Part of our Accounting Concepts guide

What Is Faithful Representation?

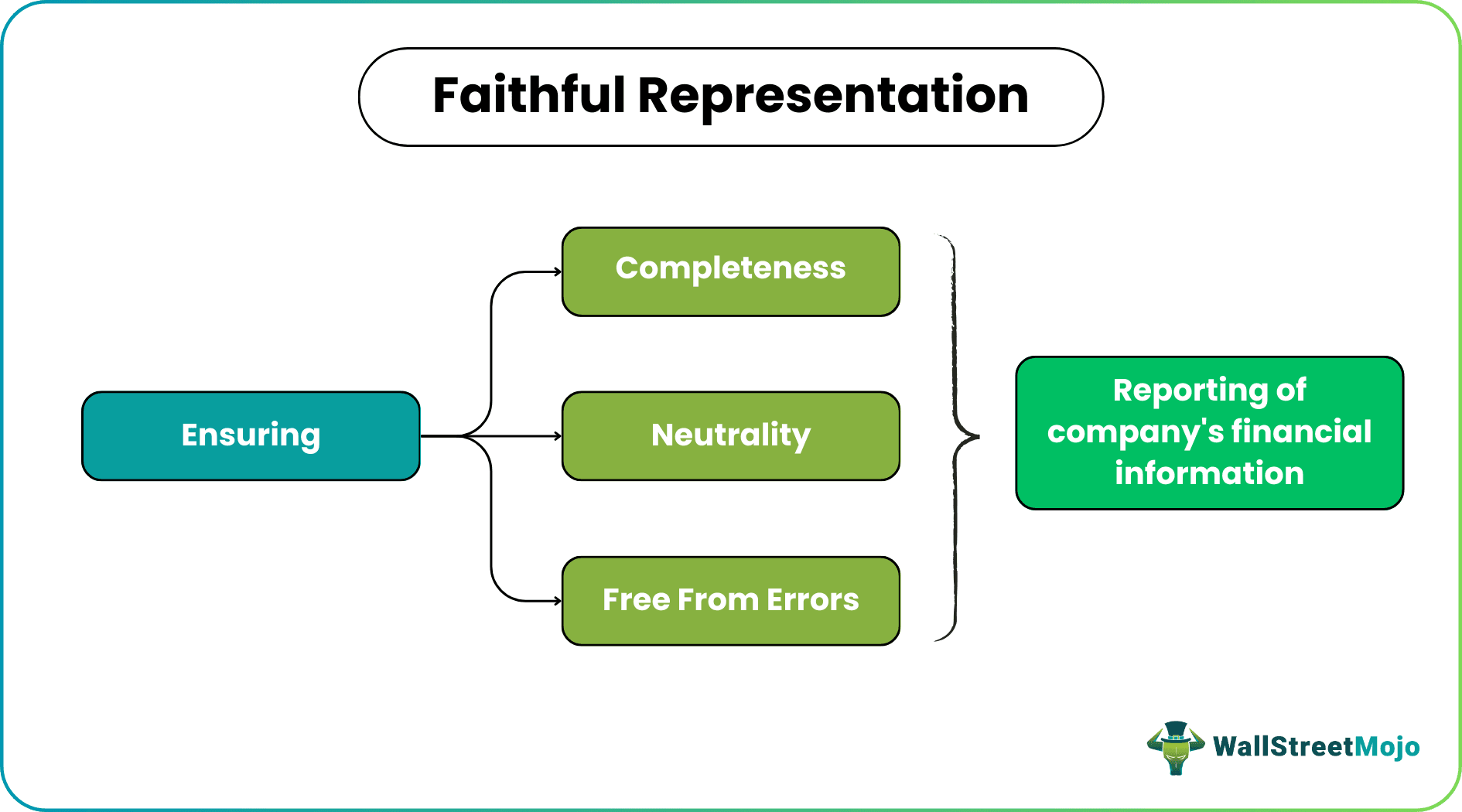

Faithful Representation refers to an accounting concept that emphasizes accurate reporting of a company’s actual financial position in compliance with the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB). Thus, the firm’s financial statements and reports should be unbiased, complete, and independent from material errors.

It is a critical qualitative characteristic that makes the business’s financial information valuable for the company’s investors, creditors, shareholders, regulators, and other parties for critical decision-making. This is because it brings out an accurate picture of the firm’s financial performance and condition. Moreover, it applies to all financial statements, including balance sheets and cash flow statements.

- Faithful representation emphasizes reporting the true and accurate financial information of a company.

- The three elementary components of this accounting concept are complete, neutral, and error-free financial reporting.

- Such attributes are essential to make the company’s financial insights reliable and valuable for its stakeholders, investors, managers, creditors, and other parties.

- The reliability of the firm’s financial statements is enhanced through factors like verifiability, understanding, comparability, and timeliness.

Faithful Representation Explained

Faithful representation is a critical aspect in ensuring that the firm’s financial reporting is trustworthy and includes all the facts related to a company’s performance and condition. It serves as a basis for making informed investing, lending, and strategic decisions for the business. Moreover, the financial insights should be verifiable, comparable, and understandable at the same time. It even helps the firm comply with tax laws and reporting regulations while improving its reputation due to its financial transparency to various stakeholders.

