Table Of Contents

What is Intercompany Transaction?

Intercompany transactions are when one division, department, or unit of an organization takes part in a transaction with another division, department, or unit within the same organization. It is very common in multinational and big firms having subsidiaries.

A parent firm and a subsidiary, two or many affiliates, or even two or more divisions within one unit might be involved in these transactions. And many other triggers might set them off. For example, a firm may sell merchandise from one division to another division of the same company, or a parent company might lend money to one of its affiliates. Both of these scenarios include the company as a whole.

Table of contents

- What is Intercompany transaction?

- An intercompany transaction is a transaction that occurs between two firms or departments within the same organization.

- Amounts subtracted from gross income are not considered earnings and profits of any member and are not classed as exempt income.

- There are three intercompany transactions: upstream, downstream, and lateral.

- Examples include the sale or acquisition of inventory or fixed assets, the provision of loans, guarantees, or other commitments, the announcement and payment of dividends, and the provision or receipt of loans.

Intercompany Transaction Explained

A transaction involving corporations that, are between the members of the same unit or organization is referred to as an intercompany transaction. Considering E is the member who is receiving the property or services being transferred from A, who supplies the goods or services. Transactions between companies can involve the following:

- The sale of property by A to E (or any other transfer, such as an exchange or contribution), regardless of whether or whether A recognizes a gain or loss from the transaction;

- The execution of services by A for E, as well as the payment or accrual by E of its spending for A's performance;

- A's decision to provide E a license to use technological innovation, a rental of property, or a loan of money, as well as E's payment for or accrual of its expenditure; and

- The portion of A's shares given to E per A's distribution.

Trading activities may be involved in intercompany transactions. Examples of trading operations include the sale or purchase of inventories or fixed assets; the provision of loans, guarantees, or other obligations; the declaration and payment of dividends; and the provision of or receipt of loans. As a result, it is possible for balances on the balance sheet (such as accounts receivable and accounts payable, financial assets and financial liabilities, dividends payable and dividends receivable) and transactions on the income statement (such as sales and purchases, interest expenses, and dividends paid or received) to be created as a consequence of such transactions.

Timing Of Transaction

The timing of the transaction is also crucial to count it as a valid intercompany transaction. For example, suppose a transaction takes place in part while S and B are members and in part while they are not members. In that case, the transaction is considered to have taken place when implementation by either S or B takes place or when payment for performance would be taken into account under the rules of this section if it were an intercompany transaction, whichever occurs first. This applies even if the transaction occurs in part while S and B are members and in part while they are not. In situations like this, appropriate changes need to be made, such as splitting the transaction into two independent transactions that each indicate the degree to which S or B has been completed.

