Part of our Accounting Concepts guide

What Is Expense Recognition Principle?

→ Explore all 59 Expense Recognition articles

Expenses recognition principle primarily refers to the accounting principle that follows the accrual basis concept, where expenses are recognized and matched in the books in the same period as revenues. It reflects when the expenses incurred will appear in the company’s financial statements.

This principle provides guidance to the management regarding how and when the revenue and expenses are to be matched. Thus, it clarifies the time and method of the matching process, which primarily differentiates the accrual basis from the cash basis of accounting. This affects the tax deductions obtained by the company later on.

Expense Recognition Principle Explained

The expense recognition principle, which is also termed matching principle, acts as a guidance in the accounting process, which identifies how the expense will be reported in the financial statement of the company. It primarily follows the concept of accrual basis of accounting, which is commonly used in the organizations.

As per the accrual basis, the expenses are recognised as and when they take place, not when the cash is paid or received. It also takes into account the fact that the expense will be recognised when the revenue for the same transaction will be identified. This will provide a clear and transparent view of the profit-making capacity of the business.

While recognizing the expenses as per the matching expense recognition principle, the accounting periods are assumed to be annual, quarterly or monthly, as per the process followed by the entity. Based on these periodicities, expenses are incurred.

However, it is important that the organization should follow the process consistently and apply the principle for each and every transaction, so that there is compatibility and authenticity in the financial statements and reports that are presented to the stakeholders for better clarity regarding the operations of the company.

Types

There are two types of matching expense recognition principle –

- Accrual Basis – Under this accrual principle expense will be recognized in the books as and when it is matched with the revenue. For example, telephone bills per month are $500 paid for 13 months. Under this method, $6000 for 12 months will consider this year’s rest of $500 for one month next year.

- Cash Basis – Under this cash basis method, the expense will be recognized in the books when it is paid or received. Consider the above example; under this method, a full $6500 will be recognized in the same year when it is paid.

Examples

Let’s understand this concept with the help of the following example.

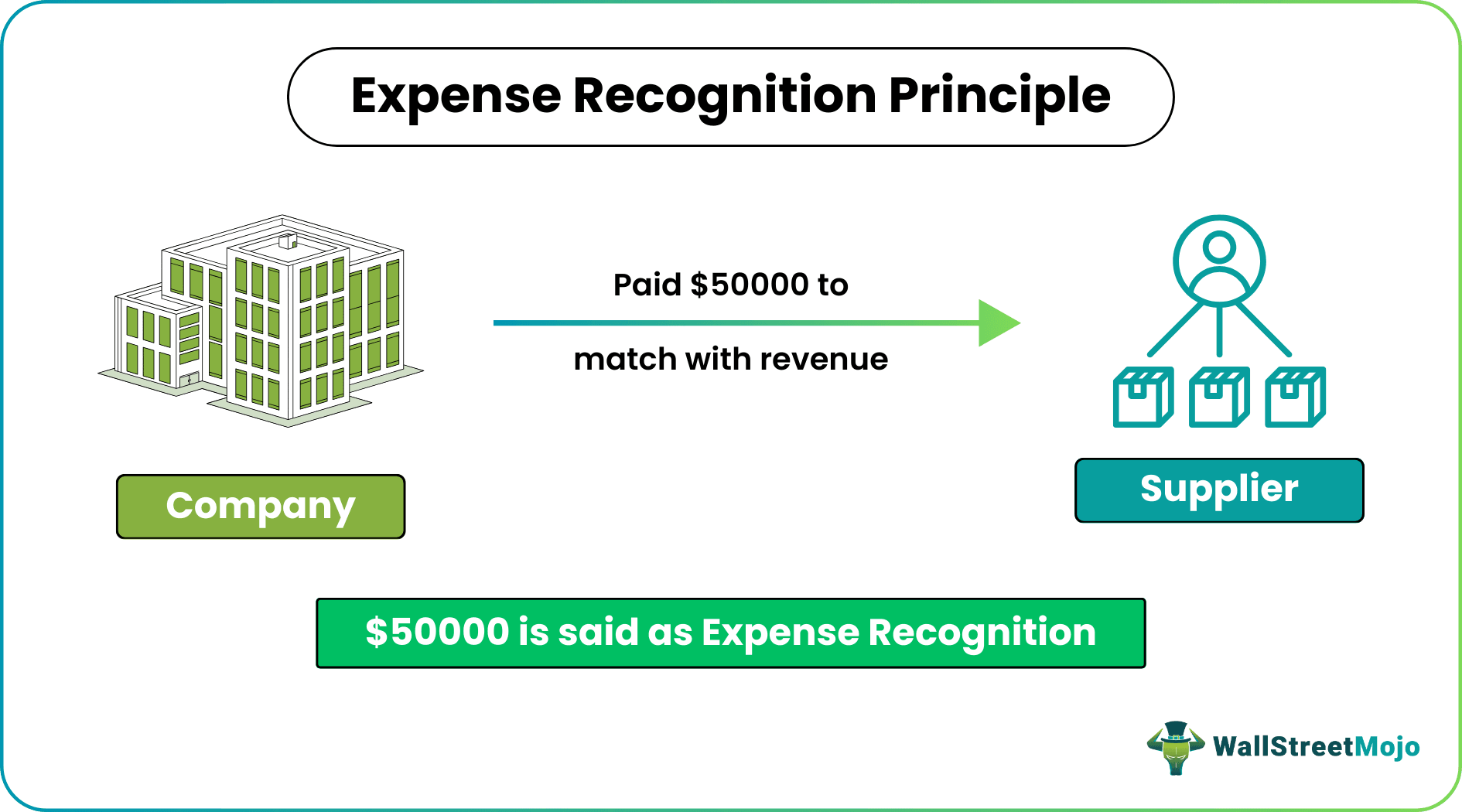

Example #1

Company X paid $ 50000 to the supplier for material, which he will sell next month for $ 80000. In this case, X will recognize $ 50000 as expenses in the next month to match with revenue; otherwise, the current month’s expenses will be high, and the tax amount will be high in the next month. It is also done for income tax. Without this principle, income tax in the current month will be less than next month.