Although faithful representation in accounting is crucial for businesses, the accounting team faces immense challenges in ensuring the trustworthiness of the enterprise’s financial statements. The foremost difficulty arises in the selection of suitable accounting policies that align with the substance over form objective of the company. Moreover, some events or transactions are intricate and complex to report in the books. Indeed, it is again challenging to maintain comprehensive and real-time information in businesses where a lot of small transactions take place daily. To deal with such issues, the accounting team should strictly adhere to the principles and guidelines of the company.

Characteristics

The faithful representation in accounting can be achieved when the company’s financial information demonstrates the following attributes:

- Completeness: The financial statements are supported by disclosures, and the transactions, conditions, and events cover all the related facts that reflect the firm’s financial performance and position.

- Neutrality: It is equally necessary to maintain the objectivity of the financial reports by ensuring that these are unbiased and not influenced by any person or group for deriving personal benefits.

- Free From Errors: Simultaneously, the books of accounts should be accurate and should not have any material errors or misstatements that would otherwise impact the viability of such information.

Examples

The reliability of a company’s financial information can be better understood with the help of the following real-world examples:

Example #1

Suppose XYZ Ltd. reported its financial information for the accounting period ending on December 31, 2023. However, the following faithful representation issues were found during the audit:

- Completeness: The transactions worth $1,500 for goods sold in cash (as per the cash receipts) should have been accounted for in the income statement.

- Neutrality: A sleeping partner in the business, John, has drawn a $6,000 salary for the company’s active management.

- Free From Errors: The electricity charges for October 2023 were recorded twice in the books, elevating the expenses by $2,700.

Example #2

The WorldCom scandal involving $3.85 billion in accounting irregularities shook investors and the public, leading to CFO Scott Sullivan’s dismissal and SEC fraud charges. The company wrongly booked line costs as capital expenditures, artificially inflating profits. However, some of the red flags, like consistent, smooth earnings growth, should prompt investor skepticism.

While some call for changes to Generally Accepted Accounting Principles (GAAP), experts emphasize the need for more vigorous enforcement and governance to prevent future scandals. CEO certification of financial statements is suggested but faces feasibility challenges. Auditing reforms are crucial, as auditors missed systematic misclassifications at WorldCom. Overall, the scandal emphasizes the importance of faithful representation, transparency, accountability, and rigorous oversight in corporate governance and financial reporting.

Importance

Faithful representation in accounting serves as a critical requirement when it comes to financial reporting and taxation. Let us discuss the various reasons for its significance:

- Reflects True Financial Position: The faithful representation of the company’s finances facilitates the business to represent its fair financial condition and performance to the stockholders, investors, creditors, regulators, and other associates.

- Fosters Transparency: The reliable reporting of a business’s financial information can enhance the transparent communication and accountability among the various stakeholders of the company.

- Ensures Compliance with Accounting Standards: The companies that maintain accuracy and reliability in their financial reporting are more compliant with the accounting standards of IASB and FASB.

- Supports Financial Analysis: A faithfully represented accounting statement can help stakeholders perform various financial analyses, including ratio analysis, trend analysis, and other performance analyses.

- Empowers Decision-Making: The financial reports of a company should be reliable as they are crucial for decision-making by internal and external parties such as managers, directors, investors, lenders, regulators, and shareholders.

- Enables Comparability: When the company follows a consistent practice of fairly representing its financial information, it aids in the comparison of business performance across different accounting periods and with the financial position of its competitors.

- Ensures Verifiability and Auditing: The regulatory bodies and tax authorities can cross-verify a firm’s financial transactions and events with supporting documents.

- Builds Stakeholders’ Trust: As the business accurately reports its financial insights to its stakeholders, they develop confidence and trust in the company and its management.

Faithful Representation vs Relevance

Relevance and faithful representation are two inevitable qualitative attributes of financial reporting of companies. However, given below are some of the primary differences between these two accounting concepts:

| Basis | Faithful Representation | Relevance |

|---|---|---|

| Definition | It is the qualitative aspect that determines the accuracy and reliability of a company’s financial reports. | It is the qualitative attribute that depicts the usefulness of the published financial information for decision-making. |

| Characteristics | Complete, neutral, and error-free | Predictive value, conformity value, and materiality |

| Depicts | Reliability of financial information | The usefulness of financial information |

| Selection Factors | How consistent is the substance with the related assets and liabilities? | The features of assets and liabilities and the manner in which they facilitate future cash flows |

Frequently Asked Questions (FAQs)

How to show faithful representation?

A company can check the reliability of its financial statements by ensuring that it accounts for all the transactions without any bias, material errors, or misstatements. Moreover, the transactions must have relevant supporting documents and disclosures for factual evidence.

What are the contributory factors towards faithful representation?

As per the International Accounting Standards Board (IASB), four factors facilitate the faithful representation of financial reports: verifiability, comparability, understandability, and timeliness.

What is the difference between reliability and faithful representation?

Reliability in accounting refers to the accuracy and dependability of financial information, ensuring that it is free from material errors and bias. On the other hand, faithful representation is a broader concept encompassing completeness, neutrality, and freedom from errors, emphasizing the true reflection of a company’s financial position and performance. While reliability focuses on the accuracy of data, faithful representation extends to the overall integrity and transparency of financial reporting.

Recommended Articles

This article has been a guide to what is Faithful Representation. We explain its examples, characteristics, comparison with relevance, and importance. You may also find some useful articles here –

Recommended Articles

Continue with these closely related articles from the same guide.