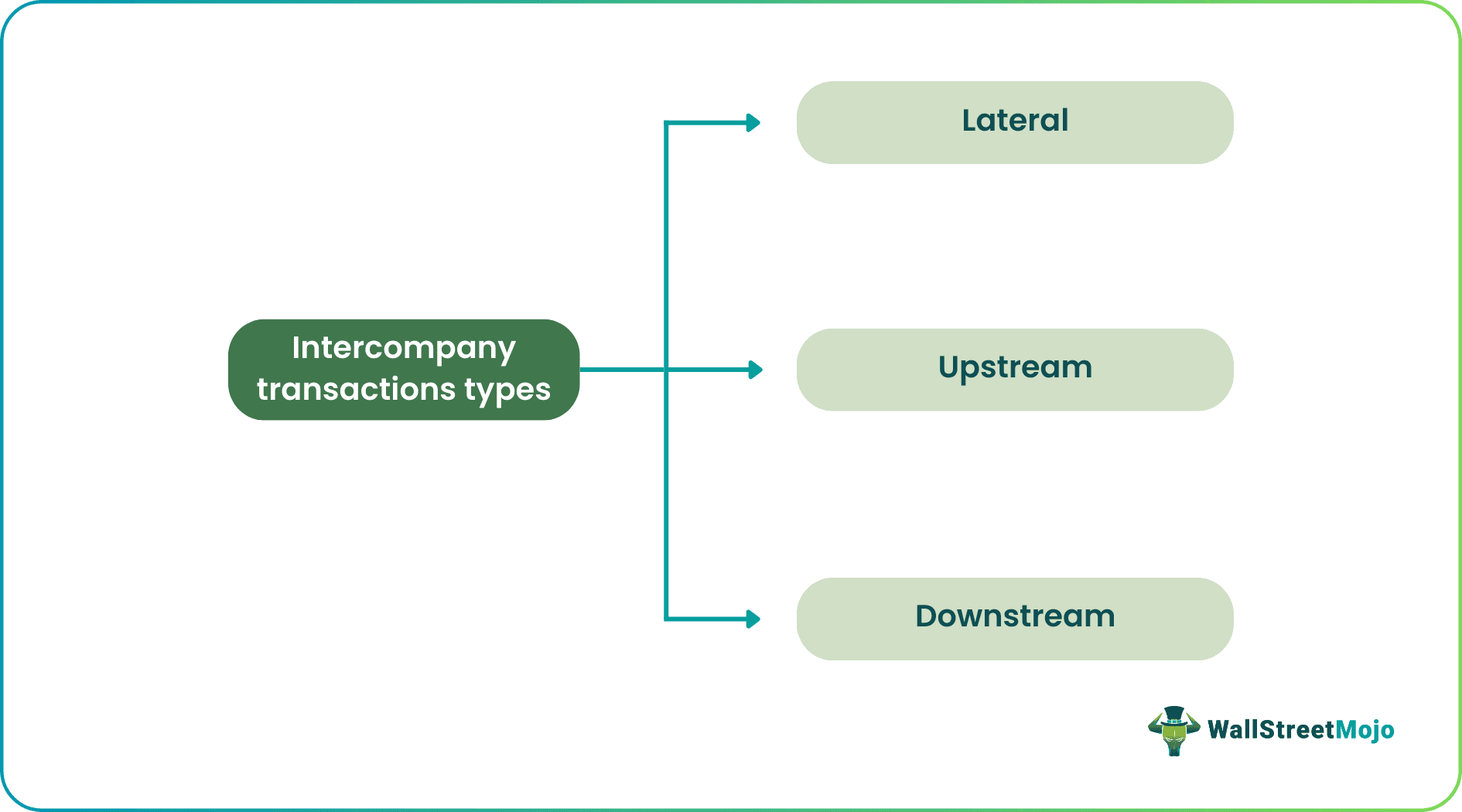

Types

The three primary kinds of intercompany transactions are lateral, upstream, and downstream.

#1 - Downstream

When a parent firm does business with one of its subsidiaries, this is known as a downstream transaction. When something like this occurs, the parent firm is the one that is responsible for recording the transaction as well as any associated profit or loss. As a result, only the parent business and its stakeholders, not the subsidiaries, have access to information on the transaction, making it invisible to them. A parent firm selling an asset or inventory to a subsidiary is an example of a transaction that falls under the category of "downstream."

#2 - Upstream

A transaction considered upstream moves from the subsidiary to the parent company. When an upstream transaction occurs, the subsidiary is responsible for recording the transaction and any associated profit or loss. As an illustration, a subsidiary may lend an executive to its parent business for a specific amount of time. It also simultaneously bills the parent company on an hourly basis for the person's services. Since they are co-owners of the subsidiary, stakeholders with can divide either the profit or loss from the subsidiary.

#3 - Lateral

A lateral transaction is a transaction between two different subsidiaries that are part of the same parent company. Accounting for a lateral transaction is very similar to accounting for an upstream transaction. It is recorded alongside the profit or loss by the subsidiary or subsidiaries. One illustration of this would be when one subsidiary charges another for the provision of information technology services.

Examples of Intercompany Transaction

Let us have a look at the examples to understand the concept better.

Example #1

Let's pick a basic scenario and use it as an illustration of what an intercompany transaction looks like. Imagine that business A is the parent of the other company. It has a subsidiary that goes by the moniker B. The parent firm will send cash to the subsidiary company in order to assist in managing its operations. Even if Firm A and Firm B have independent legal entities, the transfer of cash is an intercompany transaction.

Example #2

An article by B2B explains a number of use cases, and the challenges present during intercompany transactions. For example, in the case of the cost of products sold, expenses, accounts payable, personnel, cash, sales, and loan covenants, it explains and investigates many parts of the situation. It draws attention to potential errors that seem little but might have significant repercussions at a later time. Examples of this include the transfer of goods from the parent company to the subsidiary company. If there is no documentation or a difference in sales numbers in the case of comparable items with various versions.

Tax Treatment

- A's intercompany items include sums from a transaction that have not yet been accounted for using the distinct entity technique. For example, if A is a cash-method taxpayer, income is taxable even on nonreceipt of cash. Similarly, an intercompany item under A's method of accounting can be a replacement for gain or loss from a transaction.

- Separate entities of A's intercompany items and E's items are recalculated to produce a similar effect on consolidated taxable income. As if A and E were divisions of a single corporation, and the intercompany transaction was a transaction between divisions.

- The prohibited amount in the computation of any credit shows against federal income tax.

- Amount deductions from gross income are not considered earnings and profits and are not classified as tax-exempt income.

Frequently Asked Questions (FAQs)

A transaction between two companies or departments within the same organization is known as an intercompany transaction. In addition, transactions from a subsidiary to its parent company, transactions that take place from a subsidiary to another subsidiary, and transactions between subsidiaries are referred to as intercompany transactions.

It is necessary to eliminate the intercompany income and cost of sales resulting from the transaction in the consolidated financial statements. Eliminate intercompany receivables and payables, purchase, sales costs, and profit/loss from transaction accounts in the consolidated financial sheet.

Journal entries that belong particularly to intercompany transactions are known as intercompany journal entries. These are entries that are recorded in the accounting ledger of an organization. Therefore, the consolidated income statements, as well as the balance sheets, needs to be removed in the appropriate manner.

Recommended Articles

This article has been a guide to what is Intercompany Transaction and its meaning. Here, we explain the concept, its types, examples, and tax treatment. You may also find some useful articles here: