Part of our Accounting Concepts guide

What Is Provision in Accounting?

The provision in accounting refers to an amount or obligation set aside by the business for present and future liabilities belonging to specific categories. By their very nature, provisions are estimates of probable loss related to the future for events undertaken in the past and present.

Provisions are calculated keeping into consideration the predefined regulatory guidelines by banks and financial institutions. However, any business can undertake them against bad debts or any other future liability. Such liabilities may include bad debt, reduced asset value, tax payments, warranties, pensions, unsold inventory costs, etc.

Provision in Accounting Explained

Provision in accounting can be set aside when the actual event against which providers are created crystallizes. It can happen when there is higher than expected recovery, lower than expected claims, etc. Also, it can be reversed if the actual liability turns out to be less than what was provisioned.

Firms are well aware that they may run short of funds at any point in time. They are likely to witness future expenses unexpectedly rising due to changing marketing sphere and their performance, Hence, they always try to have a sufficient amount set aside to be used to bear unexpected future costs arising due to any reason.

Provisions are different from reserves. Though both these terms are used for the funds kept aside for future obligations and expenses, there is still a difference between them. While provisions are funds kept aside from the net revenue or profits to bear specific future expenses, reserves are funds kept aside from profits to take care of any kind of expenses or liabilities, irrespective of the specificity.

Provisions in accounting differs from accrued expenses as well in terms of certainty. The former is associated with the uncertain future costs which may arise out of anywhere or anything. On the contrary, the latter is related to the expenses that are fixed to be taken care of at regular intervals.

These funds aside not only help companies remain prepared for the uncertain liabilities, but also let them understand the pattern related to financial obligations that increase or decrease over time. Based on the observation, the firms get a chance to assess their business and make decisions in accordance with that.

Features

The definition of provision in accounting specifies the features and importance of the process. However, for an in-depth look at the characteristics, the features have been listed below:

- Always associated with a future liability that is uncertain and cannot be fully quantified;

- It always leads to a reduction in profits for the business.

- It represents a liability for the business and forms part of the liability side in the balance sheet.

- It is done following certain regulatory guidelines (like Banks do provision under BASEL guidelines) or as per historical business practice (in the case of other businesses).

- It is undertaken in those cases where it is probable that an outflow of funds will happen or certain receivables will face delinquency.

