 (b) came into existence, which prevented the tax item shifting among partners that occurred through special allocations. Though the former allowed partners to reflect any economic arrangement in the agreement with flexibility, the latter made sure the clauses are not misused.

New Regulations

In October 2020, Internal Revenue Service (IRS) updated the instruction on Form 1065 with regards to the partnership capital account. Per the changes in the reporting requirements, partnership firms would require maintaining the capital accounts on a tax basis. Browsing through page 31 of the Form updated in 2020 provides all details about how to report the details in the account using tax basis method. It mentions three methods for adjusting the opening balance – tax basis method, modified outside basis method, Section 704 (b) method, and modified previously taxed capital method. According to the data generated by the IRS, many partnerships have already been seen implementing the tax basis method using multiple measures to adjust the opening balance of the account.

Advantages

A partnership capital account is quite useful as it makes easy for the partnership firms to keep track of the contributions of each partner and their share of income in accordance with the same. The clarity that these accounts provide make them one of the most significant records for the firms to maintain.

Let us have a look at the benefits offered by these accounts to partners in a partnership firm:

- Transparency in the records is maintained through the capital account of partners.

- In the event of the closure of a business, the amount to be received or distributed to each partner can be easily determined.

- The liabilities of each partner can be easily fixed.

- Decisions can be easily taken to maximize the benefit to the firm because of transparent records.

- A partnership capital account can be presented and accepted as a legal document.

- With the transparency and clarity of accounts, it is easy to admit the new partner, or it gets easy to settle the account at the time of retirement of a partner.

Disadvantages

Despite multiple advantages of these accounts, there are a few limitations that cannot be ignored. The individuals involving in recording the details in the partnership capital account must be aware of the demerits of maintaining such accounts.

Listed below are the limitations of these account. Let us have a look at them:

- In the case of a partnership other than a limited liability partnership, the partners are jointly and severally responsible for the outside liabilities; hence the risk of one partner is transferred to other ones in their profit-sharing ratio and from the personal estate if liabilities are more than assets and the partners capital account becomes of no value in this case as the capital account cannot be enforced for limited liability.

- As in most organizations, no separate current account is prepared; hence the basis of capital contribution gets changed with transactions.

- There are chances of conflict in case of a change in the basis of the capital.

Recommended Articles

This has been a guide to what is Partnership Capital Account. We explain its format, examples, how to calculate it, new rules, advantages, and disadvantages. You can learn more about it from the following articles –