Part of our Shareholder Equity guide

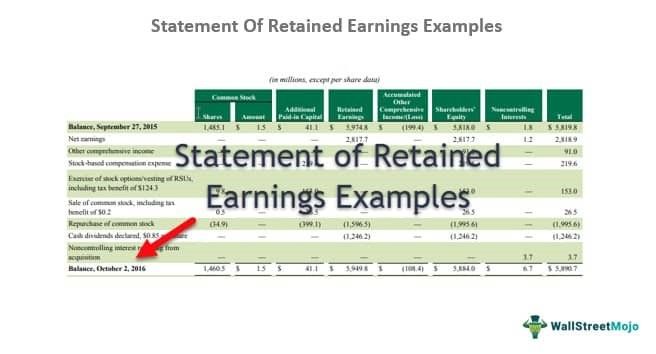

What Are Statement Of Retained Earnings Examples?

The statement of retained earnings examples show how the retained earnings have changed during the financial period. This financial statement provides the beginning balance of retained earnings, ending balance, and other information required for reconciliation.

The examples of Statement of Retained Earnings discussed below address as many situations/variations as possible. These situations are not fully exhaustive, and it is possible to encounter the ones that vary from those given below. However, one must remember that the core reasoning and concept behind retained earnings statements remain the same.

- The statement of retained profits details the evolution of retained earnings throughout the accounting period. The initial balance of retained earnings, the ending balance, and other details needed for the reconciliation are all provided in this financial statement.

- Retained earnings it is important to keep in mind, allowing us to estimate the amount of net income a company has left over after paying shareholders dividends (in cash or stock).

- With this knowledge, it would be simple for us to comprehend and present the statement of retained earnings.

- A statement of retained profits sometimes referred to as a statement of changes in equity, displays the entire amount of earnings that a company has accrued and retained in the business since it started operations.

Statement Of Retained Earnings Examples Explained

The statement of retained earnings examples show how much the company has earned and accumulated since its operation. Thus, they are a portion of the business profits that are kept aside for various purposes like paying dividends to shareholders, paying off loans, or making new investments that will bring further returns for the business.

These statements are prepared based on a series of steps, including three headings –

- One for company name,

- The second for the report named Statement of Retained Earnings,

- And third is the financial year’s overall report named as Fiscal Year Ended – preceded with the year mention.

The mention of the balance retained earning from the previous year along with the previous year adjustments, retained balance for the current year less any adjustments as applicable, net income, dividend payments mention, and ending retained earnings, etc.

We must remember that statement of income and retained earnings example help us gauge the net income left with a company after dividends (cash/stock) are paid to the shareholders. This understanding would make interpreting and presenting the statement of retained earnings very intuitive for us.

Retained Earnings Video Explanation

Examples

Below is the statement of income and retained earnings example.

Example #1 – KMP Limited

KMP Limited reported a Net Income of $ 84000 for the year ended December 31, 20X8. Retained Earnings on January 1, 20X8 were $ 47000. The company did not pay any dividends in the year 20X8.

Therefore, the statement of retained earnings will be –

Calculation:

Retained Earnings on December 31 20X8 = Retained Earnings on January 1, 20X8 + Net Income – Dividends Paid

= 47000 + 84000 – 0

= $ 131,000

Example #2 – ChocoZa

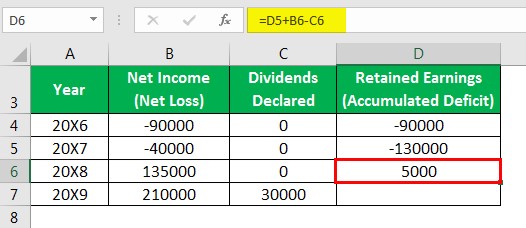

You started a homemade chocolate company called ChocoZa in the year 20X6. The Net Income (Net Loss) and dividends are paid below for the years 20X6-20X9.

| Year | Net Income (Net Loss) | Dividends Declared |

|---|---|---|

| 20X6 | -90000 | 0 |

| 20X7 | -40000 | 0 |

| 20X8 | 135000 | 0 |

| 20X9 | 210000 | 30000 |

The Retained Earnings (Accumulated Deficit) for all the four years are calculated as below:

Retained Earnings for Year 20X6

Year 20X6: Retained Earnings (Accumulated Deficit)= Beginning Retained Earnings + Net Income (Net Loss) – Dividends

= 0 – 90000 – 0

= -90,000

We have an accumulated deficit of -90,000 in the year 20X6. (Please note that a negative result for retained earnings implies an Accumulated Deficit)

Retained Earnings for Year 20X7

Year 20X7: Retained Earnings (Accumulated Deficit)= Beginning Retained Earnings + Net Income (Net Loss) – Dividends

= -90000 – 40000 – 0

= -13000

We have an accumulated deficit of -130,000 in the year 20X7

Retained Earnings for Year 20X8

Year 20X8: Retained Earnings (Accumulated Deficit)= Beginning Retained Earnings + Net Income (Net Loss) – Dividends

= -130,000 + 135000 – 0

= 5000

We have retained earnings of $5000 in the year 20X8

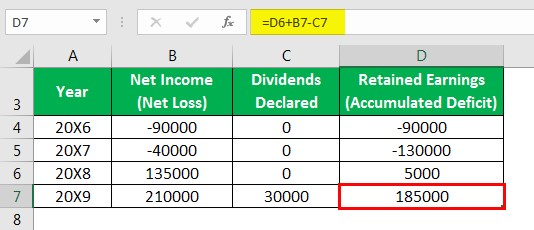

Retained Earnings for Year 20X9

Year 20X9: Retained Earnings (Accumulated Deficit)= Beginning Retained Earnings + Net Income (Net Loss) – Dividends

= 5000 + 210000 – 30000

= 185000

Thus, we have retained earnings of $ 185,00 in the year 20X9

The retained earnings and accumulated depreciation are summarized in the below table:

Example #3 – Dee Private Limited

These examples of retained earnings statement discusses the scenario in which the company pays a cash dividend

Dee Private Limited had a net income of $ 260,000 for December 31, 20X8. Also, retained earnings at the beginning of the same year were $ 70,000. The company has 10000 shares of its common stock outstanding. The company pays a dividend of $1 on each of its shares.

Therefore, retained earnings can be calculated as –

Calculation:

Retained Earnings on December 31 20X8 = Retained Earnings at the beginning of year + Net Income – Cash Dividends Paid

= 260000 + 70000 – (10000 * $1)

= 260000 + 70000 – 10000

= 320000

Example #4 – Supreme Ltd

These examples of retained earnings statement discusses the scenario in which the company pays a stock dividend

Supreme Ltd retained earnings of $ 38000 on January 1, 20X5. The company reported a net income of $ 164000 for the year. The company, looking at good net income for the year, decided to pay a stock dividend of 10% on 10000 common shares when the shares were trading at $ 14 per share in the market.

Therefore, retained earnings can be calculated as –

Calculation:

Retained Earnings on December 31 20X5 = Retained Earnings on January 1, 20X5 + Net Income – Stock Dividends Paid

= 38000 + 164000 – (0.10 * 10000 * 14)

= 38000 + 164000 -14000

= $ 188,000

Frequently Asked Questions (FAQs)

Who utilizes the statement of retained earnings?

As internal stakeholders already have access to the retained earnings information, the statement of retained earnings is primarily prepared for external parties like investors and lenders. The net income paid out to investors as dividends are one piece of information in which external stakeholders are interested.

Is profit a part of the retained earnings?

Retained earnings are a business’s remaining earnings after paying all of its direct and indirect expenses, income taxes, and dividends to shareholders. The equity stake in the company can be used, for example, to fund marketing, R&D, and new machinery purchases.

What is the statement of retained earnings journal entry?

The date of the declaration of dividends by the board of directors of a corporation results in a journal entry that debits Retained Earnings and credits the current obligation Dividends Due. Therefore, retained Profits are decreased due to the issuance of cash dividends.

Recommended Articles

This has been a guide to what are Statement Of Retained Earnings Examples. Here, we explain the concept in detail along with examples. You may also find some useful articles here –