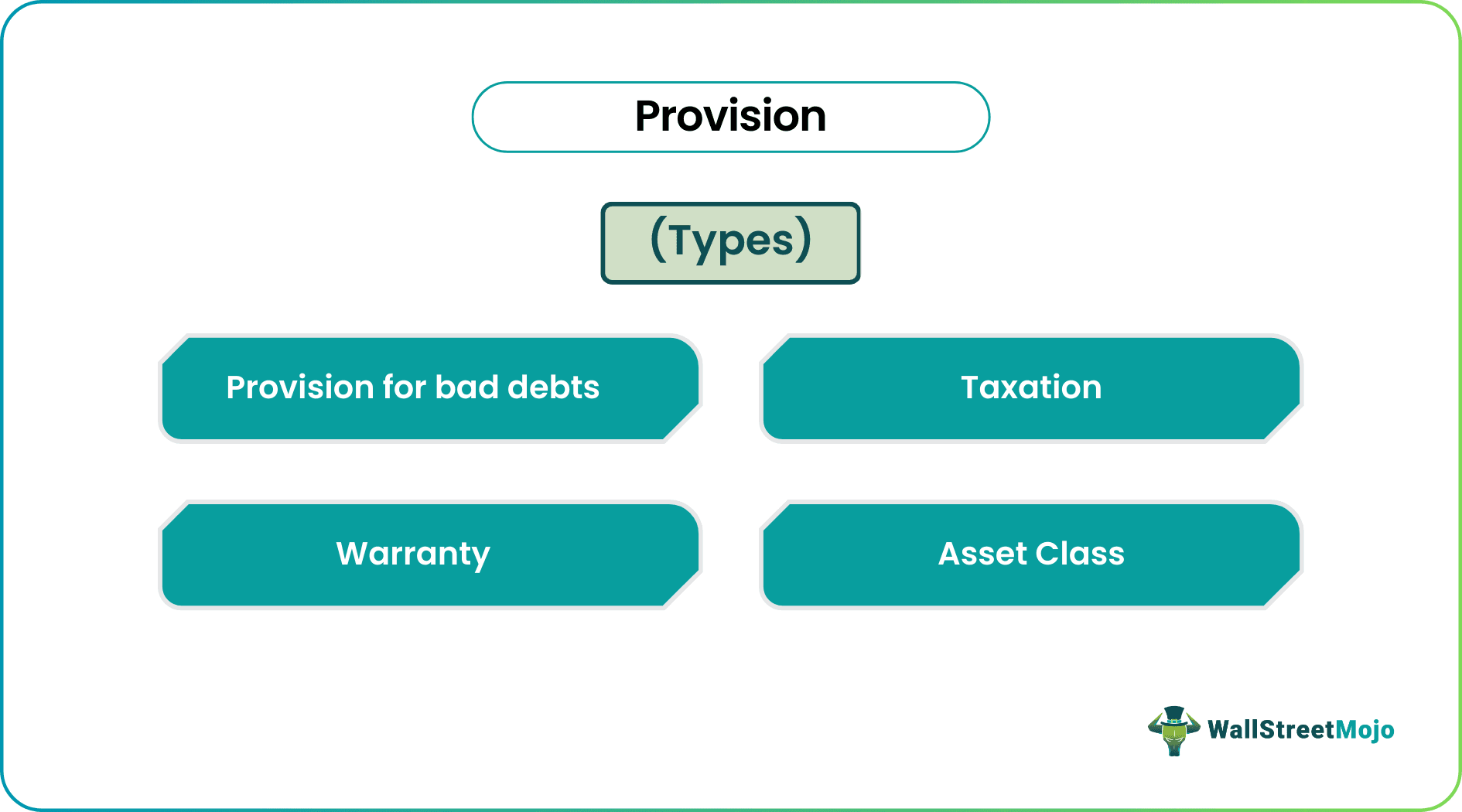

Types

There are different types of provisions created in the ordinary course of business. Some are confined to a particular business, while some are across business types. Here are the most common types –

- Provision for Bad Debts: This includes provisions marked by business against bad debts in the normal course of business based on historical averages.

- Warranty: This includes provisions made by the business for warranty extended by the business.

- Taxation: This includes provision arising out of tax liability as computed by a business based on Income earned following Income Tax Rules.

- Asset Class: This type of provision creation is confined to Bank and Financial Institutions, where a certain percentage of outstanding loan value is apportioned as Provision. The amount of percentage to be apportioned varies and increases as an Asset (i.e., Loan) defaults and moves from standard category to substandard category, doubtful, and loss asset.

How to Create?

The provision entry is made properly by following series of steps thoroughly. It is a two-step process, which include the following steps:

- Determine the amount of provision, which is again dependent upon various factors and varies for Industry and business across different jurisdictions.

- Accounting treatment of the provision amount is calculated in step 1, which involves debiting provision expenses from the Income Statement and creating a liability account under the Balance Sheet for the business.

Let’s explain the two steps with the help of a hypothetical example.

ABC Bank has provided a Term Loan to XYZ amounting to $100000, which requires a periodic monthly payment of $1200. XYZ has not paid the dues for the last three months, and accordingly, the ABC Bank has classified the account as Non-Performing Asset (NPA) and created a provision on the said Term loan equivalent to 20% of the amount of loan, i.e., 20% of $100000 which is $ 20000.

Thus as per step one, the amount of provision is $20000.

Now, $20000 is debited under Income Statement, and a separate provision account is created in the Balance Sheet equivalent to the same amount.

Example

Let us consider the following instance to understand how provision in accounting entry is made:

A company selling air conditioners with a year warranty has to set aside a certain amount as provisions for any claims that may arise during the warranty period. The company determines the Provision amount based on the past claims data for such air conditioners. This amount is debited from the income statement, thereby reducing the profits. At the end of the year, if the actual claims are less than the amount of provision, the balance amount is reversed back, thereby relinquishing the Provision Liability.

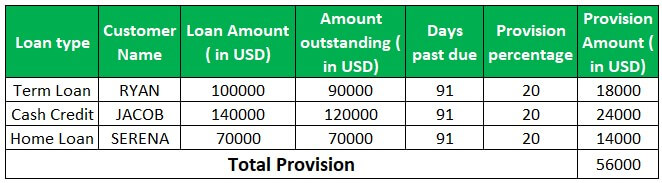

Bank A has granted the following three loans with the details as mentioned below:

Bank A will have to create a provision of 20% on the amount outstanding on each of the above loans as payment has gone past the due date over 90 days, classifying them into Non-performing Assets.

Thus Bank A will create a Provision of $56000 by debiting its Income Statement and creating liability under the head Provisions in the Balance Sheet Account.

Importance

The way these provisions in accounting are kept aside and used signify their importance. Some of the significances of these amounts are as follows:

- Provisions act as a cushion against future liabilities or on the happening of uncertain events.

- Instead of impacting the Income Statement in one go, provision helps businesses create a sinking fund type liability account in the Balance Sheet to navigate against such events.

- Every business is prone to bad debts, tax liability, etc. These expenses cannot be reliably estimated at the beginning itself, and that’s how provision comes into play by helping businesses better manage such unforeseen but certain events.

Recommended Articles

This article has been a guide to what is Provision in Accounting. Here, we explain the concept along with its types, importance, example, and features. You may learn more about financing from the following articles –