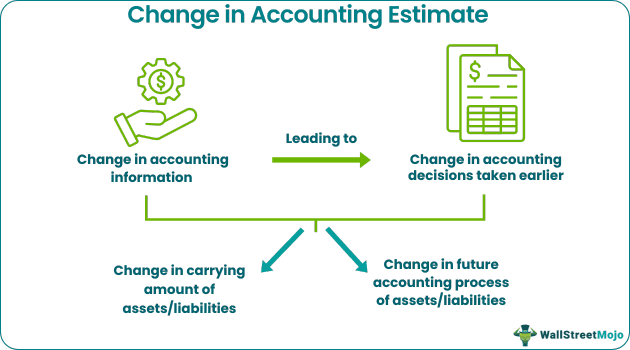

What Is The Change In Accounting Estimate?

A change in accounting estimate occurs when there is the appearance of new information, which replaces the current data based on which the company had taken an earlier decision, resulting in two things – changing the carrying amount of an existing asset or liability and alteration of subsequent accounting for recognition of future assets and liabilities.

There are different and less stringent compliances regarding changes in accounting estimates over the change in principle. The latter needs to be changed retrospectively, whereas the former to be prospective. In some cases, one can find that the change in accounting principle may lead to a change in accounting estimate. In such cases, reporting and disclosure requirements of both variation in principle and estimate should be followed.

Change In Accounting Estimate Explained

The process of changes in accounting estimate is the adjustment that is made in the carrying amount of liabilities and assets or any other related expense. This decision results from evaluation and assessment of the current condition and the expected future obligations and benefits that the business expects to get from these assets and liabilities.

This is due to some new development or new information in the accounting field. Therefore, they are not referred to as correction of any accounting error. The business develops of designs new estimates in order to achieve the goal that it needs to meet through the accounting policies which are reflected as change in accounting estimate disclosure in the financial statements.

Thus, the process includes two things:

- Selection of a method of measurement or valuation technique which may be used for measuring the loss allowances for any credit loss expectation.

- Selection of input that will be used during application of the selected measuring process. For instance, while determining the amount of provision, the exected outflow of cash needs to be determined.

So, change in estimates can be referred to as the change in measurement methods or inputs as given in the cases above.

Prospective Or Retrospective?

Any changes made in the accounting estimates arise due to new information of developments, which are not considered as errors. However, the effect of such changes are recognized in accounting prospectively and they are included in the income statement.

The treatment of change in accounting estimate is done in the period when the change takes place, provided the change affects the financial statement of that accounting period only. But if the change affects both current and future accounting periods, then the profit and loss statement of both the periods will be affected.

The method of prospective change means the modification is applied for conditions, events or transactions starting from the date of change in estimate. The effect related to the present period is recognized in the current income statements and the effect on present and future period will influence both the income statements.

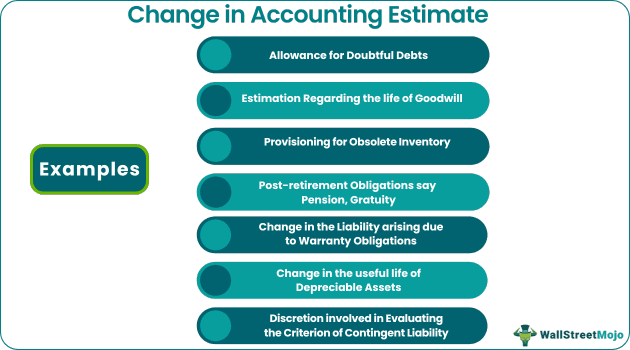

Examples

Let us understand the concept with the help of some suitable examples.

Example #1

While accounting for the transactions, we need to consider the number of estimates or use our prudence or judgment. In some cases, these estimates can prove inappropriate, as the basis on which we had taken our assumption has changed. Keeping our books aligned with the subsequent changes warrants a change in accounting estimate.

In the following situation, we use our prudence.

