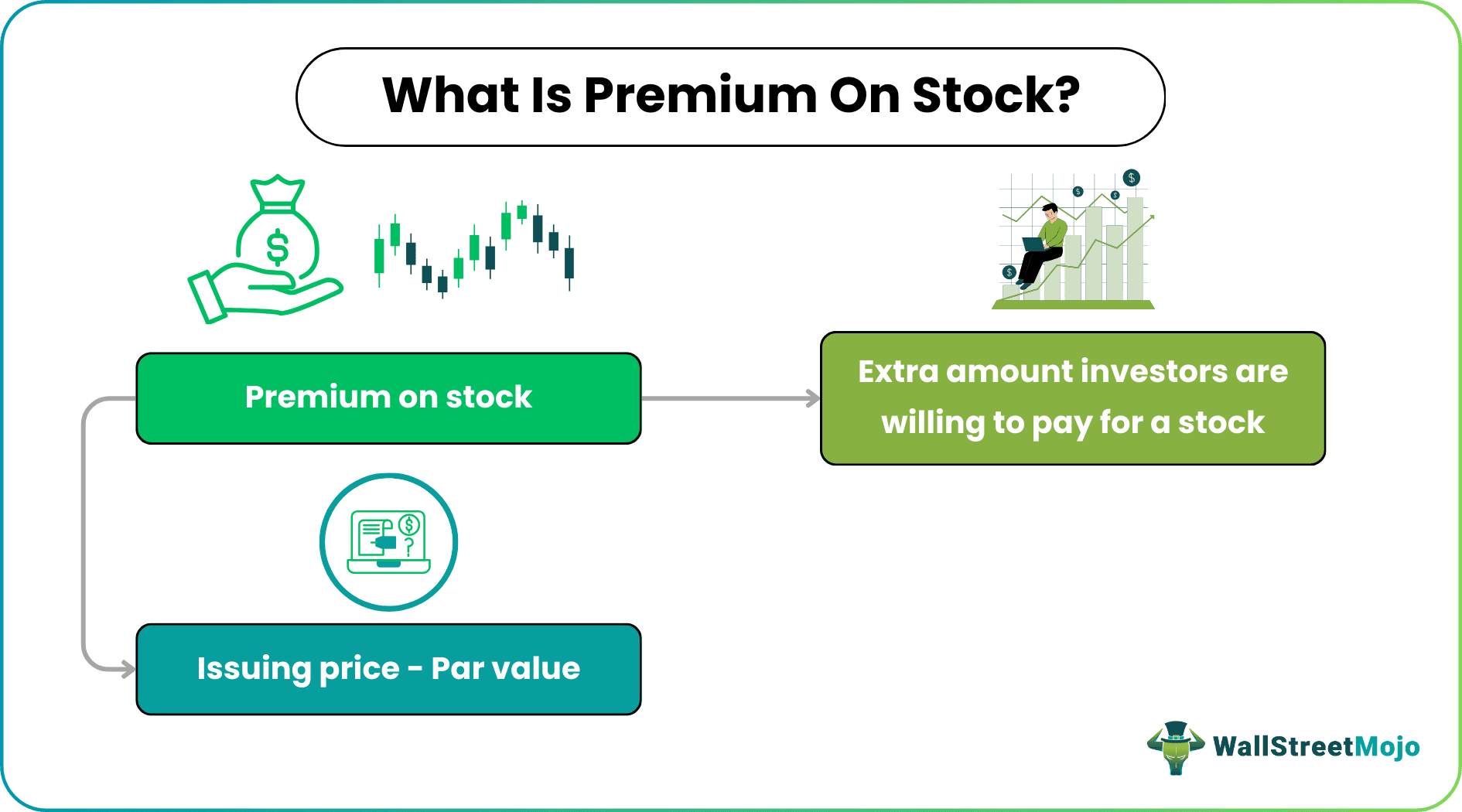

What is Premium on Common Stock?

Premium on Stock is defined as the amount of extra money which the company’s investors are ready to pay to the company for the purchase of the company’s stock over its par value and is calculated by subtracting the par value of the share issued from the issuing price.

A premium on stock highlights the number of money investors are willing to pay in addition to the stock’s par value. It is an indication of the share value and the expectations from the market for the specific company. The firm should either be exceeding market expectations or keep investors interested in the company’s prospects, making them pay more than the par value of the share.

- The premium on stock is calculated by subtracting the par value of each issued share from the issuance price, representing the extra amount investors are willing to pay the company for its shares beyond their par value.

- It must be utilized exclusively for this designated purpose in accordance with various state regulations.

- The stock premium is allocated to issue fully paid bonus shares to existing shareholders, and it cannot be allocated for debentures, upfront expenses, or exceeding the company’s authorized share limit.

Premium on Stock Explained

Premium on stock is the additional money that investors agree to pay to own a stock. This premium price is calculated by subtracting the lower par value from the higher issuing price. The result obtained is the final extra amount that investors have to pay for the stock they prefer.

The investors agree to pay this premium amount when they could clearly see the progressive growth of the company to which the stock belongs. Paying this extra amount for the stocks ensures more returns or profits for the investors. Hence, they don’t hesitate to invest extra in them.

Example

Let us consider a simple example to understand this concept better:

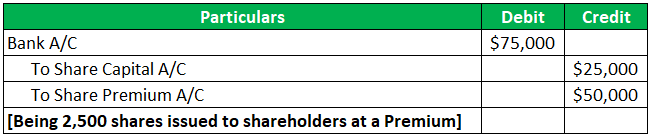

Say Mr. Frank is running a restaurant with four more shareholders. Mr. Frank wants to issue an additional 2,500 shares of $10 par stock to new investors to raise additional capital for expansionary projects. As the restaurant is performing exceptionally well, and the investors recognize future potential, the investors are willing to pay $30 for every share. In this case, the difference of $20 is the premium amount on the stock.

Accounting

The accounting for the stock premium is quite simple. The common stock account is used for recording the par value of the stock issued, and a separate account termed ‘paid-in capital over par’ is used to record the premium. This is an equity account representing the number of money investors have contributed to the firm in addition to the stock’s par value. The journal entries for the same can be written as follows by extending the above example with a necessary explanation:

If additional stock is issued at a premium, the stock issuance is recorded by debiting cash for $75,000 [2,500 shares *$10 par value]; crediting common stock for $25,000 [2,500 shares * $10 par value]. Further crediting the balance of $50,000 [$75,000 – $25,000] i.e. paid-in capital in excess of base value of $25,000. One can observe that common stock is only for recording the par value of the newly issued shares. Additionally, the paid-in capital account records the entire premium the new investors are willing to pay for the shares.

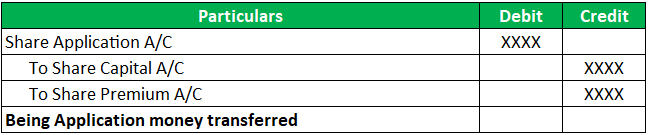

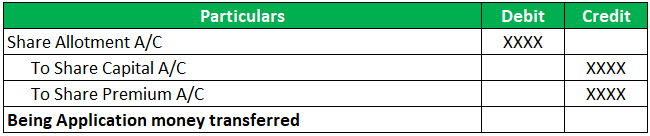

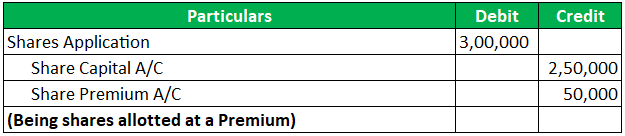

The entries have a different recording treatment when the securities premium amount is received with Application money and Allotment money.

If the premium money is received with application money, it’s not credited directly to the Securities Premium Account. The application is received, but as there are possibilities of rejection, one must wait until the application is accepted and finalized. The entries would be:

There will also be times when the stock premium is collected with the allotment money. The journal entries would be:

Further, upon transfer of application money, the entry would be

An important point to be noted here is that if any advance amount was received during the application, such money should be adjusted towards the share allotment account. However, firstly the advance money should be adjusted against the nominal value of shares, and if any balance remains, it shall be adjusted against the securities premium account.

