What is Accelerated Share Repurchase (Buyback)?

Accelerated share repurchase is the method adopted by the companies to repurchase their outstanding shares in large blocks from the investment bank. Further, the investment bank acquires shares from the clients of the company.

An accelerated share buyback, also known as a repurchase, means that the company purchases its shares to reduce the outstanding shares in the open market. The reduction in the number of shares outstanding in the market eliminates potential threats from the large shareholders. Instead, they want to increase their control to significant levels in the company. In addition, using a buyback, the company invests in itself, which improves the proportional share of earnings; this steps up a stock’s valuation.

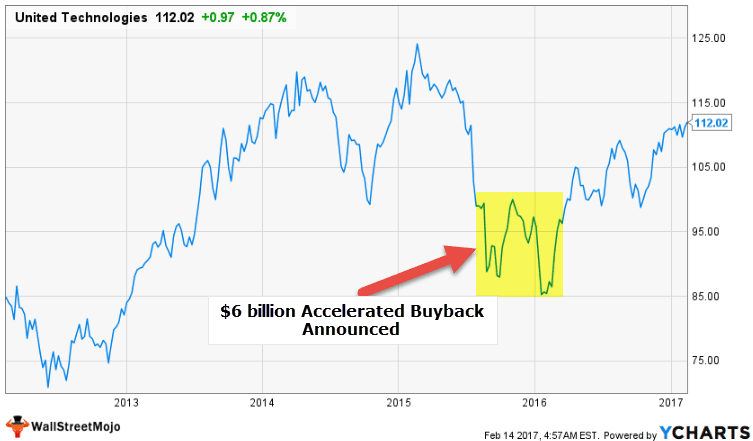

As the above snapshot shows, United Technologies entered into an “accelerated buyback” agreement with two banks (Deutsche Bank AG & J.P.Morgan Chase) to repurchase $6 billion worth of the company’s stock. Is Accelerated Buyback different from the Share Buyback from the open market?

How does Accelerated Buyback Work?

An “accelerated” buyback is also known as an accelerated share repurchase (ASR). Companies follow the practice of buying back shares of their stock from the market. Traditional buyback methods may take weeks or even months for the companies to purchase shares from the open market. But in the case of an accelerated plan, the companies ask the investment banks to short the full amount immediately. When the companies purchase the shares that the investment banks have shorted, it agrees to bear any losses on behalf of the bank. These shares, rather than being sold, are retired by the company. The buyback programs generally become a common phenomenon during the economic downturn when the stock prices fall to typically low values.

In an accelerated buyback, the company buys its shares from an investment bank, and the investment bank, in turn, borrows shares from the company’s clients. The investment banks to buy shares in the open market. Since the investment bank has sold the shares to the company to return the shares to its clients, they purchase the shares from the open market. At the end of the transaction, the company receives more shares than it initially had. While the returns on accelerated buybacks are positive, it is still less scalable compared to conventional open market repurchase operations.

The main benefit of accelerated buybacks is that it gives a big short term boost to share prices of the company. At the same time, the company’s earnings get elevated, and the profitability of the company increases on a per-share basis. The management also uses such a method to alter the earnings figure for reporting reasons and incentive remuneration. This procedure can also sometimes seem to be a strategic move by the companies to shift the risk of stock buybacks to the investment bank when the company senses that the shares are undervalued.

Shareholders, very often, prefer to share buyback programs, despite the risks involved because the ownership held by each investor expands when the number of outstanding shares floating in the market decreases. As a result, the company generates higher returns by making its shareholder value less dilute and spreading the same market cap over fewer shares than earlier. But realistically, in most cases, the ideal target is not achieved completely.

The share repurchase programs boost the earnings per share of the company and boost stock prices as well. Apart from boosting earnings per share, the buyback program reduces the value of the assets on the balance sheet. As a result, the shareholders’ funds, the return on assets, return on equity increase because the balance sheet has to remain balanced. Mostly, the repurchase programs target the short-sighted investors.

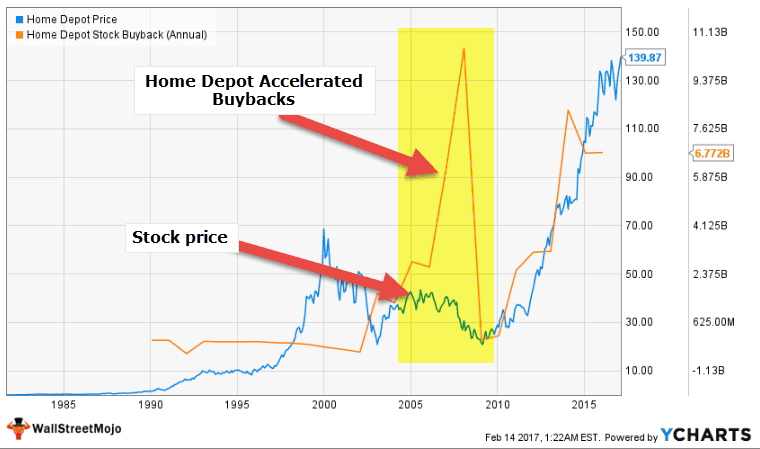

Home Depot Accelerated Share Repurchase Case Study

Since the company’s initial share repurchase program in fiscal 2002 through the end of fiscal 2015, the company has repurchased shares of its common stock, having a value of approximately $60.1 billion.

- In 2006-2007, Home Depot agreed to buy back 289.3 million shares of its common stock for $10.7 billion.

- In 2014-15, Home Depot buyback in excess of $7 billion worth of common stock.

As shown in the below graph, Home Depot prices have climbed from a low of approx. $20 per share in 2009 to a current high of $139 in 2017.

source: ycharts

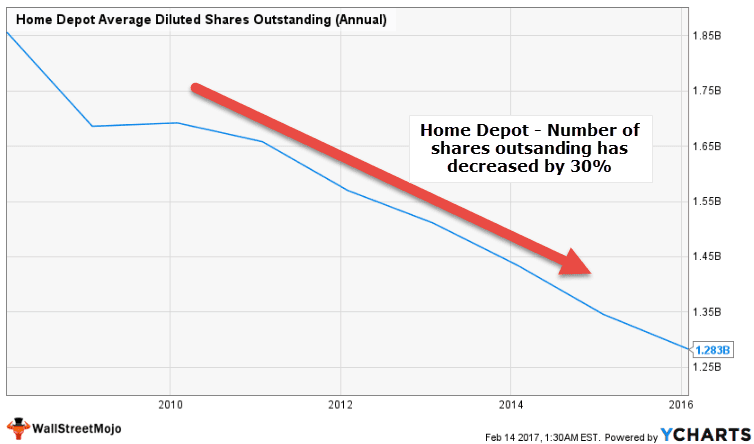

Home Depot Shares Oustanding

We note that Home Depots Average diluted shares outstanding decreased by more than 30% in the past 6-7 years. It is due to the buyback of shares.

source: ycharts

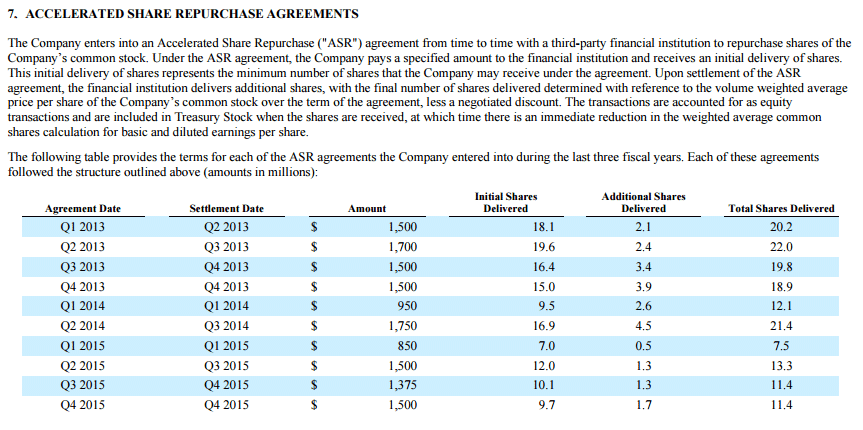

Sample Accelerated Share Repurchase Agreement – Home Depot

Below is a sample accelerated share repurchase agreement of Home Depot. This details the amount committed for buyback each quarter; initial shares delivered, additional shares delivered, and total shares.

source: Home Depot 10K Filings

United Technology Accelerated Buyback

At the end of 2015, United Technologies entered into accelerated share buyback agreements with Deutsche Bank AG and J.P.Morgan Chase, each delivering $3 billion worth of stock under this program.

source: ycharts

This accelerated buyback was a part of the $ 10 billion repurchases planned for 2016. As per Chief Executive Greg Hayes, this buyback takes advantage of the “big disconnect” between the company’s value and share price.