- Bad Debt Reserve

- Provisioning for Obsolete inventory

- Change in the useful life of depreciable assets

- Change in the liability arising due to warranty obligations

- Estimation regarding the life of Goodwill

- Discretion is involved in evaluating the criterion of contingent liability

- Post-retirement obligations say pension and gratuity.

It is not an exhaustive list, and it would expand depending upon the sector in which the business is involved.

Example #2

ACE Inc bought a chemical plant amounting to $400 mn on January 1, 2016. At the time of recognition of the plant as a fixed asset, the company estimated its useful life to be ten years and salvage value to $80 mn.

The company used the Straight Line Method for depreciating the assets.

On January 1, 2019, the company learnt that the salvage value of the plant has decreased to $60 mn and life to 8 years due to new technology being introduced in the market.

Calculation

- From 2016 to 2018, the company would have recorded depreciation of $32 mn per annum, {(400-80)/10}.

- As of January 1, 2019, the book value would be $336 mn. ($400-$32-$32).

- Due to new technology in the market,

- Now the revised depreciation would be $35 mn {(336-60)}/8}.

Please note that the change in estimate affects subsequent periods only and not the historical book values.

Is A Change In Accounting Estimate Equivalent To Error?

An error happens unintentionally, and a change in estimates would not fall under this category.

Estimates are based on certain assumptions and theories, and when it changes according to the scenario, we need to alter the basis. It does not tantamount to error or omission.

Once an error is identified, we need to assess the appropriate means to rectify the error.

There are three things to be considered when we identify the omission in the financial statements –

- Determining if the error exists and it is not changed in the accounting estimate or principle.

- Assessing the materiality of the error, keeping in mind the revenue or turnover of the company;

- Reporting an error in the previously issued financial statements;

So, there is a thin difference between error and treatment of change in accounting estimate. It would involve the judgment and experience of the management involved.

Internal Controls

Financial statement risks related to changes in accounting estimates must be adequately mitigated by the proper internal controls placed by the management.

Management should understand the significant assumptions and methods used and ensure that the controls timely identify unnecessary changes to prevent harm to stakeholders’ interests.

A company should try the following to ensure stringent control on changes in the accounting estimates.

- Communication flow should be proper and flawless.

- A qualified person should be handed this task for alteration whenever required.

- A comparison between pre and post-change of the estimate should be listed, which would help the stakeholders to make informed decisions.

How Should An Investor Look At Estimates?

An investor needs to ensure that the company’s financial position is free from bias, errors, and wrong assumptions.

He should be able to ask the following questions while deciding to invest in the company –

- Whether the rate of depreciation, if taken more than the permissible limit of the law, in line with the usage of the assets?

- Is the provision of bad debts inflated or deflated to temper the company’s profits?

- Is the useful life of the fixed asset proper?

Though it may seem difficult for an investor to deep-dive into such types of questions, the actual position of the company lies in this pothole only.

Disclosure

The entity should disclose the following in the financial statements-

- Nature and amount of change in an accounting estimate that has an effect in the current period or has an impact on the future periods.

- If it is impracticable to determine the effect in future periods, then proper change in accounting estimate disclosure should be provided in the notes to accounts.

Change In Accounting Estimate Vs Change In Accounting Policy

A change in accounting policy governs how the financial information would be calculated, whereas a change in accounting estimate is a change in the valuation of financial information.

The best example of a change in accounting policy is the inventory valuation. The company is using First in, First Out (FIFO) inventory method as the valuation of the stock. Due to the law’s requirement, now the company has to use the Last In, First Out (LIFO) method as the stock valuation.

In the accounting estimate, the company was using the Straight Line Method to depreciate the asset, and it has estimated salvage value of the asset as $3,000. But due to changes in the market scenario, now the company can fetch only $1,000 of its assets.

Due to this, the depreciable value would alter, resulting in a change in the accounting estimate. If the company had changed the Straight Line Method to Written Down Value, it would be classified as a change in accounting policy.

Recommended Articles

This has been a guide to Change in Accounting estimates. Here we discuss Examples, Internal controls, and disclosure of Changes in Accounting estimates. We also discuss how investors look at estimates. You can learn more about financing from the following articles –