Part of our Accounting Concepts guide

What Is The Realization Principle?

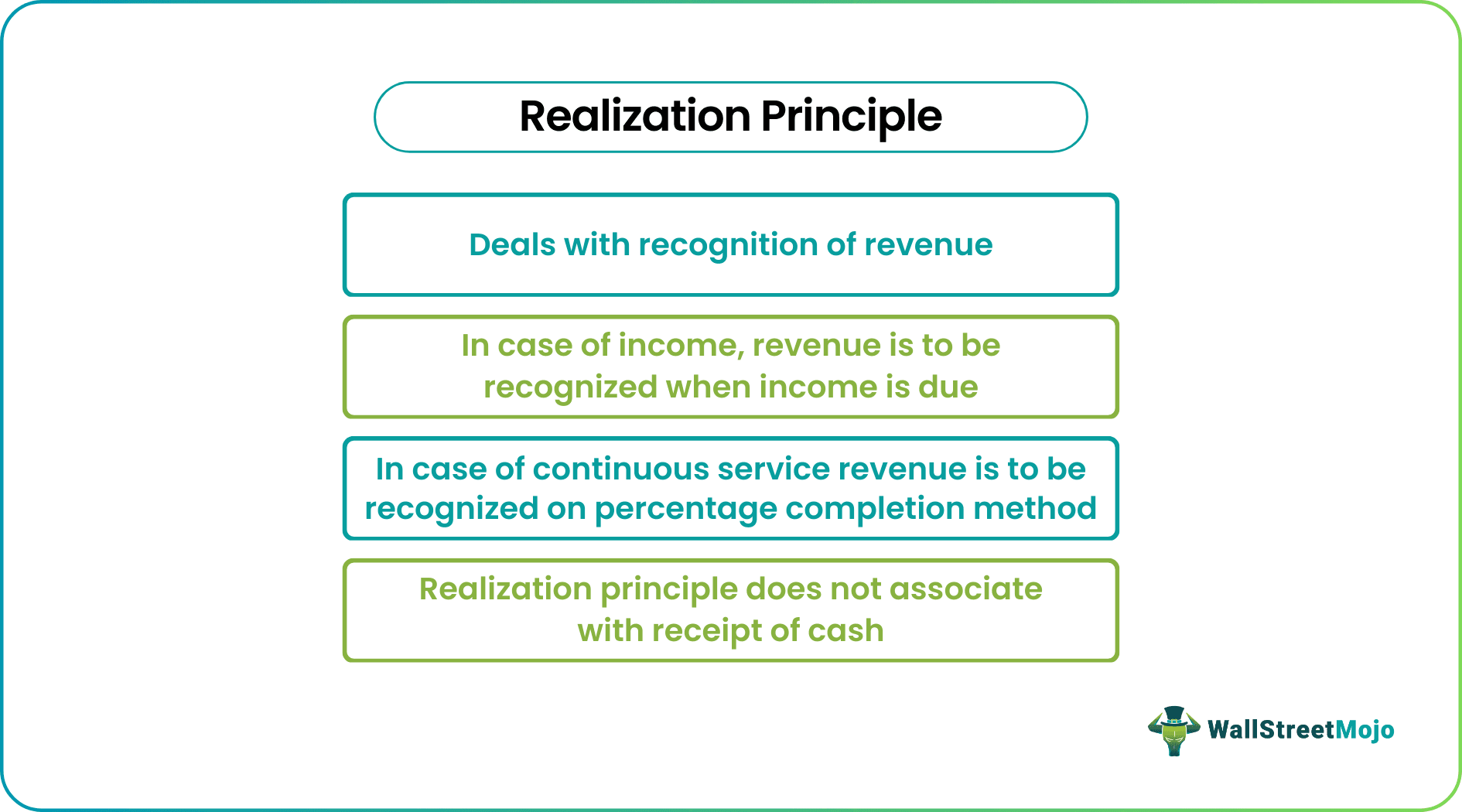

The realization Principle is a revenue recognition principle that states that the income or revenue is recognized only when earned. The company is reasonably certain that the payment against the same will be received from the customer. It generally occurs when the underlying goods are delivered, risk and rewards are transferred, or income gets due, irrespective of whether the amount is received or not.

Explanation

The realization principle deals with revenue recognition, i.e., profit should be realized when goods are transferred or risk and rewards are transferred. In the case of income, revenue is recognized when income is due. In the case of a continuous service business like a real estate business, revenue or income is to be recognized on the percentage completion method. According to this concept, revenue is to be recognized only when it is earned, or it becomes reasonably certain that the company will receive the payment from its customer. This revenue is realized when risk and rewards are transferred or income is due. The realization principle does not associate with a cash receipt, i.e., income is to be realized, or revenue is to be recognized even if the cash is not received. For example, revenue cannot be recognized if the advance is received, but goods are not transferred. It is to be recognized only when goods are delivered.

Examples

Example #1

I received $ 20,000 on 23-03-2020 as an advance against the goods purchased on 02-04-2020, amounting to $ 30,000. Goods are delivered on 05-04-2020. State when revenue is said to be realized as per the realization principle?

Solution – As per the Realization principle, in the case of goods, revenue is to be recognized only when the risk and rewards are transferred concerning an underlying asset where risk and rewards are said to be transferred when the goods are delivered, or the seller accepted his responsibility of the goods in case of damage or destroy at buyer place.

In the above case, the goods were delivered on 05-04-2020. So, the revenue is said to be realized on 05-04-2020. Hence sales are to be recorded on 05-04-2020 and not on 23-3-2020. The realization principle does not deal with the receipt of the amount.

Example #2

ABC Ltd. sells trucks to its sole dealer and enters into a contract to deliver the truck to the customers and maintenance for one year. State how revenue is to be recognized as per the recognition principle?

Solution – As per the Recognition principle, in the case of goods, revenue is to be recognized when all the risks and rewards related to the underlying asset are transferred.

In the case of services or investment, it is to be recognized when income is accrued.

In the case of continuous services, it is to be recognized on a percentage completion basis.

In the above case, the sale of the truck is related to the sale of goods, and the maintenance contract is the continuous service to be provided to the customer for a one year period.

So, according to the recognition principle, the revenue of trucks is to be recognized when risk and rewards related to the truck are transferred, or the truck is delivered, whichever is earlier.

In the case of a maintenance contract, revenue is to be recognized on a percentage completion basis, i.e., out of total trucks sold, only the trucks for which warranty period is completed, i.e., the service contract expired, are to be recognized.

Importance

- It ensures a true and fair view of the accounts as profit is to be realized and recognized only when the seller transfers risk and rewards.

- The risk can be minimized through the realization principle.

- True revenue earned during the year is given importance and recognition instead of revenue collection.

- It ensures recognition consistently.

- In the case of continuous services percentage of completion, the method can be used to recognize revenue. Hence it provides a solution for all types of revenue recognition based on the type of revenue.

- It gives importance to legal ownership, which is acceptable and enforceable by law.

Advantages

- The realization concept gives more importance to the recognition of revenue.

- It is commonly followed in a business organization as per the accrual system of accounting.

- It guides the accounting process and recognition of revenue.

- Through realization principles, the inflation of revenue and profits can be controlled.

- The true and fair view is better reflected in the realization concept.

Recommended Articles

This has been a guide to what is the Realization Principle and its definition. Here we discuss examples, importance, and realization principles in accounting and advantages. You may learn more about financing from the following articles –