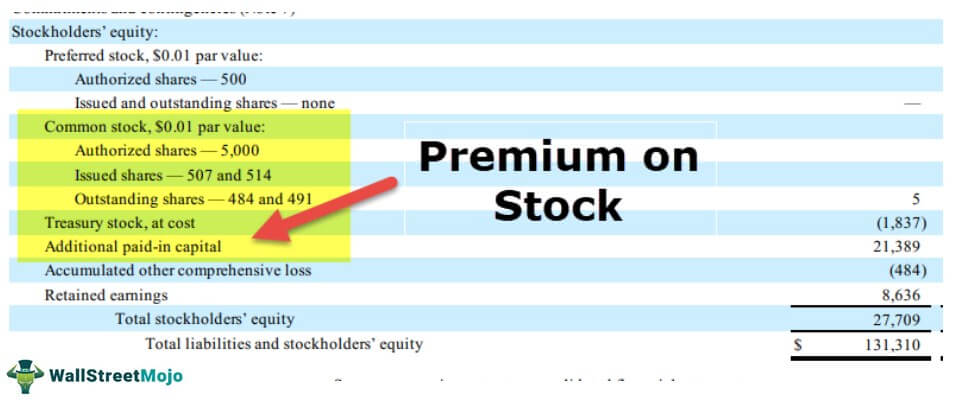

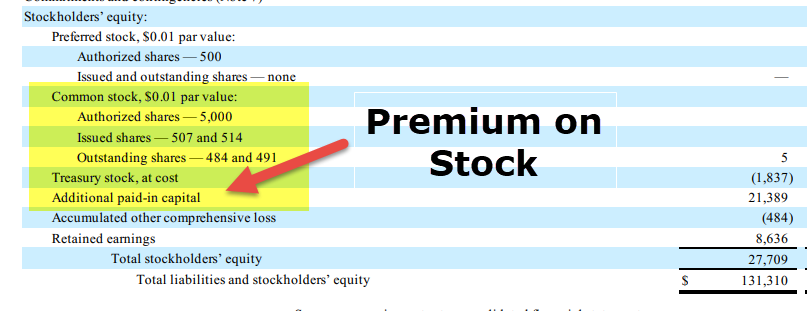

The account is listed on the equity section of the balance sheet and just below the common stock account.

- Every firm should strictly note that the stock premium is a non-distributable reserve. It can be used exclusively for a purpose as defined in the company’s by-laws. It cannot be considered for any other purpose.

- Stock premium should be used for paying equity-related expenses such as Underwriter’s fees.

- Firms are not permitted to utilize the share premium for the dividend payment to shareholders or for setting off operating losses.

- It could also be used for bonus issues to the stakeholders. The costs and expenses associated with issuing new shares can also be adjusted from the share premium.

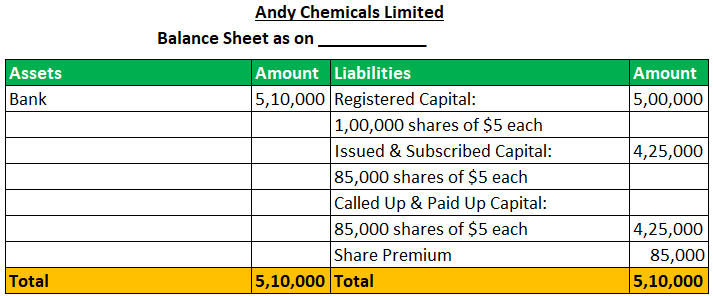

Let us look at an extensive example with its impact on both the Journal and the Balance Sheet:

Andy Chemicals Ltd. had an authorized capital of $10,00,000 divided into 1,00,000 shares of $10 each. They issued 35,000 shares to the directors and 50,000 shares to the general public at a premium of $1 per share. Subscriptions were received completely, and these shares were allotted.

Securities Premium Account

This Stock premium account has been created for specific purposes. Various laws across the state that this account should only be used for such a specific purpose and no other activity.

The account is used for the following purposes:

- Issuance of fully paid-up bonus shares to the existing stakeholders. It should be noted that this cannot exceed the limit of the unissued share capital of the firm.

- Writing of shares and debentures, e.g., commission paid or discount given on the issue of shares.

- Usage for the writing of any preliminary expenses of the company;

- The balance could also be used in providing a premium payable on debenture redemption of the preference share of the company.

- Buy-back of its shares.

- It should not be used for dividend payments.

Frequently Asked Questions (FAQs)

1. What role does premium on stocks play in initial public offerings (IPOs)?

In IPOs, the premium can indicate market demand and investor perception of the company’s value. A higher premium might signify strong investor interest, while a lower premium could suggest cautious sentiment.

2. Can the premium on stock change over time?

Yes, the premium on stock can change based on market conditions, company performance, industry trends, and investor sentiment. It may increase or decrease as these factors evolve.

3. How does a premium on stock affect a company’s cost of equity?

A higher premium can result in a higher cost of equity for a company, as investors would expect higher returns to justify the premium paid for the stock.

4. How does the premium on stocks relate to stock splits or reverse splits?

The premium might remain relatively constant during a stock split as the par value is adjusted. In a reverse split, where several shares are consolidated into one, the premium may increase due to the reduction in outstanding shares.

Recommended Articles

This article has been a guide to what is Premium on Stock. Here, we explain the concept with an example, accounting process, and securities premium account. You can learn more about accounting from the following articles –