Part of our Shareholder Equity guide

What Is Paid in Capital?

Paid in Capital is the amount received by the company in exchange for the stock sold in the primary market, i.e., stock sold directly to the investors by the issuer, and not in the secondary market where investors sell their stock to other investors who can have both common and preferred stock.

Also known as contributed capital, this contribution marks the capital investors invest in the shares of a company. It is the par value of the shares that investors pay. When this par value figure exceeds and shareholders or investors pay more than the par value for the share, it becomes additional paid in capital.

Paid In Capital Explained

Paid in capital is the part of the subscribed share capital for which the consideration in cash or otherwise has been received. It is a part of Shareholders Equity in the balance sheet, which shows the number of funds that the stockholders have invested through the purchase of stock in the company.

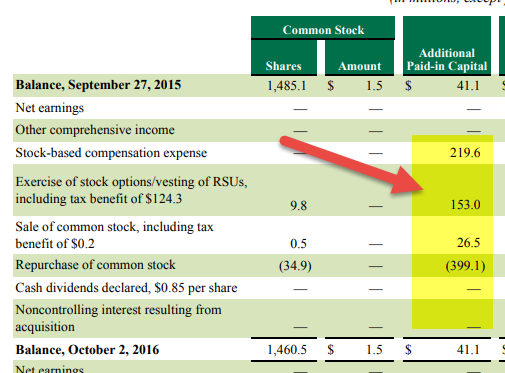

The paid-in capital on balance sheet is the aggregate amount invested by all the investors, not the particular investor. The image below shows how these capital investments are reflected on the balance sheet:

When the investor directly purchases the company shares, the company receives the fund as contributed capital. When the buyers buy the shares from the open market, then the amount of shares is directly received by the investor selling them. Paid in share capital is not an income generated by the company through its day-to-day operations, but actually, it is a fund raised by the company through selling its equity shares.

- The capital is paid in during the preferred stock or common stock issuance by the investor. The shareholders are considered the owner of the company. Their money is invested in terms of share capital and return; they get dividends (share of profit in the company)

- The shares issued by the company always have a par value. It is fixed when the company originally issues the shares in an IPO (Initial Public Offer). It is the original cost of the stock shown in the certificate. Market value is different from par value. Market value is determined by the buying and selling of the business in the open market. In the balance sheet, the shares are always shown at their par value or face value.

- There are mainly two components of the paid-in share capital. The first one is the stated capital, which is reported in the balance sheet at the par (face) value, and the other is APIC, which amounts to the money received by the company above its par value. APIC calculation often reflects the significant part of the shareholders’ equity before the retained earnings Start to accumulate, and it is a secure layer in case the retained earnings are a deficit.

Factors

There are determinants that significantly affect the amount that one pays to own the shares of a company. Let us have a look at the factors in detail below:

source: Starbucks SEC Filings

#1 – Issuance of shares

At the time of incorporation of the company, promoters and investors purchase the shares. Firstly, the authorized share capital is fixed by the company beyond which the company cannot issue the shares in the market. The company fixes the par value or the face value of each share. So initially, the balance sheet issued, and paid-in capital is recorded at the par value. Afterward, let’s say a company wants to raise funds by issuing more share capital. I.e., funds are required for any capital expenditure or other large business transactions. Then, the company will issue more share capital, and the investors will pay up the amount. After the investor has paid the amount, a new journal entry will be passed by recording the increase in the paid-in capital of the company. Stock prices in the secondary market don’t affect the amount of paid-in calculation in the balance sheet.

#2 – Bonus Shares

A bonus issue means an issue of free additional shares to the company’s existing shareholders. Bonus shares can be issued out of free reserves, securities premium, or capital redemption reserve accounts. With the issuance of bonus shares, the amount in the paid-in capital is increased, and the free reserves are decreased. Although it doesn’t affect the total shareholders’ equity, it will individually affect the paid-in capital calculations and free reserves.

#3 – Buyback of shares

The buyback of shares by the company also affects the paid-in capital. The shares bought back by the company are shown in the shareholders’ equity at the cost at which they are purchased in the name of treasury stock. Suppose the company sells the treasury stock above the purchase cost. In that case, the profit from the sale of treasury stock is credited in the paid-in capital calculation from treasury stock under the head shareholder’s equity. If the company sells the share at a price below its purchase cost, then the loss from the sale of treasury shares is deducted from the company’s Retained earnings. And if the company sells the treasury stock at the purchase cost only, then the shareholders’ equity will be restored to its pre-share-buyback level.

#4- The Retirement of treasury stock

The retirement of treasury stock is also an option for the company if it doesn’t want to reissue it. Due to the retirement of treasury stock, the whole balance applicable to the number of retired shares gets reduced. Or the balance from the paid-in capital calculation at par value and the balance in additional share capital gets reduced accordingly depending on the number of retired treasury shares.

#5 – Issuance of preferred shares

Sometimes management prefers to issue different classes of preferred shares instead of the common stock because of the expected negative reaction from the market by the company if it issues the share, as that issuance may lead to the dilution of the value of equity. It will increase the total balance as the issuance of the new preferred shares will increase the paid-in capital as excess value is recorded.

Formula

The mathematical equation that helps in calculating the paid-in or paid-up capital is mentioned below:

Paid in Capital Calculation = Common Stock + Additional Paid-in Capital (APIC)

Examples

Let us consider the following instances to understand the paid in capital definition better and also check how to calculate it:

Example 1

Let’s take an example where a company named XYZ Ltd. Issues shares worth $20 million, having a face value of $20 per share. The company issues the shares at $30 per share, which shows that $10 is the premium on the issue of shares. Now the amount received is $600 million. It is bifurcated as

- Common Stock = $400 million ($20 million *$20)

- Paid-in capital Calculation = $200 million ($20 million *10)

- Additional share capital can be shown as the contributed surplus or can be reported differently under the head shareholders’ equity.

Example 2

As per September 2023 report, World Bank specified it capital requirement, given the need to organize effective campaigns to encourage climate adaption, resilience, and mitigation. According to the report, the World Bank must receive funds to finance the related annual spending worth $3 trillion by 2030. The banking sector ace stated that the paid-in capital of $22.6 billion that the World Bank’s International Bank for Reconstruction and Development receives is not sufficient enough to increase its lending capacity for the purposes. Hence, it would require more capital investments from different sources.

Paid-in Capital vs Retained Earnings

Paid-in capital and retained earnings are two widely used terms in the corporate sector. While the former is the investment that firms receive, the latter is what they earn. Let us look at the differences between the terms in brief below:

- Paid-in or paid-up capital is the amount invested to own shares of a stock of a company. On the contrary, retained earnings is the net income of the firm, which it is left with after the deductions and liabilities are met.

- Paid-up capital is what shareholders provide to the firms with which they grow further. Retained earnings is the company’s accumulated amount from the gross profit, which is used for reinvestment without the firms having to ask for the money from third-party entities.

- The former cannot have a negative value, while the latter can be negative as well.

- Paid-in capital is the direct investment that investors make and receive dividends in return for the same, while retained earnings give companies an opportunity to not ask for investments from shareholders and utilize their net income, which is their own money that they are free to reinvest for their own growth. Retained earnings cannot be used to distribute dividends. They are the amount left with the business after all financial obligations are borne.

Recommended Articles

For more on Shareholder Equity, explore these related articles from our Shareholder Equity guide.