Example #2

In some cases, matching revenue concept is not possible; therefore, expenses recognized in the period for which they are related, for example, salary, rent, electricity, administrative expenses.

Suppose company X paid 13-month rent amounting to $ 13000, and per month rent is $ 1000.

Journal entry in 1 year-

| Particulars | Debit | Credit |

|---|---|---|

| Rent A/C………..Dr | $12,000 | |

| Advance Rent A/C | $1,000 | |

| To Bank | $13,000 |

In the below scenario, X will recognize $12000 as rent for this year, and the balance of $1000 will recognize the expense in the next year, and It will show rent under advances.

Journal Entry Next Year

| Particulars | Debit | Credit |

|---|---|---|

| Rent A/C……..Dr | $1,000 | |

| To Advance Rent A/C | $1,000 |

This year’s rent expense adjusted with advance rent.

Advantages

Every accounting concept has its own advantage and disadvantage. Therefore it is important to understand the same for this concept of expense recognition principle in accounting. Let us study the advantages first.

- During the Audit of financial statement, if the Auditor finds books of the company’s accounts have not followed the accrual concept, then the Auditor may qualify the Audit report. For example, as per the standard on Audit, the Auditor has to check whether the company is following the accrual concept or not. If he fails to identify, then there will be professional misconduct by the Auditor, so the Audit has to check the same. Therefore, a company following the accrual concept can save itself.

- The accrual concept depicts the true profitability of an organization.

- The accrual concept shows a more accurate financial statement than cash because cash basis recognizes when it is paid or received that may consist of the amount relating to another period also.

Suppose company X paid $ 26000 for electricity for 13 months and per month electricity is $ 2000.

As per the accrual basis, electricity expense will be $ 24000, i.e., $2000 per month, and it will recognize $ 2000 in the next year as it is related to next year’s expense, but as per cash basis full $ 26000 will be recognized in the books in the same year.

As we can see, the cash basis considers $ 2000 also, which is about next year; hence, it causes less profit this year and more profit in the next year.

Those following accrual concepts need not report anything in notes to accounts, but if the company is following a cash basis, it has to report in notes to accounts.

- Stakeholders are more focused on the accrual concept rather than the cash basis because the accrual concept shows the permanence of business and reflects the accurate and fair view of financial statement.

- An accrual basis is beneficial in the preparation of projected financial statements. It can determine the upcoming expense and sales, which provides a great tool in tax planning.

- Cash basis method is simple to use because it records the transaction when it is paid, it is generally used by small companies and individuals.

Disadvantages

The disadvantages of the expense recognition principle in accounting are detailed below.

- It is challenging for a small company to manage its books accounts because the accrual concept requires monthly reporting and a skilled employee to manage it properly.

- The major disadvantage of maintaining books of accounts on accrual is that we will report revenue and expenses as and when they happened without waiting for actual cash received; hence, it is sometimes difficult to pay taxes without cash received in hand.

- It is difficult for a small company where there is a liquidity problem. It has to pay taxes without having actual cash received.

- It is difficult to change from one method to the accrual method because it requires a cost.

- The cash basis recorded the transaction when it was paid. Still, in reality, there can be some expenses that need to be paid in the future, so investors will not be able to decide whether the company is making a profit or loss.

- The accrual basis principle does not suit a small company with a liquidity problem that exists, and it is also difficult for a small company at the time of payment of tax.

- The cash Basis principle does not depict the true profitability of a company.

- Accrual basis sometimes becomes very complicated, requiring skilled employees to maintain the same.

Change in Expenses Recognition Principles

A change in expense recognition principles is a change in accounting policy, and disclosure is required in the notes to the accounts.

Expense Recognition Principle Vs Revenue Recognition Principle

Both the above are two essential principles followed in the accounting process which provides guidance regarding how the expenses and revenues should be recognised in the financial statement and reporting. However, there are some important differences between them, as given below:

- The former is a guidance regarding how the expenses incurred should be recorder and the latter is a guidance regarding how the revenue should be recorded.

- The former states that the expense should be recorded when they are incurred and the latter states revenue should be recorded when it is earned.

- The former is considered as incurred when goods and services are received irrespective of when cash is paid, as per the accrual concept, but the latter is earned when goods and services are given, irrespective of when cash is received.

- The former is commonly used for transactions related to rent, wages, salaries, utilities, etc and the latter is used for interest received, royalty earned, long term subscriptions, contacts, etc.

Thus, the above points clearly highlight the basic differences between the two accounting concepts that are widely used for recording transactions in the books of accounts.

Recommended Articles

This has been a guide to what is Expense Recognition Principle. We explain it with examples, differences with revenue recognition, types & advantages. You can learn more about it from the following articles –