Advantages of Accelerated Share Repurchase

If the management of the company believes that the shares are undervalued, they repurchase the stocks and resell them when the price of the stock has been increased to reflect the precise value of the firm.

But for the meanwhile, the process of accelerated buybacks does serve some important purposes that are listed below:

- Accelerated share repurchase indicates to the investors that the company has enough money for economic crises or emergencies.

- The repurchase of shares increases the earnings per share (EPS), due to the reduction in the number of outstanding shares.

- Buybacks also counter unfavorable events such as hostile takeovers by preventing another firm from acquiring the company’s majority stock. The takeover target may buy back shares at a price, which is greater than the market value.

- Accelerated share repurchase stimulates the existing open market repurchase programs.

- Companies also consider buybacks for compensation; at times, the company’s employees and management are rewarded with stock rewards and options.

- Share repurchases help in avoiding the dilution of existing common shareholders.

- When the company spends the cash on hand on buying stocks from the market, it improves the overall performance metrics of the company.

- When companies carry out accelerated plans, they usually see that their stock price is higher. Yet, the investors are not cashing on it because of being bullish on the company. In this situation, an accelerated buyback can kick start another rally of the company’s stock.

- Companies can generally increase dividend payments after an accelerated buyback as there are fewer shares on which the company has to pay dividends.

Disadvantages of Accelerated Buy Backs

- Any share repurchase program serves as an easy cover-up for the poor financial status of the company. The investors get a false impression about the company’s financial situation as the statistics improve drastically.

- Often, it has been observed that the company insiders take advantage of the stock exchange programs while not diluting the actual EPS number, which is reported in the company’s books.

- During the accelerated programs, the share repurchases are often unable to be completed. It becomes difficult to know the real impact of the repurchase on the market price.

- When companies buy their stock, it also creates a negative reputation for the company in the market.

- The buying of its stock from the market also leads to poor utilization of the company’s capital because the company could as well employ the same dollars to fuel its business growth.

- Sometimes, buying the stock in the open market turns out to be a poor option for the companies. Because of flotation in the stock market, the repurchase doesn’t prove to be a good use of capital.

Accounting & legal requirements

In item 703 of Regulation S-K, it is stated that for all repurchases of equity-related securities, the following information must be reported by the company in the form of tables:

- Several shares are repurchased.

- The average share price paid for repurchasing;

- The number of shares whose repurchase has been completed under the publicly announced program;

- The maximum number of shares (or the approximate dollar value) that are remaining to be repurchased under the program;

Further, the company must disclose the above information for each month of the preceding fiscal quarter in the report of the next reporting period.

Additionally, for publicly announced programs, the SEC requires disclosure (in footnotes to the table mentioned above) of the following information:

- The announcement date.

- The approved number of shares or the amount by the board of directors;

- The date of the expiry of the program if any;

- Whether any program has expired during the last fiscal quarter;

- Whether there is any program has been terminated before expiration or which the issuer does not intend to continue.

Generally, these disclosures are also included in the liquidity and capital resource section of the companies’ “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which is an integral part of their annual and quarterly reports. Generally, these disclosures are also included in the liquidity and capital resource section of the companies’ “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which is an integral part of their annual and quarterly reports.

A company considering the share repurchase plan should consult outside counsel and other investment advisors. When carrying out the accelerated buyback programs, the companies should review the limitations or restrictions on repurchasing the shares, some of which are listed below:

- Tax and accounting statistics related to sharing repurchase

- Any application requirement related to the stock exchange on which the shares are listed

- Organizational documents, including certificate of incorporation and bylaws

- Relevant laws related to a state of incorporation

- Any agreements that may limit the ability to repurchase the company’s securities

Conclusion

Many companies will continue to face critical choices regarding how to best allocate their surplus cash. An increasing number of companies, over the years, have chosen to repurchase shares of their stock.

It is also important for a company to critically analyze the implications of share repurchases from a legal point of view, as discussed above in this article, so it can make an informed decision. Suppose a company elects to implement a repurchase program. In that case, it should take great care to ensure that the individuals and the institutions, who are tasked with implementing the program, understand the relevant contractual restrictions and statutory requirements as well as the necessary processes required to ensure compliance.